JOLTS Job Openings set to decline slightly in May as Fed focuses on taming inflation

- US JOLTS are forecast to have eased to 7.28 million in May, yet remaining above the 2025 average.

- Job Openings data will be watched to confirm market expectations of Federal Reserve rate hikes.

- EUR/USD remains on the defensive, with 13-month lows at a relatively short distance.

The US Bureau of Labor Statistics will release the Job Openings and Labor Turnover Survey (JOLTS) for May on Tuesday at 14:00 GMT. The report, which gathers US employers’ estimates of job openings, hires, and separations nationwide, is closely watched by the market as it normally comes ahead of an array of employment gauges released throughout the week, culminating in the key Nonfarm Payrolls report.

May’s JOLTS figures are likely to be closely watched on Tuesday because they come in a crucial moment, with markets repricing chances of interest rate hikes by the US Federal Reserve (Fed) as inflation keeps rising well above the central bank’s target.

A high level of uncertainty surrounds the Middle East conflict, and inflationary pressures have failed to abate despite the recent decline in Crude prices. The Fed has reiterated its commitment to fight inflation, boosting investors’ hopes of at least one rate hike this year. In this scenario, this week’s labour market data might be key to assessing the timing of the next monetary policy move and give a fresh boost to US Dollar (USD) volatility.

What to expect in the next JOLTS report?

Job openings are expected to come in at 7.28 million in May, according to the market consensus. This is a moderate decline from April’s 7.61 million openings, which was the best reading since July 2024, but still a good reading, as it remains significantly above the 2025 average of 7.08 million openings. If these figures are confirmed, they are likely to endorse the theory of a stabilising US labour market and underpin the narrative of US economic exceptionality.

April’s JOLTS data beat expectations with a 4.6% monthly increase in job openings – 731,000 new vacancies – from March’s 6.88 million openings, while quits, layoffs, and discharges were little changed.

Beyond that, the US Nonfarm Payrolls release reported 172K new jobs in May, completing an impressive performance in the three months to May. These figures boosted market confidence about the US economic resilience to the Middle East war and allowed Fed policymakers to forget about the labor market and focus solely on the overshooting inflationary levels to draw their near-term monetary policy. This new scenario has prompted investors to ramp up bets of some monetary policy tightening in the coming months.

