The Mag 7 trade is ending – The AI cash-flow divorce is just beginning

- The AI boom is not weakening. The market is simply becoming less willing to reward companies for writing ever-larger infrastructure cheques without a clearer cash-return timetable.

- Microsoft, Amazon, Alphabet and Meta are becoming the financing arm of the AI cycle, while chips, memory, networking and power infrastructure increasingly look like the early cash beneficiaries.

- NVIDIA remains central to the AI buildout, but its share price is now being judged on the duration of exceptional returns rather than the existence of exceptional demand.

- The broad Mag 7 basket trade is giving way to stock selection, technical dispersion and a much sharper focus on free cash flow, margins and return on invested capital.

The Mag 7 trade is ending

The old Mag 7 trade was simple: own America’s best businesses, own the AI future, let index gravity and passive flows do the rest. It was one ticket for everything investors wanted to believe in: monopolistic margins, endless cash generation, cloud growth, AI upside and just enough scarcity to keep the multiples rich.

That trade is starting to come apart at the seams.

This is not a call that the Mag 7 is finished, or that these companies have suddenly become bad businesses. It is a recognition that the basket is no longer doing one job. The same AI boom that turned them into the market’s crown jewels is now forcing investors to separate the firms writing the cheques from the firms cashing them.

Microsoft, Amazon, Alphabet and Meta are spending like industrial empires trying to lock down the next cycle before anyone else gets there. Only this time, the railroads are GPUs, memory, data centres, power contracts, and ever more expensive financing leases. NVIDIA, memory suppliers, storage names, networking firms and selected semiconductor infrastructure companies are standing at the other end of the counter collecting the money.

Demand has not gone away. Quite the opposite. Every fresh sign that AI demand is real seems to come with another huge capital bill attached. That is the bit investors are now wrestling with. Not whether AI matters, but who gets paid first, who gets paid last and whether the eventual returns justify turning the world’s best cash machines into capital-heavy utilities.

The numbers make the point. Microsoft is pointing to roughly $190 billion of 2026 capital expenditure. Amazon expects about $200 billion. Alphabet has raised its range to $180–190 billion, while Meta is targeting $125–145 billion. Put that together and the four biggest AI builders are heading toward roughly $700 billion of annual spending before the market has properly worked out where the incremental return will land.

As usual, thanks to The Market Ear — the oracle of charts — for the visual roadmap. Their technical sweep captures what the index masks: the Mag 7 is no longer one trade, but seven increasingly different arguments about AI spending, cash flow and who ultimately gets to cash the cheque.

That is why the old shorthand of “buy the Mag 7” has begun to look increasingly stale. In the first phase of the AI boom, all roads led higher because the market was pricing abundance: higher cloud demand, greater productivity, larger margins and a once-in-a-generation technology cycle. In the second phase, investors are discovering that abundance still needs to be financed.

