Cheniere Energy Q2 earnings beat estimates, revenues up Y/Y

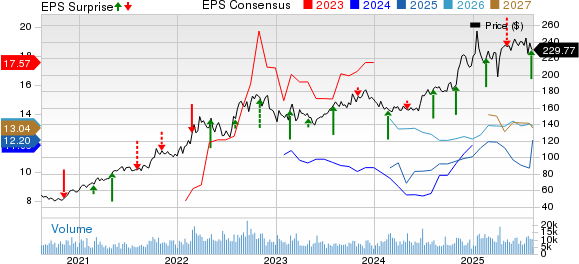

Cheniere Energy, Inc. reported second-quarter 2025 adjusted profit of $7.30 per share, which beat the Zacks Consensus Estimate of $2.30. The bottom line also increased from the year-ago quarter’s level of $3.84, primarily driven by favorable changes in derivative valuations, higher LNG margins from improved pricing and stronger LNG sales revenues supported by robust operational performance.

Revenues totaled $4.6 billion, beating the Zacks Consensus Estimate of $4.1 billion and increasing 43% from the year-ago quarter’s level of $3.3 billion, driven by a more than 45% jump in LNG sales.

In June 2025, Cheniere announced a second-quarter dividend of 50 cents per share of common stock, scheduled for payment on Aug. 18. That same month, the company also revealed plans, pending approval from its board of directors, to raise quarterly dividend by more than 10%, moving from an annualized rate of $2 to $2.22 per share, starting with the third quarter of 2025.

The oil and gas storage and transportation company reported consolidated adjusted EBITDA of $1.4 billion in the second quarter of 2025, up about 7.1% from the year-ago quarter’s level. The growth was primarily driven by an improvement in total margins per MMBtu of LNG shipped in 2025 compared with the corresponding period in 2024.

Distributable cash flow was $0.9 billion. In the reported quarter, the company shipped 154 cargoes compared with 155 in the year-ago period.

In June 2025, Cheniere finalized its decision to proceed with the CCL Midscale Trains 8 & 9 Project and, on June 18, authorized Bechtel Energy to begin full-scale work. That month also marked the start of LNG production from Train 2 of the CCL Stage 3 Project, which reached substantial completion on Aug. 6, 2025.

Around the same time, Cheniere Partners updated its SPL Expansion Project filing with FERC, shifting to a two-stage plan featuring three liquefaction trains and related infrastructure, targeting peak capacity of up to 20 mtpa, including efficiency gains from debottlenecking. By July, the company initiated the FERC pre-filing process for the proposed CCL Stage 4 Expansion Project.

On the commercial side, in May 2025, Cheniere Marketing signed a 15-year Integrated Production Marketing contract with a subsidiary of Canadian Natural Resources, securing 140,000 MMBtu/day of natural gas starting in 2030. This supply will yield roughly 0.85 mtpa of LNG, which Cheniere will market. In August, the company entered into a long-term Sale and Purchase Agreement with JERA Co., Inc. for 1 mtpa of LNG from 2029 to 2050, priced against Henry Hub with an added fixed liquefaction fee.

During the second quarter and first half of 2025, Cheniere allocated approximately $1.3 billion and $2.6 billion, respectively, under its comprehensive capital allocation strategy. These funds were directed toward accretive growth initiatives, strengthening the balance sheet and enhancing shareholder returns. The company repurchased around 1.4 million shares for roughly $306 million during the second quarter and 3 million shares for about $656 million year to date. In addition, Cheniere reduced consolidated long-term debt by $300 million during the first six months of 2025.

Cheniere Energy, Inc. price, consensus and EPS surprise

Cheniere Energy, Inc. price-consensus-eps-surprise-chart | Cheniere Energy, Inc. Quote

LNG’s costs and balance sheet

Costs and expenses amounted to $2.1 billion for the second quarter, up 26.9% from the prior-year quarter’s level.

As of June 30, 2025, Cheniere had approximately $1.6 billion of cash and cash equivalents. Its net long-term debt amounted to $22.5 billion, with a debt-to-capitalization of 66.2%.

LNG’s 2025 guidance

LNG expects a full-year 2025 consolidated adjusted EBITDA guidance of $6.6 billion to $7 billion, an update from the previous range of $6.5 billion to $7 billion. The company also anticipates a raised and adjusted guidance for distributable cash flow to a new range of $4.4 billion to $4.8 billion, from $4.1 billion to $4.6 billion expected earlier.

In June 2025, the company released an updated long-term estimate, predicting a more than 10% increase in run-rate LNG production. This outlook factors in the CCL Midscale Trains 8 & 9 Project along with debottlenecking initiatives. Cheniere also extended and expanded its capital allocation commitments, aiming to maintain investment-grade credit metrics through various market cycles, deliver increased returns to shareholders and continue investing in profitable growth opportunities. The company expects these initiatives to generate over $25 billion in available cash by 2030, equivalent to more than $25 per share in run-rate distributable cash flow.

LNG currently carries a Zacks Rank #3 (Hold).

Important earnings at a glance

While we have discussed LNG’s second-quarter results in detail, let us take a look at three other key reports in this space.

San Antonio, TX-based oil and gas refining and marketing service provider, Valero Energy Corporation (VLO), reported second-quarter 2025 adjusted earnings of $2.28 per share, which beat the Zacks Consensus Estimate of $1.73. However, the bottom line declined from the year-ago quarter’s level of $2.71. The better-than-expected quarterly results can be attributed to an increase in refining margins per barrel of throughput and lower total cost of sales. The positives were partially offset by a decline in refining throughput volumes and renewable diesel sales volumes.

The company had cash and cash equivalents of $4.5 billion at the end of the second quarter. As of June 30, 2025, it had a total debt of $8.4 billion and finance-lease obligations of $2.3 billion.

Houston, TX-based oil and gas equipment and services provider, Halliburton Company(HAL), reported second-quarter 2025 adjusted net income of 55 cents per share, which was in line with the Zacks Consensus Estimate but below the year-ago quarter’s profit of 80 cents (adjusted). The numbers reflect softer activity in the North American region, partly offset by international growth.

As of June 30, 2025, the company had approximately $2 billion in cash/cash equivalents and $7.2 billion in long-term debt, representing a debt-to-capitalization ratio of 40.4. Halliburton reported second-quarter capital expenditure of $354 million, up from our projection of $338.2 million.

Norway-based integrated oil and gas operator, Equinor ASA (EQNR), reported second-quarter 2025 adjusted earnings per share of 64 cents, which missed the Zacks Consensus Estimate of 66 cents. The bottom line declined 25% from the year-ago quarter’s level of 84 cents. Weak quarterly results can be attributed to lower liquids production across major segments and reduced liquids prices. Natural declines and portfolio divestments in Nigeria and Azerbaijan also contributed to the decrease in overall production.

As of June 30, 2025, the company reported $9,472 million in cash and cash equivalents. Its long-term debt was $24,505 million. During the same time, Equinor generated a negative net cash flow of $2,579 million compared with $4,022 million in the year-ago period. Equinor’s capital expenditures amounted to $3.4 billion in the second quarter.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.