How global interest rate shifts are creating new trading opportunities

Interest rates are the price of money. Everything else, like currency values, bond yields, equity multiples, and housing, gets priced around them. When central banks move, they move markets.

When central banks diverge, they move markets against each other. That's where trading gets interesting.

This article covers how rate differentials move currencies and how to trade them without blowing up on the risks that come with the territory.

How interest rates affect currency values

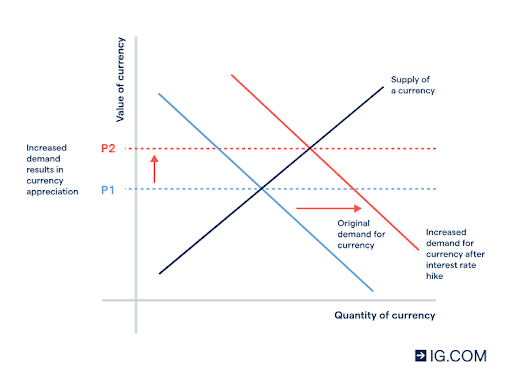

When one country's rates rise relative to others, money flows there, into bonds, money markets, and deposits. The currency strengthens. When rates fall or lag, the opposite happens, and it usually happens fast.

The dollar's run from 2022 into 2024 was a clean example.

The Fed hiked aggressively, held firm, and the broad trade-weighted dollar climbed.

USD/JPY reached multi-decade highs because U.S. yields towered over Japan's by several hundred basis points. That's the mechanism working exactly as expected.

The theory behind it, covered interest parity, mostly holds in practice, with deviations showing up mainly in funding costs and cross-currency basis during stress periods. For most FX traders, the simpler version is enough: follow the rate differential, and you understand the directional bias.

New trading opportunities from interest rate differentials

The Japan gap has been the standout setup for years.

USD/JPY and EUR/JPY moved aggressively and held their trends long enough that disciplined trend followers captured meaningful moves across a multi-year window.

The BoJ's slow normalization changes the arithmetic at the margins, but the spread is still wide enough to matter.

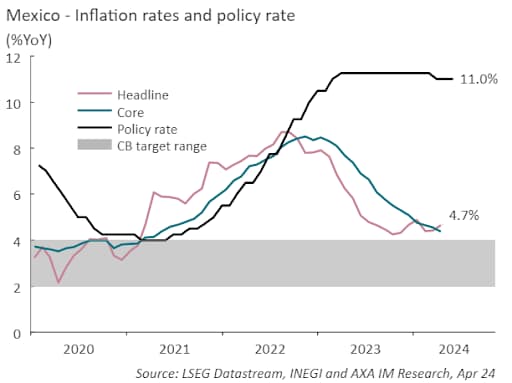

Beyond G10, Mexico's Banxico held its policy rate above 11% through much of 2023 and early 2024.

Real yield at that level draws carry flows and creates MXN setups against funding currencies like JPY or CHF.

The SNB easing early reopens CHF as a viable funding leg again. None of this is exotic, it's differential math applied to what central banks are actually doing.

Where it gets more interesting is in the sequencing. The ECB cutting before the Fed implies the EUR softens against the dollar.

If the BoE lags both, GBP holds relative strength against EUR. Each central bank's path relative to the others generates a cross-currency matrix of setups, and right now that matrix is far less uniform than it was in 2021, when every major central bank was sitting at zero.

Strategies to capitalize on interest rate shifts

The most straightforward approach is the carry trade: borrow cheap in a low-yield currency like JPY, CHF, and buy into something yielding more, collecting the differential while you hold.

The math is simple. The risk isn't.

Carry trades don't fail slowly. A risk-off event, a central bank surprise, or a geopolitical shock can unwind months of accumulated carry in hours. Capping single positions at 2-3% of capital isn't conservatism, it's arithmetic.

Brandy Hastings, SEO Strategist at SmartSites, helps businesses make data-driven decisions in constantly changing competitive environments.

She notes, "One of the biggest mistakes people make in any market is assuming a trend will continue simply because it has worked recently.

The strongest opportunities usually come from understanding what is driving the trend underneath. In interest-rate-driven markets, traders who focus on the underlying policy divergence tend to react faster than those watching price alone."