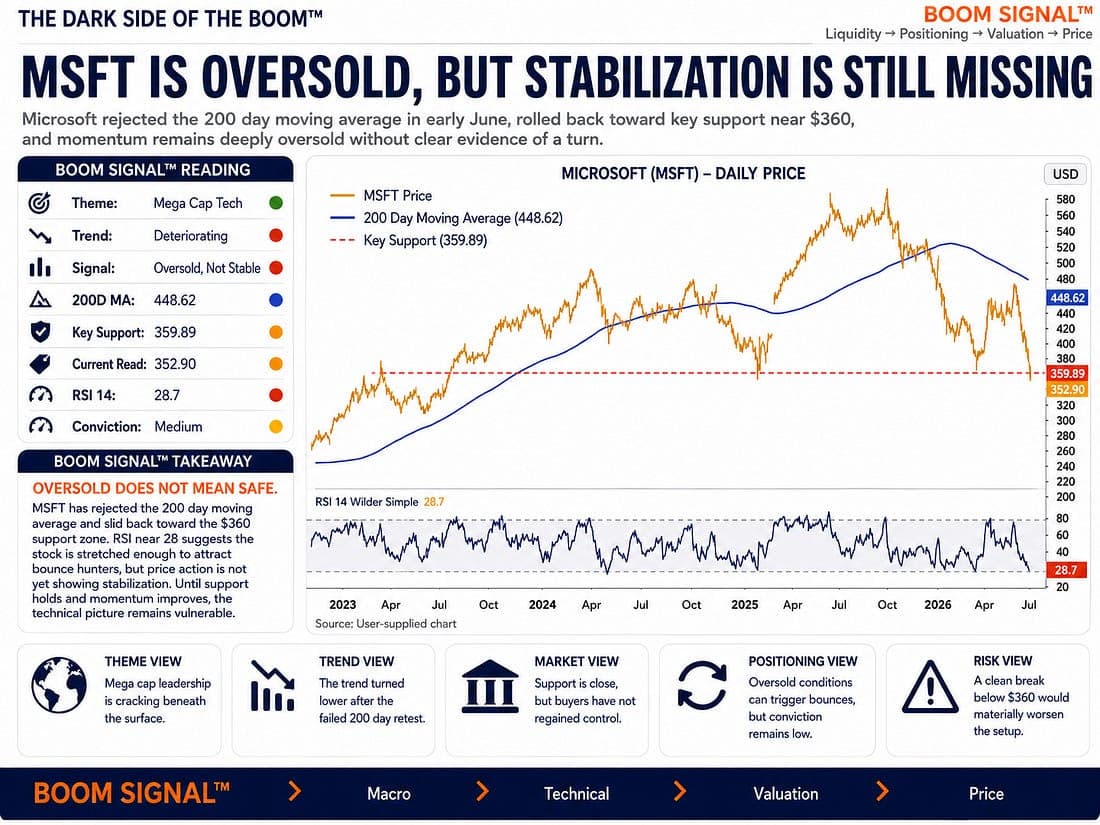

The technical picture reflects that loss of unity. Apple is sliding toward the $270 support area, where its 200-day moving average and longer-term trendline converge. Amazon has slipped below its 200-day moving average, with $220 now looking like the line in the sand. Microsoft has become the clearest example of the market’s new anxiety: an extraordinary business whose chart is being punished because investors are suddenly more focused on the bill than the payoff.

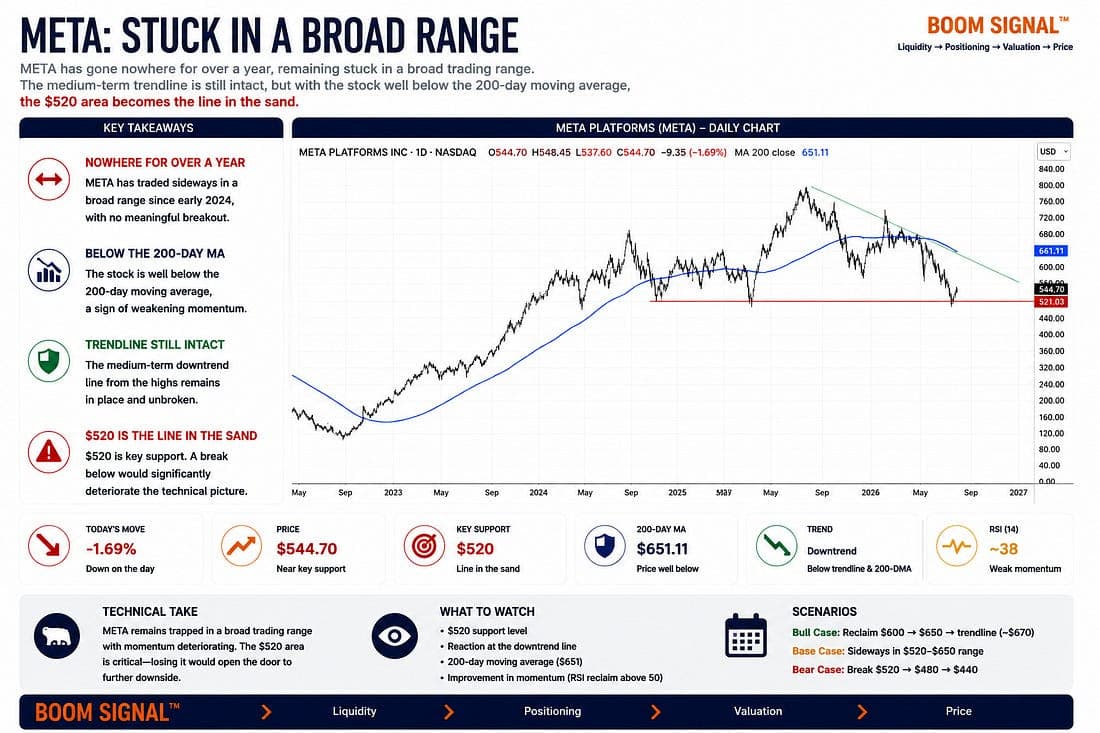

Meta is trapped in a broad range, with the $520 area becoming increasingly important. Alphabet remains in comparatively better shape, still holding above its 200-day moving average as cloud growth and a clearer revenue path offer some insulation.

NVIDIA, meanwhile, has gone from undisputed market leader to dead money, trading around levels seen months ago despite remaining at the centre of the AI supply chain.

That last point matters. NVIDIA is not being sold because the AI buildout is over. It is being treated as a duration trade. The market has started asking whether the extraordinary revenue and margin profile can remain extraordinary once every hyperscaler has already filled warehouses with chips, once custom silicon gains ground and once the buyers begin to care more about return on capital than raw compute capacity.

This is where the Mag 7 story stops being a headline and turns back into a market where the differences matter. There is no single fault line running through the group. Apple is dealing with a softer hardware and pricing backdrop. Amazon is being judged less on AWS growth than on how much cash it must keep feeding into the machine to sustain it. Microsoft has become the cleanest example of the market’s new discomfort: an exceptional business, spending exceptional sums, while investors wait to see when the AI bill turns back into margins.

