When euphoria ends, gold bulls enter the scene

Market participants are very optimistic about an economic recovery, but these positive expectations may be exaggerated. The end of this euphoria should be good for gold.

The optimism about the pace of economic recovery from the 2020 recession is growing. The analysts race in upward revisions of GDP growth in the coming quarters. For example, the IMF – in the April 2021 edition of the World Economic Outlook – expects at the moment that the US economic output will increase by 6.4% this year, compared to the 5.1% growth forecasted in January.

The euphoric mood has some justification, of course. The vaccination is progressing, entrepreneurs are used to operating under sanitary restrictions, economies are reopening and governments are spending like crazy. At the same time, central banks are maintaining ultra-easy monetary policy, keeping financial conditions loose.

Furthermore, some economic data is consistent with strong rebounding, especially in manufacturing. For instance, the IHS Markit U.S. Manufacturing PMI Index posted 59.1 in March, up from 58.6 in February – being the second-highest value on record since May 2007 when data collection began. Services are also recovering vigorously, as the IHS Markit US Services PMI Index registered 60.4 in March, up from 59.8 in February. It’s the fastest rate of growth since July 2014.

Now, the question is how strong the current boom is and how long it is going to last. Well, there is no need to argue that we will see a few strong quarters of GDP growth in the US and other countries. But for me, the euphoria is exaggerated. You see, the current recovery is not surprising at all. As the Great Lockdown plunged the world into a deep economic crisis , the Great Unlocking is boosting the global economy.

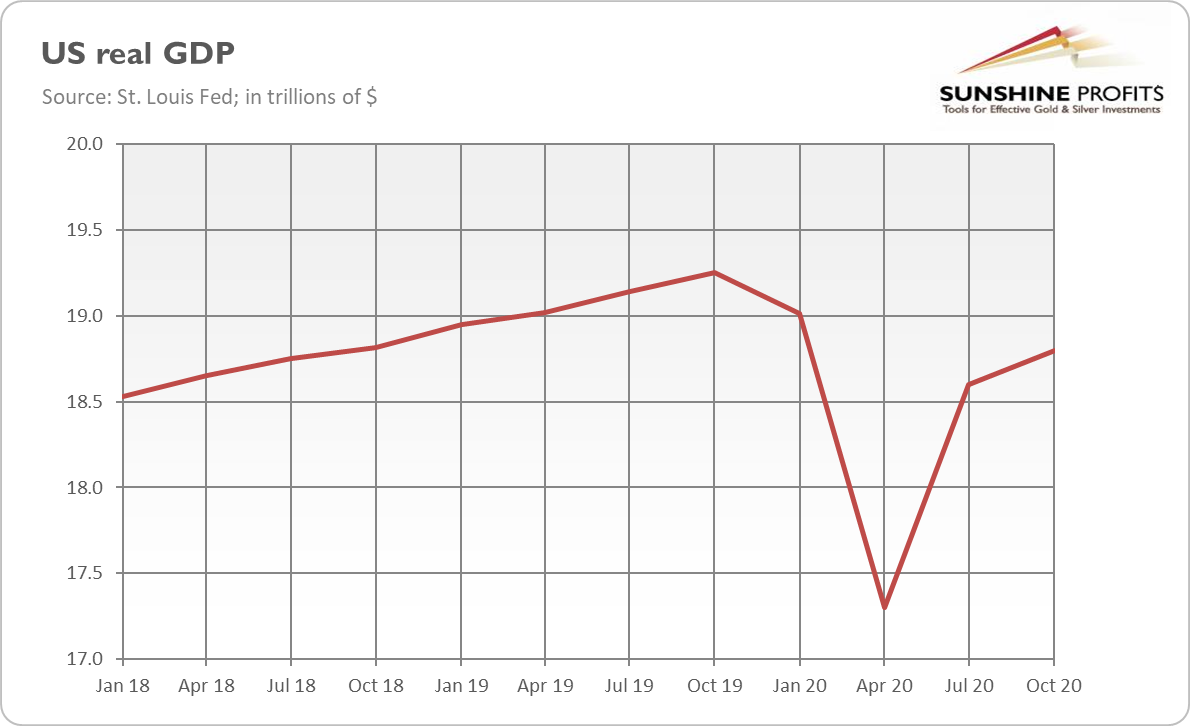

And there is the base effect. There was a low base in 2020, so the seemingly impressive recovery in 2020 is partially merely a statistical phenomenon. Let’s illustrate this effect. In Q2 2020, the real GDP plunged from $19,020 to $17,302 trillion or 9.03%year-over-year, as the chart below shows.

However, the rebound to the pre-recession level would imply the jump of 9.93%, almost one percentage higher! This is how the math works: when you divide a numerator by a smaller denominator, you get a greater percentage. So, it would be alarming if the recovery were not strong after one of the deepest crises in history.

