AMD + OpenAI – Big deal, bigger expectations?

$AMD exploded higher in early October after announcing a strategic GPU supply partnership with OpenAI, jumping an eye-watering +37% in just days. But is this just the beginning — or is the “easy money” already made?

Let’s break it down.

What just happened?

On October 6, 2025, AMD and OpenAI signed a multi-year agreement that could reshape the AI infrastructure landscape:

-

OpenAI will deploy up to 6 gigawatts of AMD Instinct GPUs, starting with 1 GW in 2H 2026.

-

AMD issued warrants for 160 million shares (~10% of the company) to OpenAI — but these only vest if key supply and share price milestones are hit.

-

AMD claims the deal could generate “tens of billions” in revenue — with a potential $100B+ halo effect as new customers follow.

It’s AMD’s boldest move yet in its effort to compete with Nvidia in the AI GPU space — and the market took notice.

What’s priced in already?

The market was quick to reward AMD:

-

The +37% stock surge reflected sentiment, validation, and a realignment of AMD’s long-term narrative.

-

The news priced in AMD as a credible rival to Nvidia for AI compute at hyperscale.

-

It also acknowledged OpenAI’s potential to anchor AMD’s roadmap through tight collaboration — not just buy chips off the shelf.

But here’s the catch:

A deal announcement alone rarely justifies a near-vertical rally unless revenue traction is imminent.

At this point, investors have already “bought the news.” Now they need numbers.

What isn’t priced in yet?

This is where things get interesting. The deal could still be a multi-year catalyst — but only if AMD executes. What’s not fully priced in yet?

1. Revenue Conversion

We’ve heard big top-line numbers. But until AMD actually starts booking sales tied to OpenAI, the Street won’t fully rerate the stock.

Watch for:

-

Actual MI300X volume shipments in late 2026

-

Bookings appearing in guidance or earnings

-

Confirmation that AMD is hitting price/performance benchmarks.

2. Margins Hold or Improve

It’s not enough to win volume — AMD must scale profitably.

-

Yield, binning efficiency, memory cost, and cooling will all impact margins

-

If AMD maintains strong margins at hyperscale, it unlocks meaningful EPS leverage

3. Follow-On Wins

The OpenAI deal is a massive validator. If it leads to wins with Meta, Google, AWS, or Oracle, the upside broadens.

Right now, those follow-on deals are not priced in — and any announcements there would be fresh catalysts.

Now what? The “Quiet zone”

Here’s the issue: we may not get follow-through anytime soon.

-

Next earnings are likely months away

-

OpenAI GPU shipments don’t begin until 2H 2026

-

Warrant milestones aren’t immediate

-

No major new customers or product refreshes announced (yet)

That puts AMD in a “quiet zone” where bullish news flow slows and price may consolidate or correct.

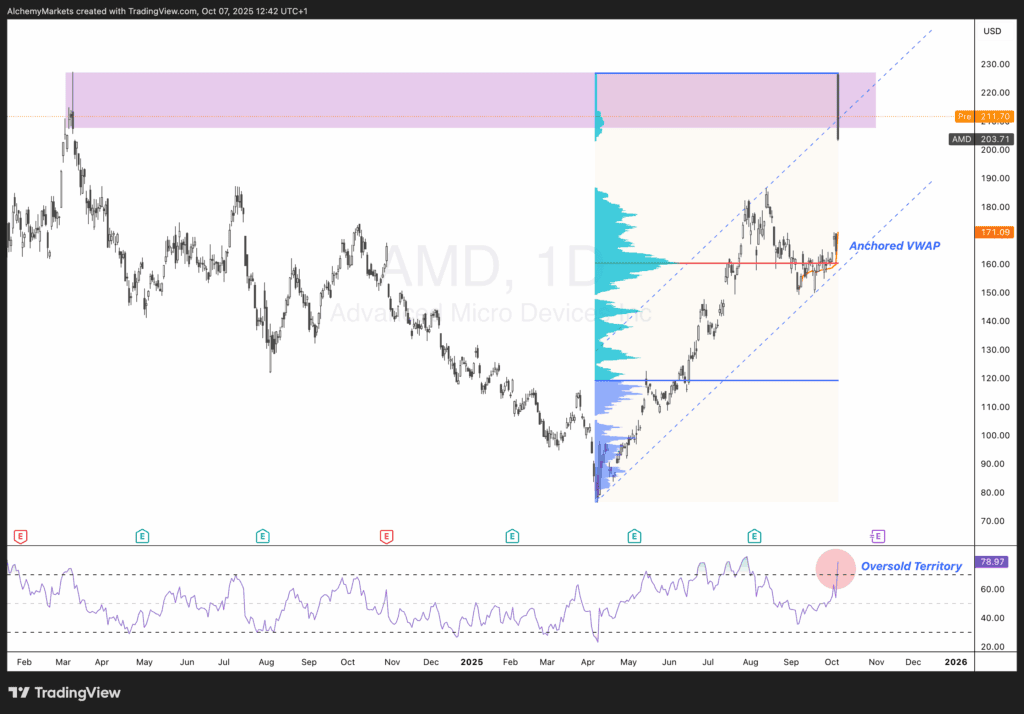

Technical view: Double top or just a pause?

Technically, AMD has now retested its March 2024 highs, forming what looks like a double top. But let’s not jump the gun:

-

It’s too early to trust the pattern without confirmation.

-

Instead, we treat the March 2024 resistance as a key level.

-

The April 2025 rally leg looks extended — and a pullback or consolidation could be healthy before fresh catalysts arrive.

Until real revenue shows up or a new hyperscale customer signs on, the stock may drift sideways or retest lower support zones.

Final take

AMD just landed the biggest deal in its AI history. It positions them as a real challenger to Nvidia — not just in GPUs, but in full-stack AI compute.

But with the stock up 37% in days and no near-term catalyst in sight, we may be due for a cooling-off period.

This story isn’t over — but it’s moved from “news-driven spike” to “prove-it phase.”

And the next phase of upside? That’ll depend on execution, revenue delivery, and new wins.

Until then, the sidelines might be the smarter place to wait for confirmation — or another breakout trigger.

Author

Zorrays Junaid

Alchemy Markets

Zorrays Junaid has extensive combined experience in the financial markets as a portfolio manager and trading coach. More recently, he is an Analyst with Alchemy Markets, and has contributed to DailyFX and Elliott Wave Forecast in the past.