Why the Bank of England can relax about inflation

Services inflation, a key indicator for the Bank of England, should fall much closer to 4% by June. Wage growth should continue to ease off too, and if we're right, that would enable the Bank to take rates lower than markets currently expect.

April's data is likely to be crazy

Brace yourselves. April is always a crazy month for UK inflation. And this year’s data, released on 21 May, is set to be even crazier.

Everything from energy price hikes and a 25% increase in water bills (ouch) to substantial rises in new car road tax looks set to take headline inflation almost a percentage point higher from the 2.6% rate recorded in March.

And those are the things we know about. The services basket, which the Bank of England ultimately cares about most, is affected by a whole swathe of annual price hikes at the start of the financial year in April. Phone and internet bills are the most prominent example, but plenty of things are affected.

In theory, the fact that headline inflation has been lower over recent months than it was twelve months earlier, should mean these annual price resets are less aggressive than last April. That doesn't seem to have always been the case in practice though, and the steep rises in both employers' taxation and the National Living Wage could add extra upward pressure. The timing of Easter adds an extra layer of potential volatility too.

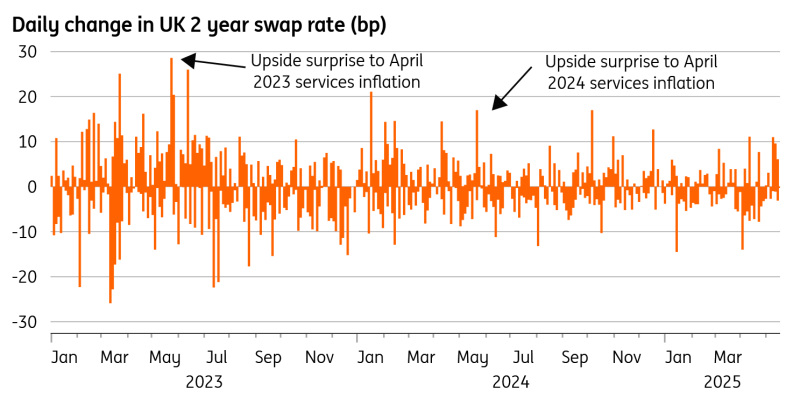

April’s numbers have proven to be highly unpredictable. Two years ago, the release of that month’s data triggered the biggest one-day repricing of Bank of England expectations of the whole of 2023. Last year’s April numbers triggered the joint-second largest move.

April's data has a habit of triggering big market reactions

Source: Macrobond, ING

Services inflation should come lower

The Bank of England is certainly wary. Markets had expected officials to signal a faster pace of easing at the most recent May meeting. The fact that they didn’t, we think, was partially because policymakers didn’t want to prejudge the April inflation data.

That said, and for what it’s worth, we think this year's April services inflation could come in lower than most expect. The BoE is forecasting 5%. We’re predicting 4.7/4.8%, though we wouldn’t bet too heavily on it.

Whatever happens, though, we think the news on services inflation is about to get better. We believe it will be half a percentage point lower by June (roughly 4.2%), well below the BoE’s forecasts, which see it hovering around 5% into the summer.

A decent chunk of this can be traced back to rents, which have been contributing more than a percentage point to services inflation. That contribution is likely to halve by the start of next year.

Private rental growth is currently running at almost 8%, but that includes existing rents, which tend to reflect wider rental market developments with a lag. We know that price increases on new tenancies are becoming much less aggressive, and that should begin to feed through to the overall rental inflation series.

Then there’s the third of rents that are social or local authority-owned, which are subject to a cap on annual price rises. The government has already announced that this cap is much lower this year. In the last fiscal year, they were allowed to rise by almost 8%. This year, it is less than 3%. These prices are updated in CPI once per quarter, so the full effect of this won’t show up until July.

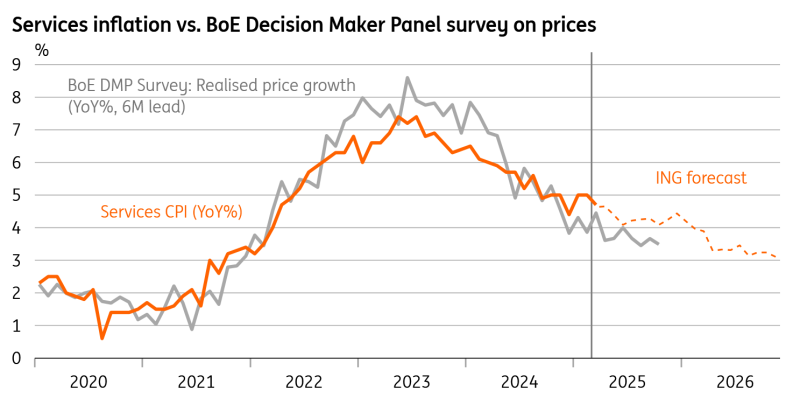

The BoE's decision maker survey points to lower services inflation

Source: Macrobond, ING

More generally, though, pricing power seems to be fading. The Bank’s Decision Maker Panel, which we know policymakers put a lot of weight upon, has shown a consistent drop in realised price growth over the past few months. That’s a decent lead indicator for services inflation, and were it not for some of the regulated price increases and sticky rents, it says it should be heading below 4%.

