The AI boom is starting to look like a credit bubble wearing a silicon halo

- The AI supercycle is no longer just a technology story. It has become one of the largest debt-funded infrastructure booms in modern market history.

- Hyperscalers are evolving from cash-rich software giants into capital-hungry industrial utilities consuming staggering amounts of financing.

- Credit markets, not equity markets, now hold the real keys to the AI kingdom. If funding conditions tighten, the entire buildout slows.

- The investment-grade market is becoming dangerously concentrated around a handful of hyperscalers and data center financings, creating “concentration without upside” risk for bond investors.

- Beneath the equity market euphoria, credit investors are already demanding higher compensation, stronger protections and more creative financing structures as cracks begin to emerge in the AI debt machine.

Credit bubble wearing a Silicon Halo

Last Wednesday’s hyperscaler earnings barrage felt less like earnings season and more like watching the Pentagon, Wall Street and the Industrial Revolution hold a joint press conference. In the span of a single hour, more than $12 trillion in market cap marched across the tape, and while the earnings themselves were mixed, the message underneath them landed like a transformer exploding in the night. The AI arms race is no longer about software. It is about infrastructure. Concrete. Copper. Cooling systems. Nuclear-scale electricity demand. And above all else, debt.

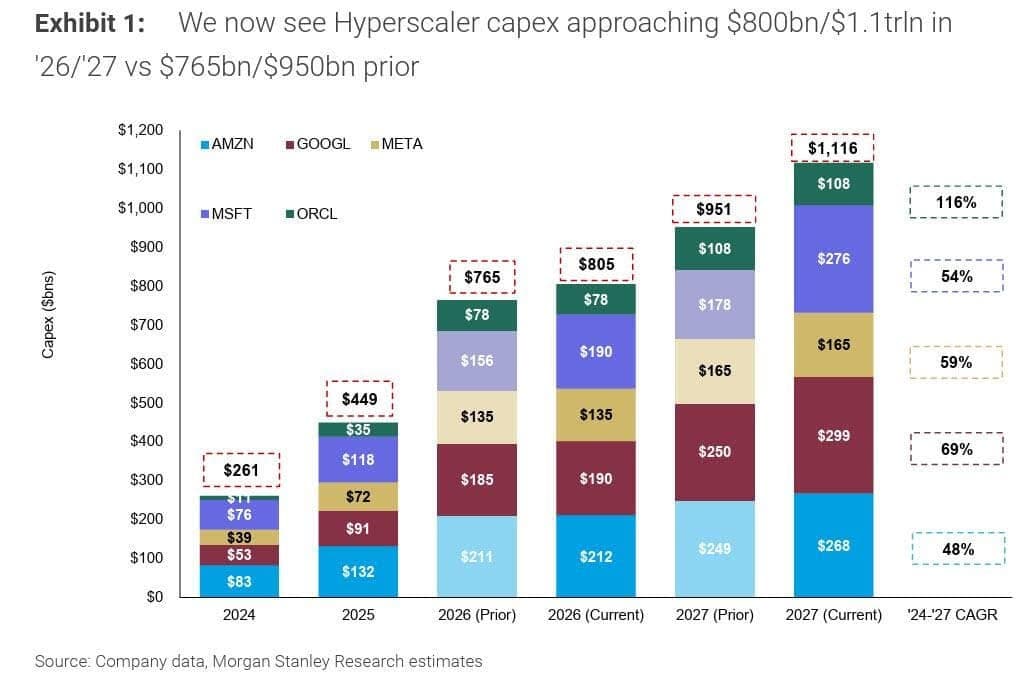

Morgan Stanley now estimates the Big 5 hyperscalers, Amazon, Alphabet, Meta, Microsoft and Oracle, will collectively spend roughly $800 billion on capex in 2026 before climbing toward an eye-watering $1.1 trillion in 2027. Andrew Sheets framed it perfectly. Next year’s spend is nearly double the 2025 levels and triple what was spent in 2024. That is not a normal investment cycle. That is the digital equivalent of rebuilding the interstate highway system while the economy is still driving on it.