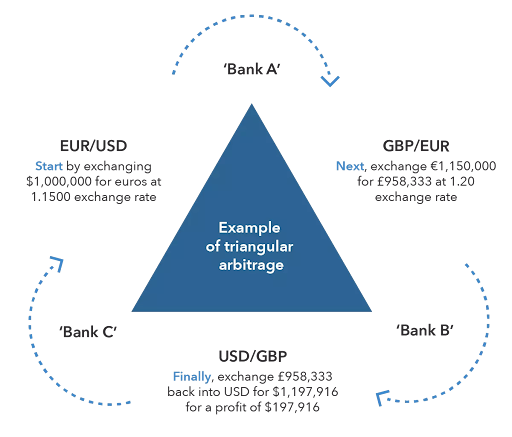

Interest rate arbitrage is mostly an institutional game, but it matters for how traders think about forward tenors.

Covered interest parity breaks down in predictable ways during funding stress, and the cross-currency basis widens in ways that don't show up in the spot price. If you're holding longer-dated forward positions, that basis eats into expected returns quietly.

Forward rate agreements and swaps are more useful as risk management tools than speculative ones for most traders.

If you're long EUR/USD and think the ECB cuts faster than the market has priced, you can layer in a rate swap to hedge the euro rate leg without disturbing the spot position.

The instrument is useful, but only if you understand the mechanics and margining before you use it.

Risks and considerations in interest rate-based trading

The central bank pivot risk is real, and it moves fast.

A single CPI print, hawkish meeting minutes, or a surprise cut when the market had priced a hold, can move a major pair 100-200 pips in minutes, and carry positions that looked well-constructed on Monday look different by Thursday afternoon.

Intervention risk is harder to hedge.

Japan's Ministry of Finance stepped into USD/JPY multiple times across 2022-2024, and those episodes are violent.

The MoF publishes intervention disclosures, but after the fact, by the time it's official, it's already happened to your position.

The SNB's 2015 removal of the EUR/CHF floor was the extreme version: the pair moved over 1000 pips in minutes, leveraged carry positions were wiped, and several retail brokers couldn't cover client losses and became insolvent.

That was a regime change, not a routine adjustment, but it's the clearest illustration of what central bank surprise looks like at full amplitude.

So what actually helps?

Diversifying across pairs means one shock doesn't crater the whole book.

Options overlays cap tail risk cheaply when volatility is low, which is usually when you want to buy them, not after the event.

Position sizes small enough to survive a whipsaw matter more than any single trade's upside. And central bank calendars, speeches, and minutes are worth reading closely.

Rawad Baroud, CEO of ZeroGPT, runs an AI-powered platform focused on analyzing and interpreting large volumes of content and language data.

He shares, "Markets often react to subtle shifts in language long before they react to official decisions.

Traders who pay attention to changes in tone, risk assessments, and forward guidance can sometimes identify turning points before they appear in economic data or price action."

Policymakers usually signal the direction of the next surprise before it arrives, if you're paying attention to the language rather than just the headline decision.

Real-world examples of trading success and failures

USD/JPY from 2022 through 2024 was a trend trade with clean fundamental backing. The Fed hiked, the BoJ held, the rate differential widened, and the pair climbed to multi-decade highs.

Traders who got long early, sized correctly, and rolled forward positions collected both carry income and spot appreciation across a multi-year move. The data is in FRED's USD/JPY series, you can see exactly how it tracked the rate spread.

The 2015 CHF shock is the case study that should be required reading for anyone trading carry.

EUR/CHF had sat near the 1.20 floor for years, the SNB had defended it repeatedly, and the carry trade against CHF had looked reliable for long enough that traders stopped treating it as a risk.

Then, on January 15, 2015, the SNB released a statement removing the floor. CHF surged. Leveraged positions were wiped. The SNB's press release from that day is public and short. Read it.

MXN in 2023-2024 was the most instructive middle case. The high real yield supported the currency, and the carry worked, but there were sharp drawdowns during risk-off windows.

Traders who sized for volatility and used those drawdowns as re-entry points came out ahead. The ones who sized for smooth carry accrual and ignored drawdown risk got stopped out at the wrong moment and missed the recovery.

The road ahead

Central banks are not moving together and won't be for a while. Inflation is cooling unevenly. Growth is uneven.

Japan's normalization is deliberate and slow. The ECB and BoC are in easing mode while the Fed watches its own data. That's a matrix of divergences at different stages, each generating its own setups and its own risks.

Watch the spreads between front-end yields in your pairs.

Track forward points as they price the differential directly and tell you what the market has already priced in versus what you think is coming. When central bankers shift their language around risks, they're usually signaling which direction the next surprise comes from.

Author