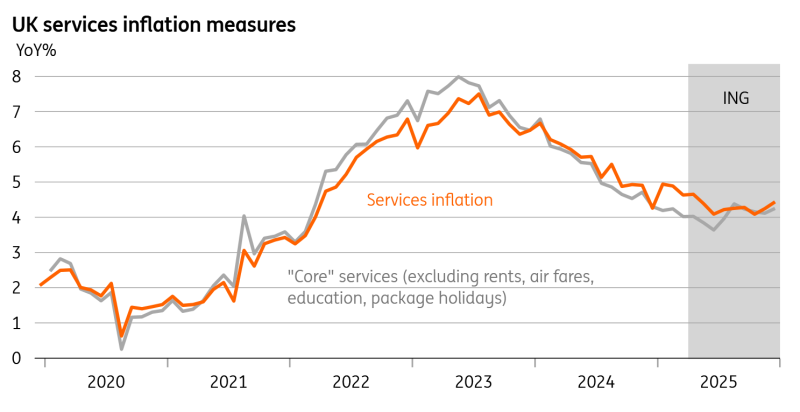

Arguably, this is already happening. If we calculate ‘core services’ inflation, which strips out volatile stuff like air fares, holidays, and rents, this is already tracking at 4% and is likely to head lower over the next few months.

'Core services' inflation set to fall below 4%

Source: Macrobond, ING

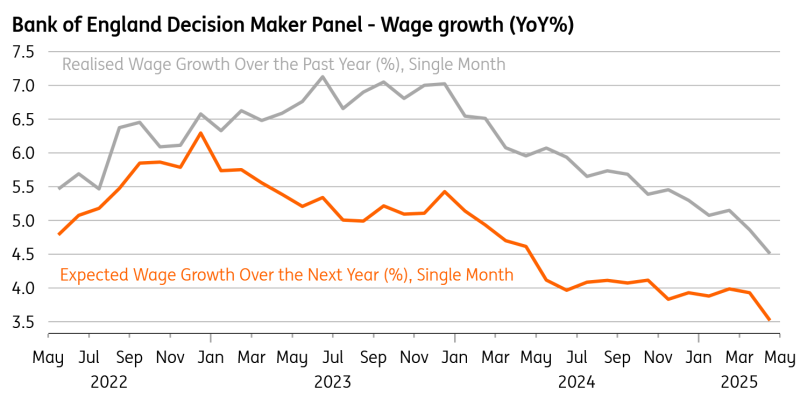

There are hints of better news on wage growth

That may all be true, but the Bank’s hawks would argue that wage growth is also much too high. At 5.6%, annual pay growth in the private sector is much higher than it should be, given how much the jobs market has cooled over the past couple of years.

Even here, though, the news is slowly getting better. The three-month annualised rate of private-sector wage growth – a better measure of recent momentum - is now 3%. And the BoE’s DMP survey suggests firms are tapering their pay rises.

The Bank will want to see more evidence of this cooling in the official data before becoming more confident on the wage story – particularly given the steep rise in the National Living Wage that’s recently kicked in. But this is a strategy that is not without risk.

Wages are just about the most backward-looking way of examining the economy. And we know that the vacancy rate is now below pre-Covid levels, a time where wage growth was closer to 3.5-4%. Recent tax hikes, fortunately, haven’t caused the spike in layoffs some of the surveys had hinted at, but hiring expectations have nevertheless cooled a lot.

Wage growth expectations are cooling off

Source: Macrobond

Could the bank speed up the pace of cuts?

In short, the Bank of England should - pretty quickly - become more relaxed about the inflation story.

Admittedly the bar for a June rate cut is set pretty high. We think the next move is much more likely in August, and our expectation is that the once-per-quarter pace of cuts continues through this year and into the next.

We don’t rule out a faster pace of easing. However, we think this more dovish inflation story is more likely to be reflected in a lower end-point for Bank Rate. Markets are pricing the terminal rate at 3.7%; we're expecting rates to eventually fall to 3.25%.

Read the original analysis: Why the Bank of England can relax about inflation

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.