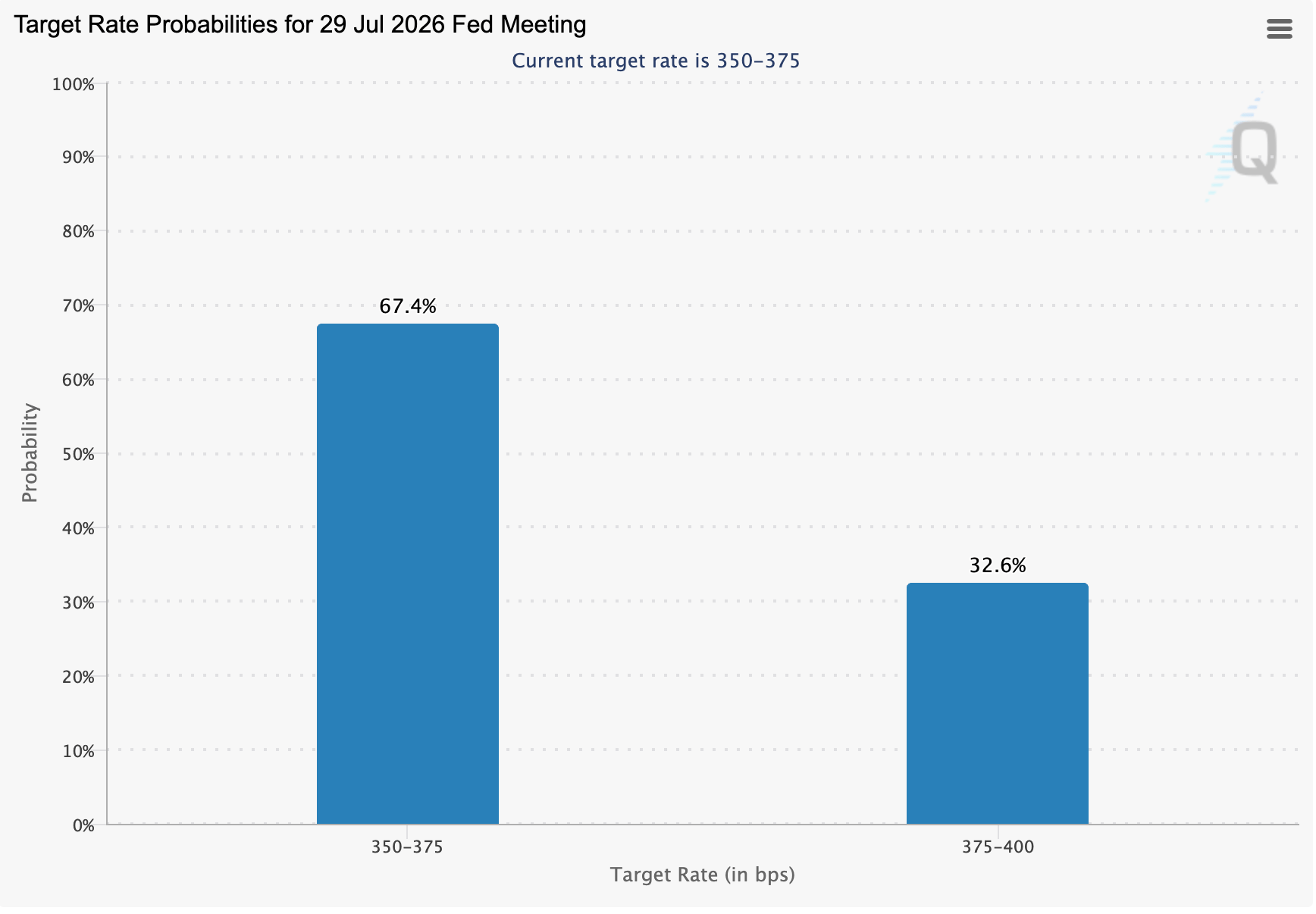

Data from the CME Group’s Fedwatch Tool shows that futures markets are pricing a 30% chance of a rate hike at next month’s Federal Open Market Committee (FOMC) meeting, and a more than 60% chance of monetary tightening in September, up from 6% and 20% respectively a month ago. This week’s employment figures will be analysed to contrast these views.

When will the JOLTS report be released and how could it affect EUR/USD?

