The Australian Dollar is long the commodity and short the customer

- AUD/USD logged its weakest close since April after another faded rally.

- China's data showed deflating demand and accelerating factory costs in the same morning.

- The RBA decides next Tuesday with household inflation expectations running hot.

The Australian Dollar (AUD) has everything a currency bull could ask for except a functioning customer, and Wednesday made that distinction expensive. AUD/USD popped with everything else after the soft core reading in the US Consumer Price Index (CPI) report, stalled ahead of 0.7050, then bled through the entire US session to finish just under the 0.7000 handle, its weakest close since April and nearly 300 pips below the May peak.

Washington's threat to resume strikes on Iran soured the afternoon tape, but the deeper problem arrived earlier from Beijing, where the morning's inflation data quietly confirmed what has capped the Aussie all month: the world's biggest commodity buyer is absorbing the energy shock as a margin squeeze rather than passing it on.

Beijing's margin squeeze is the Aussie's ceiling

The Chinese numbers deserve more attention than they received, because consumer prices missed at 1.2% YoY and outright fell 0.1% on the month, while the Producer Price Index (PPI) jumped a full point to 3.9%. Factory costs accelerating into deflating consumer demand is the definition of a margin squeeze, and squeezed Chinese producers historically respond by trimming output and import orders, which is to say by trimming the bulk-commodity demand that prices Australia's export book.

Australia sits on the right side of the Strait of Hormuz disruption, with liquefied natural gas (LNG) and coal receipts fattening the terms of trade, and Wednesday's renewed war rhetoric only steepens that tailwind on paper. The catch is that receipts require a buyer, every leg higher in Crude Oil tightens the margin squeeze choking that buyer's demand, and the buyer's retail sales are already running at 0.2% YoY into Tuesday's update at 02:00 GMT alongside industrial production. The real verdict on the Aussie arrives from Beijing roughly two hours before the RBA even speaks.

An embarrassment of hawkish riches

The domestic story, by contrast, is almost comically supportive. The Reserve Bank of Australia (RBA) raised its cash rate to 4.35% in May, a third consecutive hike delivered on an eight-to-one vote with a tone widely read as more hawkish than expected; monthly CPI hit 4.6% in March, the highest of the young monthly series, and the bank's own forecasts see underlying inflation peaking near 3.9% this quarter. Household inflation expectations sit at an uncomfortable 5.6% and refresh Thursday at 01:00 GMT, while economists remain split between a June hike and a pause until the next quarterly inflation report.

With the Federal Reserve (Fed) holding at 3.50% to 3.75%, the Aussie now carries a positive yield gap over the Dollar, and the RBA's own May minutes credited widening rate differentials and firm commodity prices for the currency's strength. Wednesday's close below 0.7000 is what it looks like when that entire framework collides with a customer that has stopped spending.

Levels and bias

Upside: Reclaiming 0.7000 puts the focus back on the zone close to 0.7050 where Wednesday's rally died, with the 50-day Exponential Moving Average (EMA) just above 0.7100 the gate back into the broader 2026 uptrend.

Downside: Initial support sits around 0.6950, with the rising 200-day EMA near 0.6900 the level where the bull case either holds or breaks.

Bias: Corrective. Next Tuesday stacks Chinese activity data at 02:00 GMT against the RBA decision at 04:30 GMT and its press conference an hour later, and until the China side of that ledger improves, bounces toward 0.7050 look like opportunities to sell rather than the start of a recovery. A hawkish RBA can decide how deep the floor sits; it cannot build the ceiling.

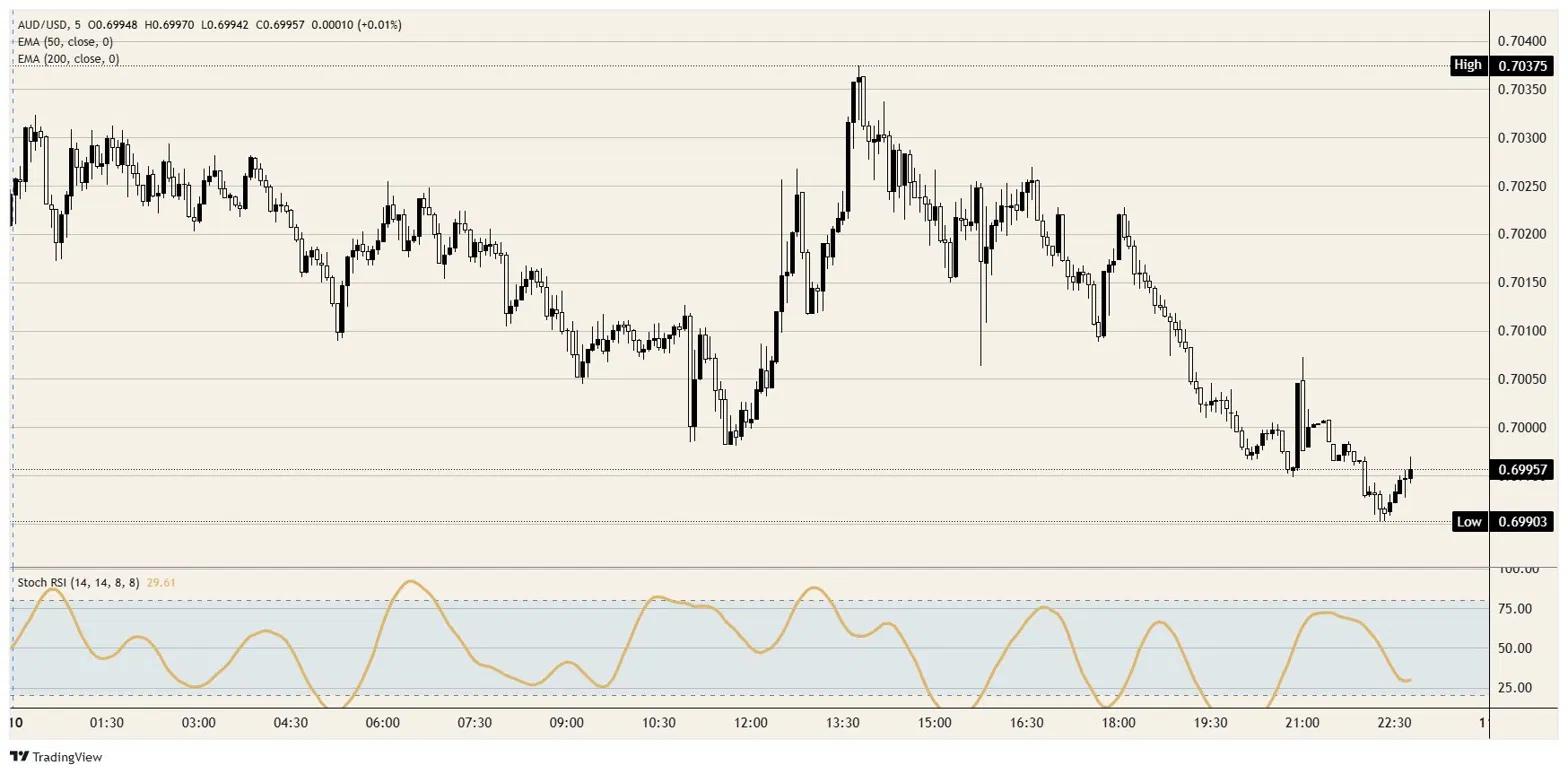

AUD/USD 5-minute chart

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.