When will the Fed “normalize” interest rates? This is normal

A drug addict constantly needs more drug to get the same effect.

The U.S. economy is addicted to easy money, and it needs more and more of this drug to maintain the high.

The problem with this scenario is eventually the addict overdoses.

This is normal

During its July meeting, the Federal Reserve signaled that a rate cut is likely in September. In his post-meeting press conference, Jerome Powell said, "If we were to see inflation moving down ... more or less in line with expectations, growth remains reasonably strong, and the labor market remains consistent with current conditions, then I think a rate cut could be on the table at the September meeting."

But a lot of people aren’t satisfied with the promise of an interest rate cut soon. They want it now!

An article headlined “Markets are clamoring for the Fed to start cutting soon: ‘What is it they’re looking for?’” published by CNBC after the July FOMC meeting highlighted the frustration of those who believe the Federal Reserve has kept rates too high for too long.

The article quotes New Century Advisors chief economist Claudia Sahm. She goes on to insist, “The Fed needs to start that process back gradually to normal, which means gradually reducing interest rates.”

This raises a question: what is normal.

Well, this is!

Or at least the current rate environment is closer to normal than the artificially suppressed interest rates the markets have feasted on for the most part since the 2008 financial crisis.

In the wake of the financial crisis, the Federal Reserve slashed interest rates to zero. It was an unprecedented move justified by an “unprecedented” emergency. Little did anybody know that the “emergency” would last for seven years!

The Fed didn’t move rates off zero until December of 2015 with a quarter percent hike. And then it waited a full year before it hiked again.

The central bank finally started hiking rates in earnest in 2017, pushing rates to 2.5 percent by December 2018.

And that was the end of “normalizing” interest rates.

But this was nowhere near normal. During the cycle prior to the Great Recession, rates peaked at 5.25 percent (June 2016).

In the fall of 2018, with his drug supply limited, the addict threw a fit. He wanted his easy money drug back. The stock market crashed, and the economy started showing signs of recession. To avoid the pain of withdrawal, the pusher (the Fed) started supplying the drug again. It cut rates three times in 2019 and abandoned balance sheet reduction.

Then came COVID-19. The pandemic gave the Fed the excuse it needed to fill the easy money syringe to the top. Rates went back to zero until price inflation inevitably reared its ugly head.

This rate history lesson illustrates a point.

The economy needs more and more easy money every single cycle. The threshold for “normal” gets lower and lower – meaning more and more of the easy money drug.

That’s why everybody is clamoring for rate cuts today. The addict is on the verge of withdrawal. He wants his drug supply to go back to normal – the new normal.

What is a normal interest rate?

It’s difficult to define “normal” when it comes to interest rates.

Interest rates are a price – the price of borrowing money. In a sane world, the market would set the interest rate in the same way it sets the price of cell phones or milk. But we don’t live in a sane world. We live in a world where central planners try to “set” rates. If we allowed the market to function, we would know exactly what “normal” means.

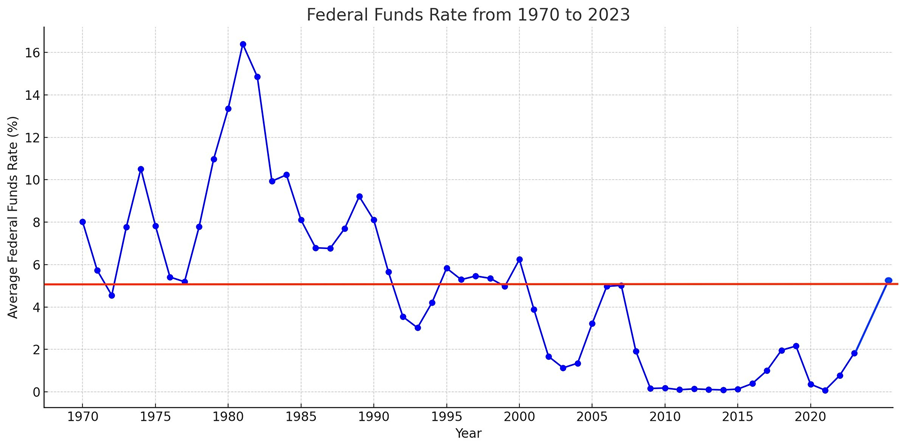

But we can look at averages, and historically, the average federal funds rate since 1970 has been 4.95 percent. That’s basically where we are today. From a historical perspective, this is normal. And yet Sahm and many others are pleading for the Fed to start “normalizing” rates.

And if you factor out the nearly 15 years of artificially low rates in the wake of the 2008 financial crisis, you discover that rates today are a little below normal. The average federal funds rate from 1970 to 2007 was 6.74 percent.

A chart of the trajectory of the federal funds rate over time makes it clear what’s happening. Every cycle, the Fed delivers more of the easy money drug fueling a boom. And once ensuing the bust passes, the peak interest rate in the next cycle ratchets lower and lower.

As the addict builds up resistance to the drug, it needs more and more to maintain the high and can tolerate less of a taper when the party gets out of control.

This is an example of what economist Robert Higgs termed “the ratchet effect.”

Higgs argued that during times of national emergency, such as wars or severe economic downturns, governments expand their authority and intervention in the economy, often justified by the need to address the crisis. After the crisis passes, the government eases the intervention, but it never returns to the “normal” before the emergency. The overall size and scope of government remain larger than before the crisis. This ratchet effect leads to a long-term trend of increasing government intervention over time, as each crisis creates a new baseline for government intervention that is higher than before.

Fed interest rate policy shows a negative ratchet effect. After each crisis, the baseline for “normal” interest rates gets lower and lower.

The problem with upping the dosage of drugs to maintain a high is that eventually, the addict overdoses.

So, how much more easy money can the Fed inject before the economy ODs?

The Fed has been reluctant to toy with negative interest rates. Instead, it has used the balance sheet to inject the easy money drug. The Fed pumped nearly $4 trillion into the economy during the Great Recession through quantitative easing. It upped the ante to nearly $5 trillion in QE injected in a much shorter timespan during the pandemic.

What’s next? $8 trillion in QE? $20 trillion?

The question becomes, when does the drug kill the addict?

The desperation for rate cuts is understandable

I completely understand why the markets are desperate for rate cuts. They want to keep the party going and the drugs flowing. Everybody knows that this debt-riddled bubble economy can’t function in a higher interest rate environment. Whether the current rate environment is “normal” or not, it’s not sustainable. The addict will go into withdrawal.

This is exactly what the economists quoted in the CNBC article tell us. DoubleLine CEO Jeffrey Gundlach said he thinks the Fed is “risking recession” by holding a “hard-line” on rates.

And he’s probably right.

But the Fed is also risking a resurrection of the inflation dragon if it starts cutting now.

This is called being stuck between a rock and a hard place.

The Fed can ramp up the party and risk an overdose (in the form of more rampant price inflation) or it can hold back the drugs and risk a painful withdrawal.

Either way, the addict has a problem.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.