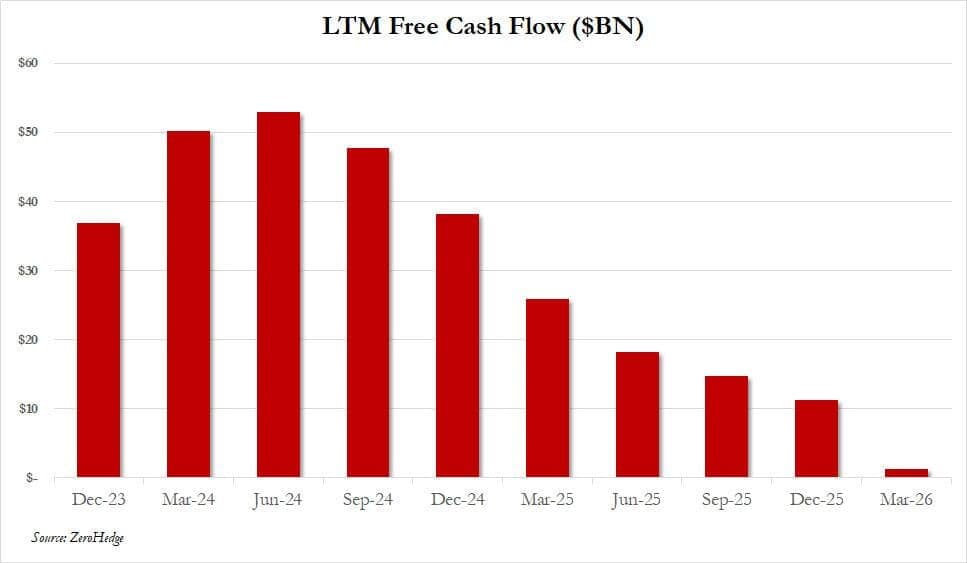

The market is still treating AI like a growth story, but the bond market has started reading it like a leverage story. That distinction matters. The hyperscalers used to be cash printing machines with feather-light business models. Now they are slowly mutating into capital-hungry utility giants with software-company valuations. Free cash flow is no longer overflowing out the back door because it is being shoveled directly into data centers, chip clusters, cooling towers and power grids.

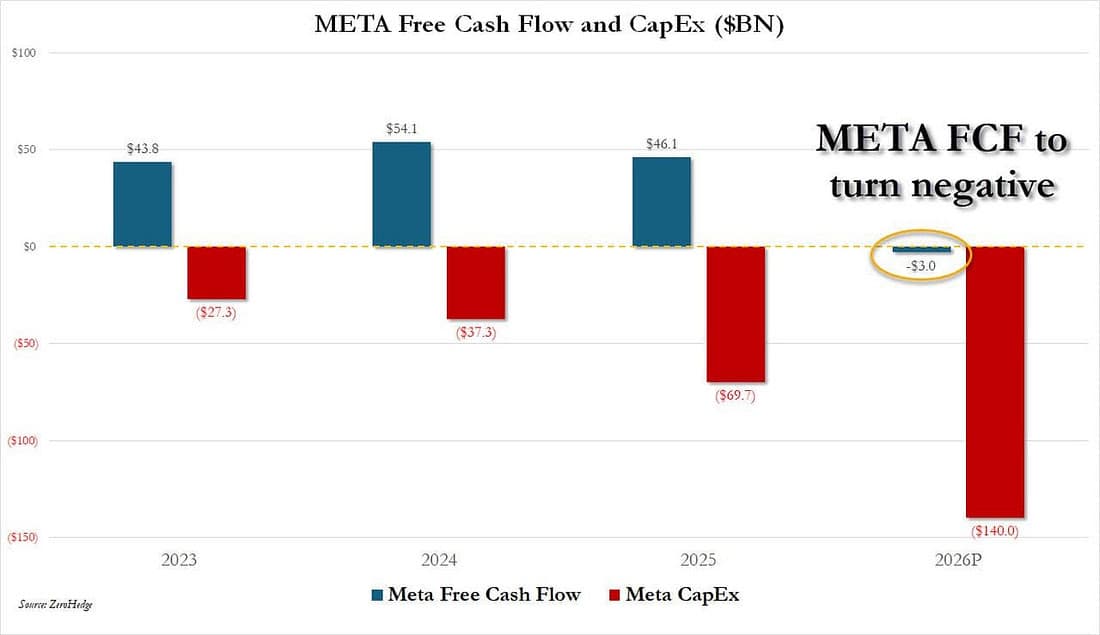

Amazon’s free cash flow profile already looks like a company trying to swallow an aircraft carrier whole. Meta’s cash generation is beginning to bend under the weight too. The equity market still sees cloud kingdoms. Credit investors increasingly see giant industrial furnaces that need to be fed every quarter.

And this is where the AI story quietly stops being an equity mania and starts becoming a credit supercycle.

