Stocks to rally after CPI, but will they reach new highs?

The S&P 500 bounced on Monday, and today it’s going to open much higher after the CPI data. Will the uptrend resume?

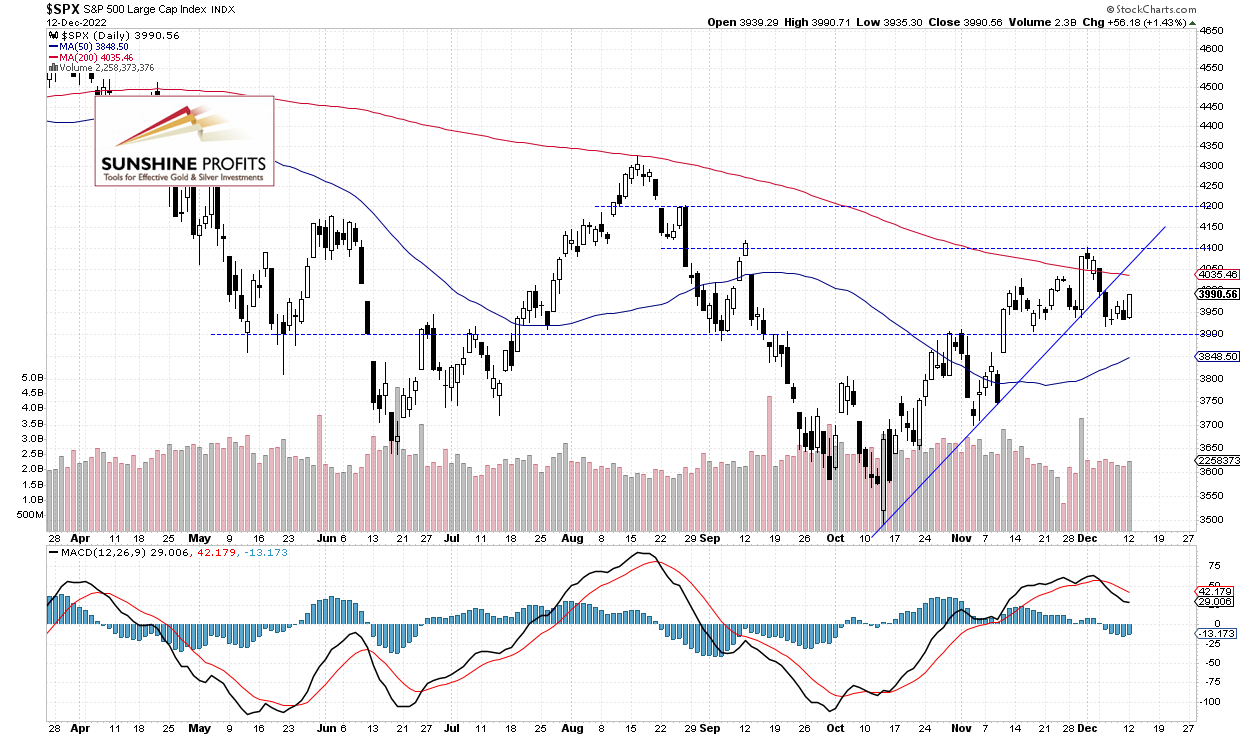

The broad stock market index gained 1.43% yesterday, as it went the highest since last Tuesday. Last week on Monday it reversed lower after a better-than-expected ISM Services PMI release, and on Tuesday it was as low as 3,918.39 (going down from its last week’s local high of 4,100.51).

This morning the S&P 500 will likely open 2.7% higher following lower-than-expected Consumer Price Index release. The market will be now waiting for tomorrow’s FOMC release. It still looks like a weeks-long consolidation within an uptrend. However, last week on Tuesday the index broke below its two-month-long upward trend line, as we can see on the daily chart:

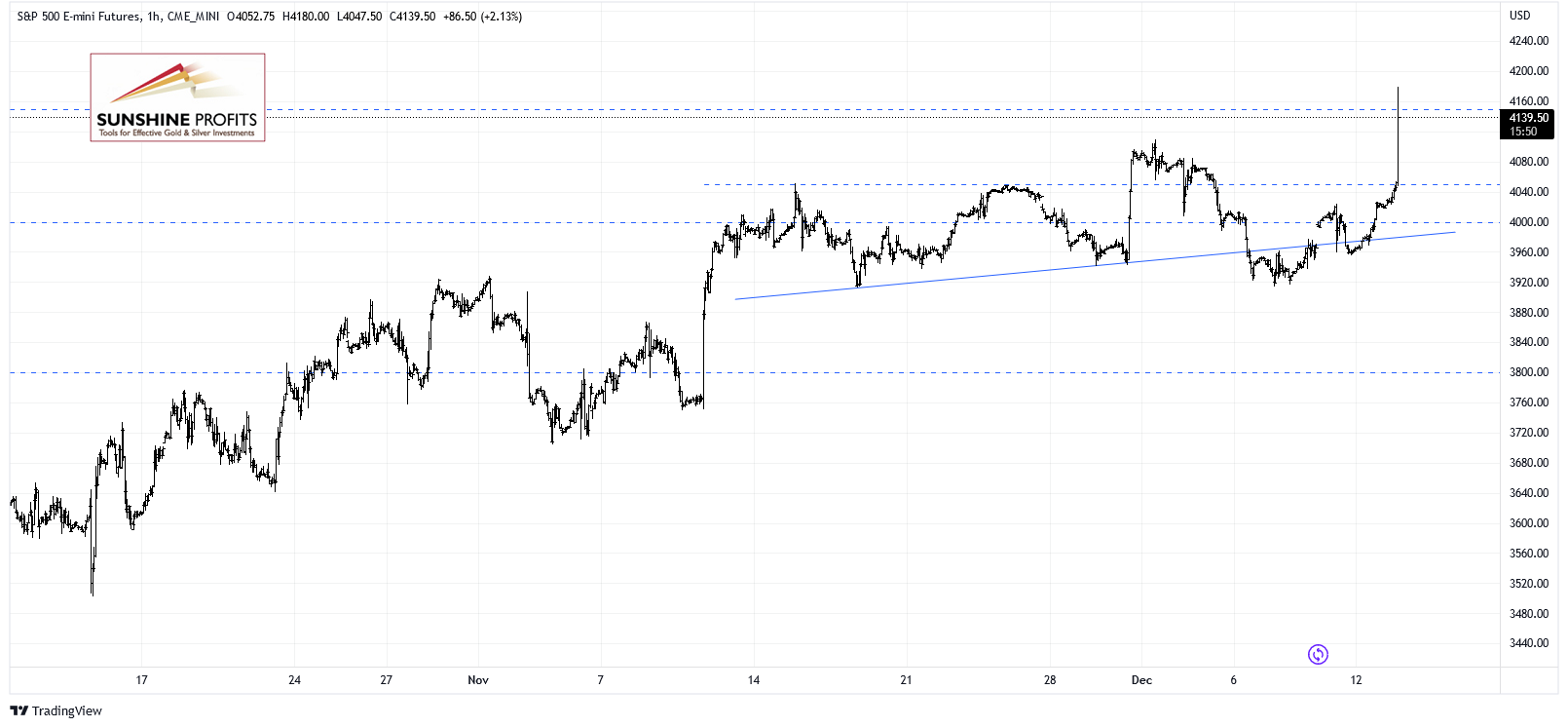

Futures contract rallies to new high

Let’s take a look at the hourly chart of the S&P 500 futures contract. It broke above the previous local highs on the inflation release. The support level is now at 4,050-4,100, marked by the recent resistance level.

Conclusion

Stocks are about to open much higher this morning on lower than expected consumer inflation release. So the S&P 500 index will likely get back above the 4,000 level. Tomorrow we will have the important FOMC release, and there will likely be even more volatility.

Here’s the breakdown:

-

S&P 500 index got close to the 4,000 level yesterday, and today it will break above it.

-

Stock prices may resume their two-month-long uptrend.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Paul Rejczak

Gold Price Forecast

Paul Rejczak is a stock market strategist who has been known for the quality of his technical and fundamental analysis since the late nineties.