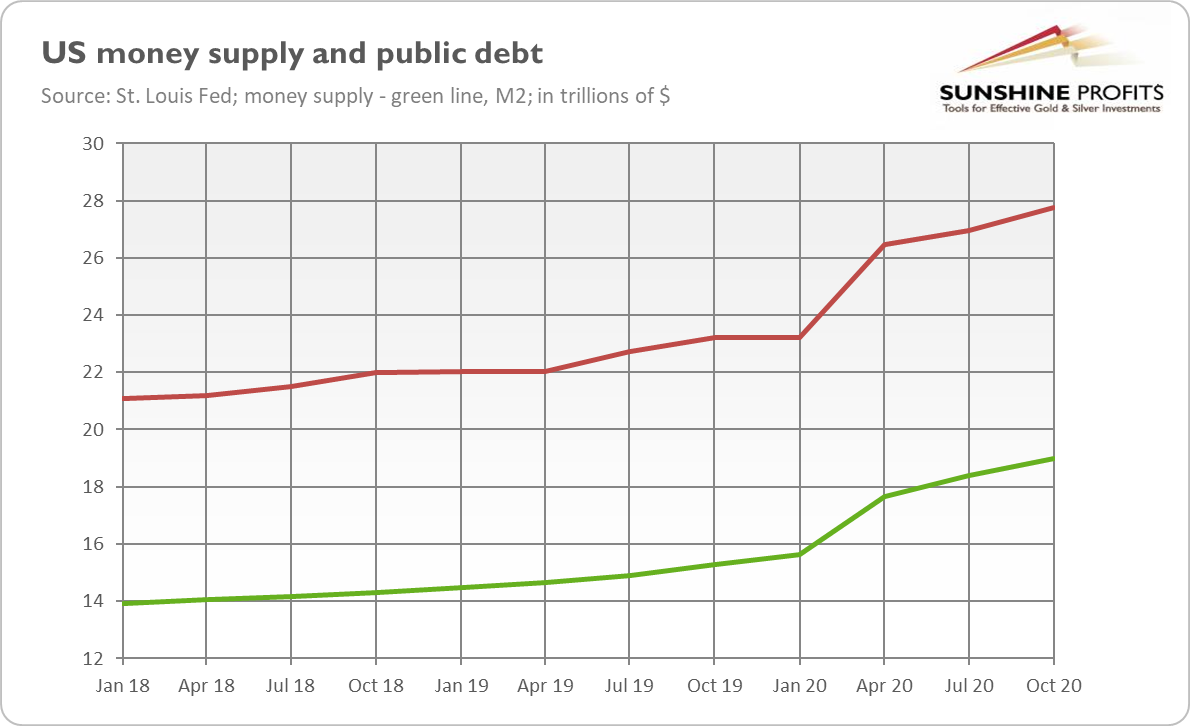

Another issue that makes me more skeptical than most pundits is the fact that the main reason behind economic growth upgrades is massive fiscal stimulus . Uncle Sam injected more than 13 percent of the GDP in government spending (only in 2020) that ballooned the fiscal deficits . Meanwhile, the Fed widened its balance sheet by almost $4 trillion. So, it would be quite strange if we didn’t see impressive numbers in light of such unprecedented inflows of monetary and fiscal liquidity. But it means that the impressive recovery in statistics is driven, at least partially, by soaring money supply and public debt (see the chart below).

And my three last concerns. First, the job recovery is more sluggish than the GDP recovery. The unemployment rate is still above the pre-pandemic level, while the labor force participation stands significantly below the level seen in February 2020. Second, a full return to normal life will occur if vaccines remain effective. But there is a tail risk of new variants of the virus, which could even be vaccine-resistant . Third, history teaches us that when the pandemic ends, social unrest may reemerge. After all, the epidemic left us with deepening inequalities and rising living costs.

What does it all mean for the gold market? Well, the market euphoria about the economic rebound is negative for gold. We have already seen how these optimistic expectations freed the risk appetite and boosted economic confidence, sending bond yields higher, but gold prices lower.

However, just as the doomsday scenarios created in the midst of the epidemic were excessively negative, the current ones seem to be too optimistic. I expect that with the year progressing, these expectations will soften or shift to the medium-term, which could be more challenging. After all, the low base effect will disappear, and both the monetary and fiscal policies will have declining marginal utility. At the same time, there will be an increased risk of high inflation, debt crisis, stock market correction or even financial crisis . After all, the current levels of stock indices are partially caused not by fundamentals, but by the elevating risk tolerance thanks to the central banks standing behind most asset classes ready to intervene in case of problems.

It seems that this process has already begun and the reopening trade is waning. Economic confidence is very high, so the room for further increases is limited. The low-hanging fruits have been collected, and when economies reopen fully, the structural problems will become more important than the cyclical ones. Investors have started to worry about higher inflation, especially because the Fed remains unmoved by rising prices. A jobless recovery would prolong the Fed’s very dovish stance , as the US central bank focuses now on full employment rather than on stable prices. All these factors explain why the price of gold has been rebounding recently, and why it can rise even further later this year , although the fact that the US enjoys a stronger recovery than the EU or Japan could support the interest rates and the greenback , creating some downward pressure on the yellow metal.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Arkadiusz Sieroń

Sunshine Profits

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017.