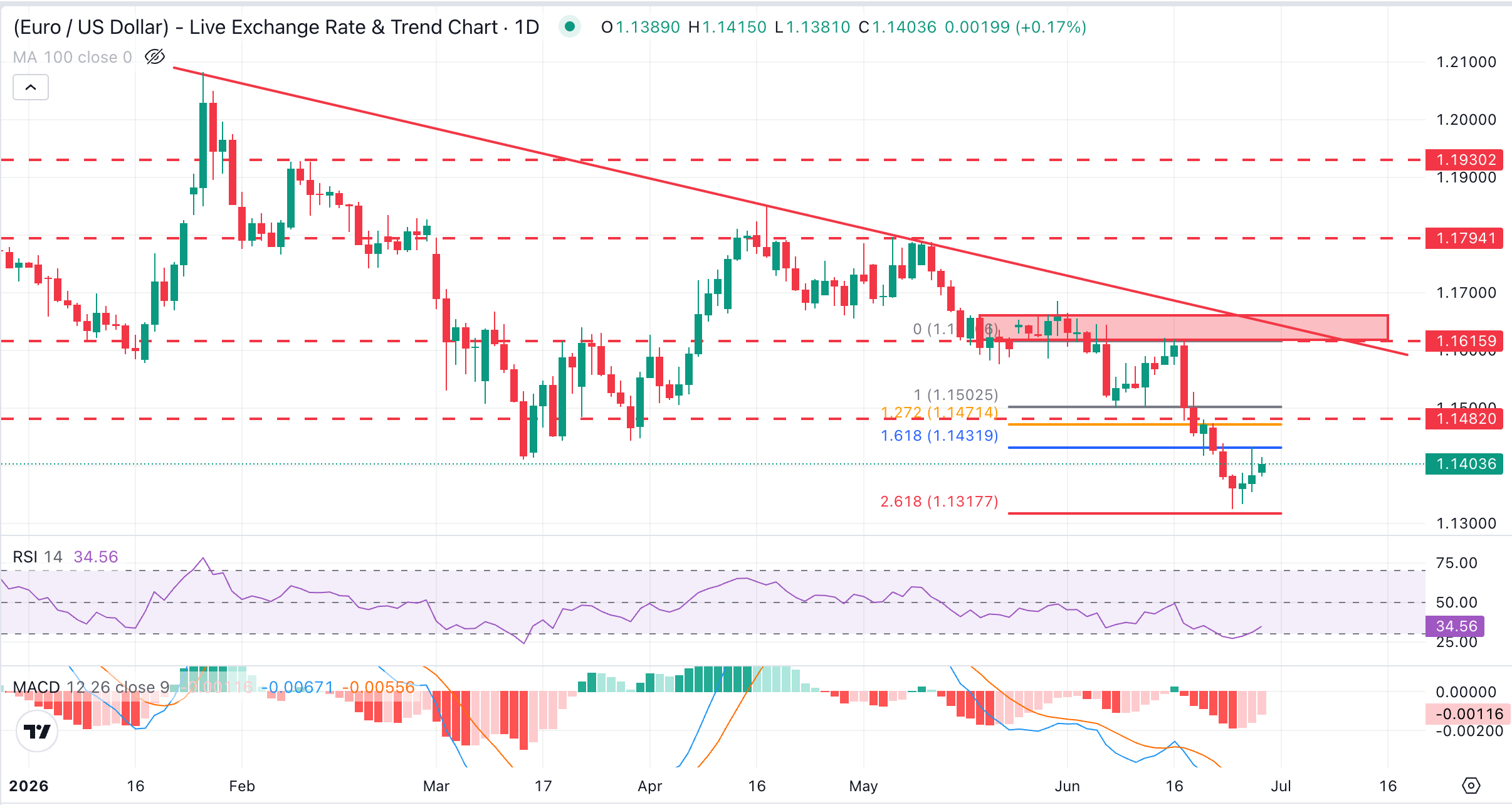

Job Openings will be published on Tuesday at 15:00 GMT. The EUR/USD is trading at a relatively short distance from the 13-month lows, on track to a 2.17% sell-off in June, and a nearly 3% decline over the last two months.

Guillermo Alcalá, analyst at FXStreet, sees the pair skewed to the downside while the US economy keeps outperforming the Eurozone’s and Iran’s war keeps dampening risk appetite: “The Euro has remained vulnerable over the last two months amid geopolitical woes and a sluggish economic growth in the Eurozone. Unless the scenario changes significantly, Euro rallies are likely to offer good entry opportunities for sellers. The 13-month low at 1.1325 remains the key support level. Further down, bears might be tempted to revisit the late May 2025 low at 1.1210.”

To the upside, Alcala sees the 1.1500 and the 1.1620-1.1640 resistance areas as the main hurdles for bulls: “The pair is struggling to consolidate above 1.1400 at the time of writing in a rebound from the mentioned 13-month lows, which, so far, seems corrective. Bulls should break the 1.1500 area (June 8,11 lows) and preferably also the area between 1.1620 and 1.1640, where late May and early June highs meet the descending trendline from the year-to-date (YTD) highs, to break the negative structure.”

Central banks FAQs

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

Economic Indicator

JOLTS Job Openings

JOLTS Job Openings is a survey done by the US Bureau of Labor Statistics to help measure job vacancies. It collects data from employers including retailers, manufacturers and different offices each month.

Read more.Next release: Tue Jun 30, 2026 14:00

Frequency: Monthly

Consensus: 7.28M

Previous: 7.618M

Source: US Bureau of Labor Statistics

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.