Will the BOJ Bring a Trick or a Treat for GBP/JPY?

Kicking off the busy turn-of-the-month week for economic data, the Bank of Japan will conclude its monetary policy meeting early in Wednesday’s Asian session.

In part because the central bank made no major changes to last week’s Financial System Report, traders and economists are expecting no change to monetary policy. That said, it is worth noting that the BOJ, Finance Ministry and FSA held a joint meeting earlier this week to discuss the sharp drop in capital markets, so it’s clear that policymakers are paying close attention to the recent market turmoil.

Beyond capital market volatility, escalating trade tensions and stubbornly low inflation will be key topics for the central bank. Though US President Trump’s trade ire remains focused on China, Japan’s export-reliant economy is vulnerable to a slowdown if protectionist actions in the US and elsewhere lead to a coordinated global slowdown in trade. Meanwhile, the BOJ switched from heavy asset buying to a longer-term “yield curve control” policy to stimulate price pressures back in 2016; early evidence of the policy’s success is mixed, but global demand for Japanese goods remains generally strong for now, so the central bank is unlikely to make any changes this time around.

Finally, traders will be watching the latest release of the BOJ’s quarterly economic projections. The most recent forecasts, made in July, expected core consumer inflation to hit 1.1 percent in the year ending in March 2019 and accelerate to 1.5 percent the following year. Any negative revisions to these projections could lead to yen weakness.

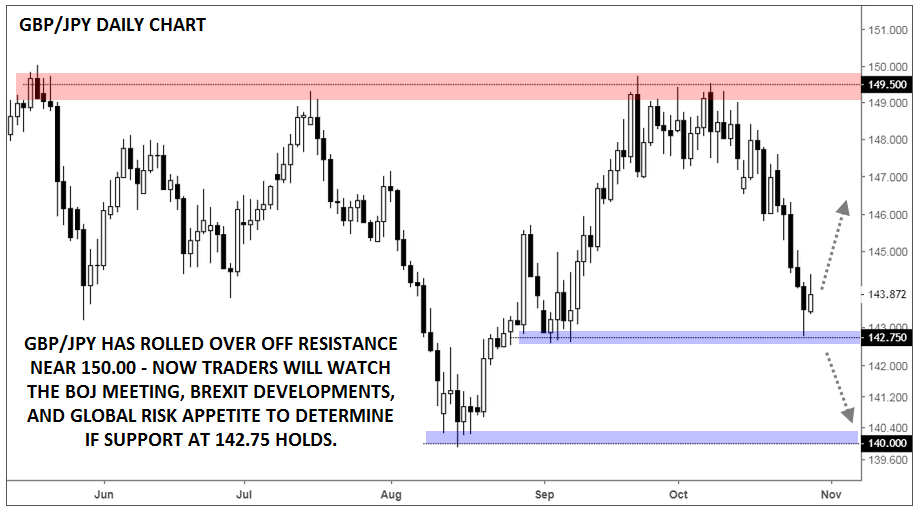

Technical View: GBP/JPY

My colleague Fawad Razaqzada outlined the technical outlook for USD/JPY last week (see “USD/JPY threatening bullish trend as stocks tank” for more), and that pair continues to flirt with its bullish trend line as of writing. Turning our attention to GBP/JPY, rates have rolled over off strong previous resistance near 150.00 to test the early-September support at 142.75.

Looking forward, idiosyncratic developments, such as the BOJ meeting and Brexit headlines, will obviously have a big impact GBP/JPY, but the pair is also likely to move in-line with broader risk sentiment.

In other words, if global equity markets extend their recent selloff, GBP/JPY could break through last week’s trough at 142.75, opening the door for a continuation down to the 1-year low near 140.00 next. Meanwhile, a recovery in global risk appetite could prompt the notoriously highly-volatile pair to bounce back toward 146.00 or higher in the next week or two.

Author

Matt Weller, CFA, CMT

Faraday Research

Matthew is a former Senior Market Analyst at Forex.com whose research is regularly quoted in The Wall Street Journal, Bloomberg and Reuters. Based in the US, Matthew provides live trading recommendations during US market hours, c