What the end of Riksbank’s FX sales means for the Krona

We estimate that the Riksbank’s FX sales will end by early February, leaving the krona without this artificial support (worth around 2-3% vs EUR, on our estimates) which has fuelled SEK gains since late September. We cannot exclude more FX sales should SEK sell off materially, but our base case is that SEK will rise in 2024, although at a slower pace than NOK.

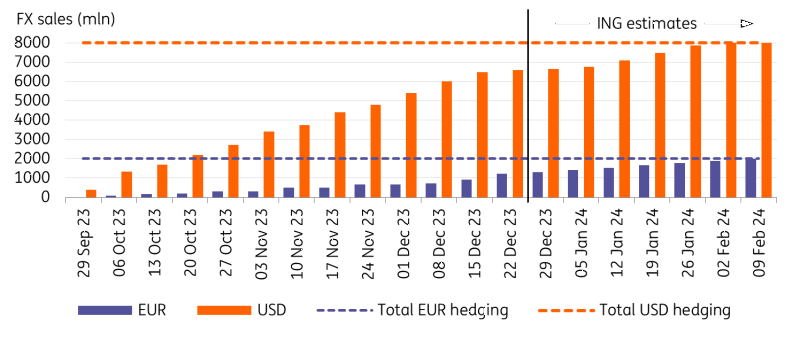

Riksbank’s hedging programme to end by early-February

We estimate that the Riksbank’s FX reserve hedging programme will end by early February. As shown in the chart below, the Riksbank has so far reported FX sales worth USD 6,600m and EUR 1,212m as of 22 December. The size of the programme is USD 8bn and EUR 2bn.

Based on the average pace of sales and accounting for lower volumes around the holiday season, we estimate that USD sales will end around the end of January or the first week of February. EUR sales (almost half of which have been carried out via EU payments) may be carried on for a couple of weeks longer.

ING's estimates of Riksbank's FX sales

Source: Riksbank, ING

FX sales have generated around 2-3% of extra EUR/SEK underperformance

We estimate that the Riksbank FX operations from 25 September 2023 until 08 January 2024 have generated SEK extra performance against EUR worth 2-3%. That is calculated by subtracting the estimated impact of traditional market drivers (2-year rate differential, relative equity performance, global risk sentiment and the relative shape of the yield curve) to the total performance of EUR/SEK in the period, which returns the (negative) premium that has emerged in the pair compared to the fair value-implied performance.

However, since EUR/SEK was overvalued before FX sales started, our best estimate for the net impact on SEK (vs EUR) of hedging operations is closer to 2.0%, which incidentally matches the current undervaluation of EUR/SEK to its short-term fair value.

EUR/SEK market-driven and FX-sales driven performance since start of hedging operations

-638404889076266336.PNG)

Source: Refinitiv, ING

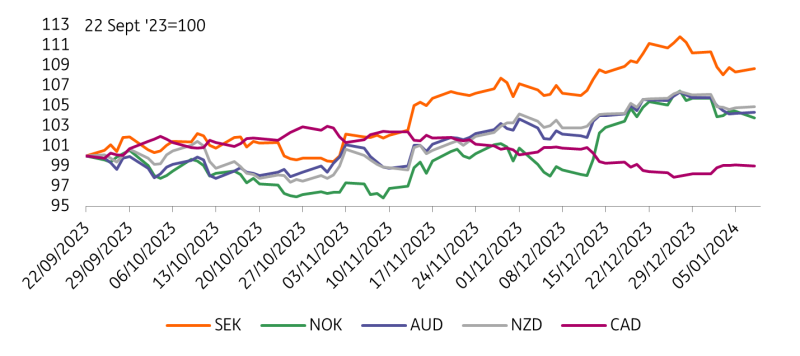

This means that once FX sales are discontinued around the end of January/early February (as per our estimates) there is a high risk that the krona will start to underperform other high-beta peers. Indeed, as shown below, SEK has been a strong performer among high-beta G10 currencies since FX reserve hedging started in November. In other words, we expect the 2% SEK positive premium to be trimmed.

SEK and other G10 high-beta FX since start of Riksbank FX sales

Source: Refinitiv, ING

Not our base case, but Riksbank can resume FX sales

Let’s remember that the Riksbank’s official reason for starting FX sales was to limit losses on its FX reserves ahead of a projected appreciation in the krona. As discussed on numerous occasions, FX sales have appeared more as covert interventions to strengthen SEK instead, or at least SEK appreciation has been a very welcome side effect of hedging operations.

To use the words of Vice Governor Aino Bunge: “The Riksbank does not have a target for the krona, we have a target for inflation. But the exchange rate affects the outlook for inflation and therefore we need to monitor it closely.” To us, this sounds like the Riksbank does have a target for the krona, and the way to chase it can be by expanding hedging operations after the USD 10bn and EUR 2bn thresholds are reached. The hedging programme has been successful at driving SEK higher, makes sense from a risk-management perspective (if the Riksbank remains bullish on the krona), and markets probably aren't expecting it, so there is some additional surprise effect to be compounded.

While we definitely cannot exclude more Riksbank FX sales beyond February, that is not our base case. We expect the Riksbank to tolerate a short-term SEK correction amid less favourable risk sentiment conditions once FX sales end, but policymakers should then be reassured by a rather stable appreciation in SEK as global rate cycles starting in 2Q favour high-beta currencies like SEK. We currently forecast EUR/SEK at 10.70 in 4Q24.

A new FX hedging programme may be deployed by the Riksbank if our bullish view on SEK does not materialise: that would most likely be due to external factors (e.g. Federal Reserve cuts delayed) rather than domestic economic slack since markets are largely pricing in monetary tightening-driven economic underperformance in Sweden in 2024.

SEK/NOK may have further to drop

As mentioned above, we see the longer-term FX impact of the end of Riksbank’s hedging operations emerging through the krona’s relative performance to other high-beta currencies. SEK’s closest peer, Norway's krone, looks more attractive in 2024, in our view.

SEK’s strength over NOK should reverse over the course of the year

First of all, NOK is more sensitive to a decline in global rates, which we expect to materialise as the Fed eases policy by 150bp this year. Second, NOK will remain positively exposed to energy prices, which we expect to find some support this year. Third, the rate and economic growth differential favours NOK over SEK.

Read the original analysis: What the end of Riksbank’s FX sales means for the krona

Author

Francesco Pesole

ING Economic and Financial Analysis

Francesco is an FX Strategist and has been with the firm since May 2019. His main focus is on the G10 space and, in particular, commodity currencies. He began his career at Credit Agricole CIB and holds an MSc in Financial Markets and Investments