Meta still has the advertising cash register ringing, but the market is starting to ask how long the infrastructure spending can run before it dents the operating story. Alphabet looks better placed because Cloud monetisation is visible, even if it remains one of the biggest writers of AI cheques. Tesla, as ever, is off in its own corner of the casino, trading as much on positioning and narrative as on any conventional valuation framework.

The franchises have not suddenly broken. What has changed is the market’s patience. For years, the Mag 7 gave investors both sides of the trade: growth on the way up and quality underneath it. They threw off cash, bought back stock, widened margins and kept a hand on the next big opportunity.

Now AI is beginning to force a choice. Money that once found its way back to shareholders is being swallowed by data centres, chips, power contracts and lease commitments. The earnings damage may not be fully visible yet, but the market has started to smell it.

That is why the money is starting to look past the architects of the AI buildout and toward the toll collectors. The firms funding the race may still own the long-term prize, but markets are rarely patient with the side paying for the stadium while someone else sells the tickets, the concrete and the electricity.

That does not make this a simple sell-the-platforms, buy-the-semis trade. The cashers are crowded too, especially where scarcity and pricing power have already been priced as permanent. But the old one-click Mag 7 allocation is no longer doing enough work. Dispersion is back. Balance sheets matter again. So does cash conversion. And for the first time in a while, the market wants to know who can monetize AI now, not just who can describe the opportunity best for 2028.

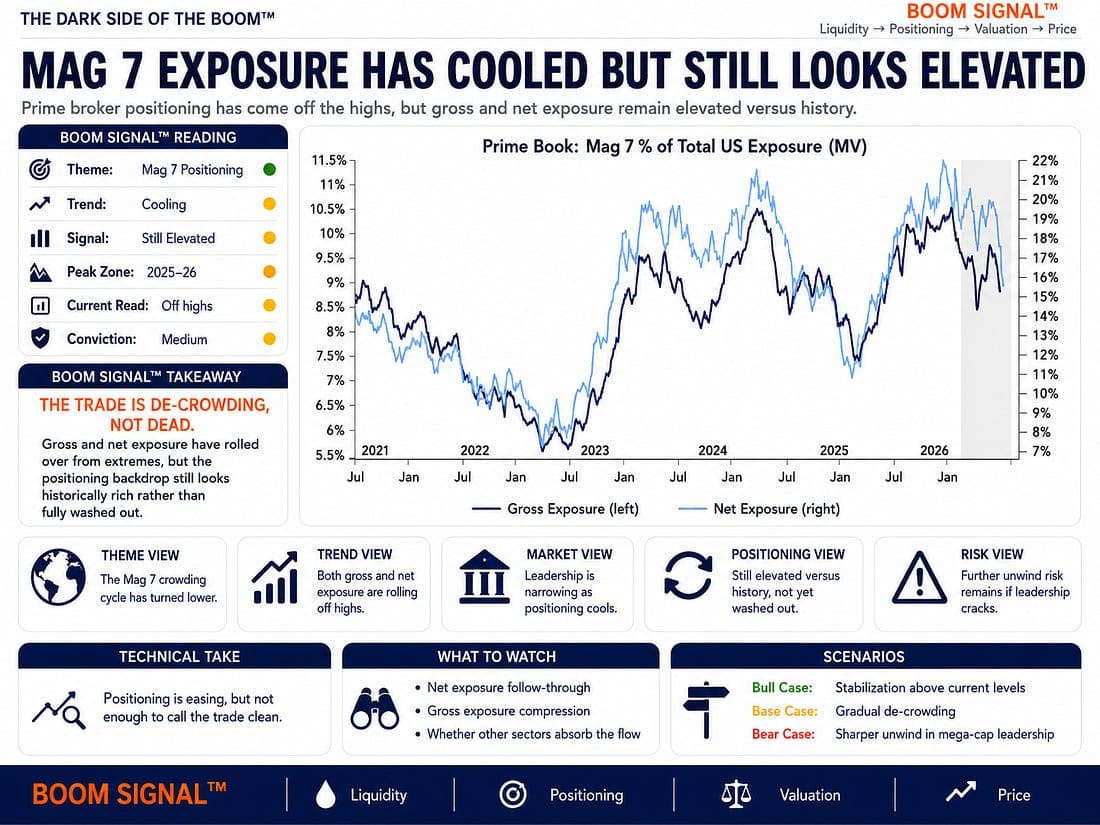

Goldman’s positioning work above suggests that capitulation is beginning to creep into Mag 7 exposure. That is important because the relative risk-reward is improving in places, particularly where deeply oversold technicals are meeting long-term support. But this is not yet a return to the old playbook of blindly buying the basket every time it wobbles.

The next winning trade is unlikely to be “the Mag 7” in the way it was before. It will be the companies that can show they are not merely financing the AI boom, but extracting cash from it. The winners will be those that can turn compute into revenue, revenue into margins and margins into free cash flow without needing to keep feeding the machine at an ever-faster pace.

The Mag 7 is no longer one trade. They are, in fact, seven very different arguments about the price of AI's future.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.