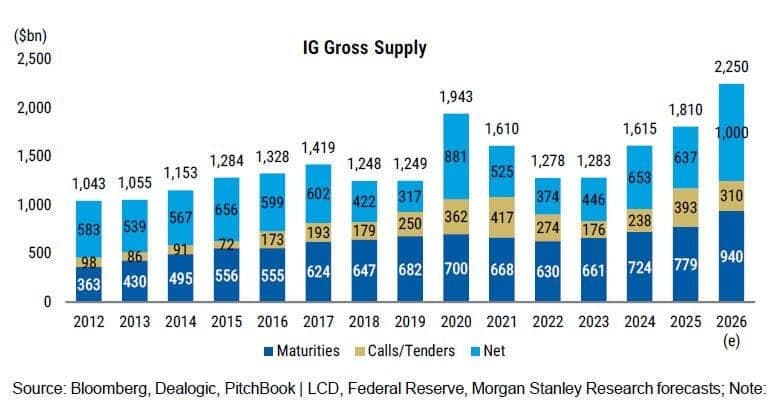

Morgan Stanley’s framework captures the contradiction beautifully. One company’s capex is another company’s revenue. That explains why semiconductor stocks exploded higher and why every AI adjacent equity trade suddenly feels bulletproof. But these outlays are now so enormous that even the richest companies on earth need to borrow to keep the machine running while preserving buybacks and dividends. US investment-grade issuance is already running roughly 20% above last year, and tech is driving a large share of it. Worse still, much of the debt is long dated, meaning the market is being force-fed duration at precisely the moment investors are already nervous about rates, deficits and supply indigestion.

Equities are partying on the penthouse floor while credit is downstairs checking whether the building foundations are starting to crack.

The first signs of fatigue are already surfacing. Bloomberg reported that after roughly $300 billion of AI debt flooded markets, investors are beginning to push back. Meta still managed to attract huge demand for its latest jumbo deal, but the order book was materially smaller than the frenzy surrounding its previous issuance. SoftBank-linked financing had to sweeten yields just to get buyers interested. Lenders are increasingly demanding backstops, guarantees and covenant protections tied to data center projects.

That is not the behaviour of a market swimming in blind optimism. That is the behaviour of a market beginning to ask where the exits are located before the theatre gets too crowded.

Data center financing itself is starting to resemble late-cycle commercial real estate with an AI paint job. Investors are no longer simply buying “the future.” They are asking old-fashioned credit questions. Can the project actually be built? Can it secure enough electricity? Will construction costs explode? Is the tenant real? Can the borrower survive delays? Can the facility remain economically viable if technology evolves faster than depreciation schedules?

The AI dream suddenly looks a lot less weightless when it has to pass through a credit committee.

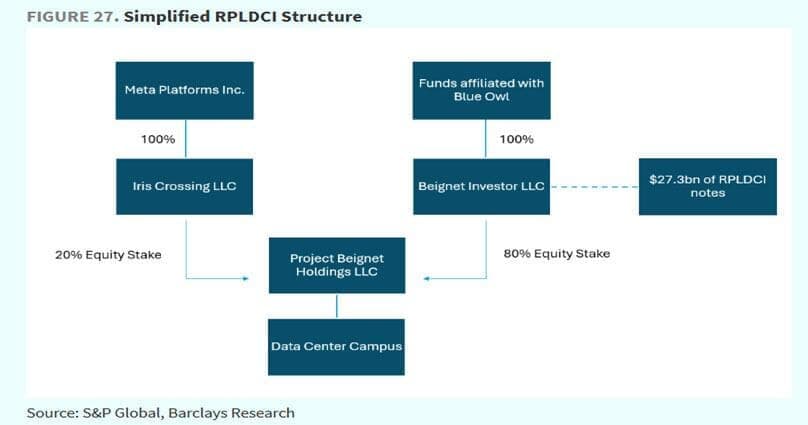

Meta’s increasingly exotic financing structures tell the story. Project Beignet. Project Sopaipilla. SPVs wrapped inside partnerships with Morgan Stanley, JPMorgan and private capital firms. These are not just clever financing vehicles. They are pressure release valves designed to spread risk across as many balance sheets as possible. When everybody wants to share the debt burden, it usually means nobody wants to be the last one holding the grenade.

The banks know it too. According to the Financial Times, major lenders are already scrambling to offload pieces of massive data center loans through private transactions, risk transfers and synthetic structures. The reason is simple. AI infrastructure borrowing is reaching sizes that are beginning to choke the arteries of the financial system itself.

One Oracle-linked financing reportedly took more than 6 months to distribute because demand simply was not deep enough. Some lenders even explored selling portions at a discount just to free up balance sheet space. That should matter a lot more to equity investors than it currently does.Because this is the hidden truth underneath the AI meltdown. The entire supercycle now depends on the smooth functioning of credit markets.

Morgan Stanley effectively admits this outright. Its analysts estimate that credit markets will finance more than $1 trillion in global data center spending through 2028. In other words, Silicon Valley may be designing the future, but bond investors are financing it.

And this is where the story becomes dangerous.

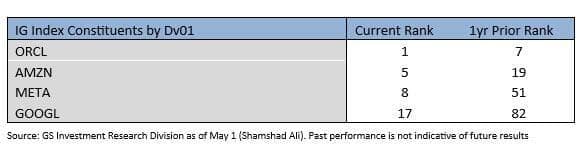

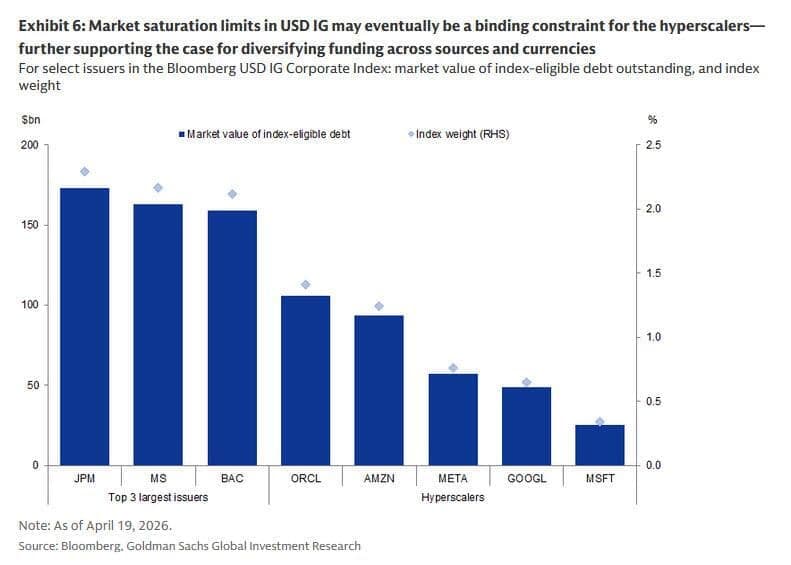

The investment-grade market is beginning to mirror the concentration risk already haunting equities. Goldman notes that just a handful of hyperscalers and AI data center deals now account for an enormous share of duration-adjusted issuance. Oracle has become one of the largest risk-weighted names in the IG universe. Meta has rocketed up the rankings in less than a year. The AI trade is no longer diversified. It is becoming a single, crowded theatre packed with ever-larger debt stacks.

That creates what Goldman calls “concentration without the upside.” Equities at least offer the theoretical potential for moonshot returns. Credit does not. Bondholders absorb the same concentration risk but with capped returns and massive downside asymmetry if spreads widen aggressively. The entire IG market is slowly morphing into a leveraged sidecar attached to the AI narrative.

And the supply wave is only beginning.

Morgan Stanley expects gross IG issuance to hit roughly $2.25 trillion next year, potentially the busiest year on record. Goldman says this year is already off to the strongest start in history. Technology alone now represents 18% of all USD investment-grade issuance, double last year’s pace.

The market can temporarily absorb almost anything when greed runs hot enough. But eventually, even the deepest bond markets start behaving like overpacked cargo ships. The weight matters. The duration matters. The concentration matters.

And there is another layer of risk the market still barely prices. Public backlash. Data centers consume staggering amounts of electricity and water, and communities are beginning to notice. Maine already passed restrictions. Other states are lining up behind it. AI infrastructure may be the market’s favourite child today, but rising utility bills have a funny way of turning political sentiment radioactive.

That means execution risk is no longer theoretical. It is political, environmental and social. Credit investors understand this instinctively because, unlike equity momentum traders, bondholders obsess over what can go wrong rather than what might go right.

The irony in all of this is almost poetic. AI was supposed to be the technology that eliminated friction, reduced labour, and digitized the economy, making it lighter and more efficient. Instead, it is becoming one of the most capital-intensive industrial buildouts in modern history.

This is no longer just a software boom.

It is a debt-fueled power grid expansion disguised as a technology rally.

And the market’s entire faith now rests on one fragile assumption. That credit markets remain permanently open, liquid and willing to absorb trillions in new supply without demanding meaningfully higher compensation.

If that assumption holds, the AI supercycle keeps levitating.

If it breaks, the market will suddenly discover that even the future has a funding cost.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.