What is NFP and how does it affect the Forex market?

NFP is the acronym for the Nonfarm Payrolls report, a compilation of data reflecting the employment situation in the United States (US). It shows the total number of paid workers, excluding those employed by farms, the federal government, private households, and nonprofit organisations.

The headline figure, expressed in thousands, is an estimate of the number of new jobs added (or lost, if negative) in a given month.

But the report also includes the country’s Unemployment Rate, the Labor Force Participation Rate (or how many people are working or actively seeking a job compared to the total population) and Average Hourly Earnings, a measure of how wages increase or decrease month over month.

Why is NFP important for Forex markets?

The Forex (FX) market pays extra attention to the US macroeconomic figures, as they reflect the health of the world’s largest economy. Employment data is particularly relevant because of the Federal Reserve (Fed) mandate. “The Fed's modern statutory mandate, as described in the 1977 amendment to the Federal Reserve Act, is to promote maximum employment and stable prices. These goals are commonly referred to as the dual mandate,” according to the central bank itself.

Generally speaking, a solid increase in job creation coupled with a low Unemployment Rate is usually seen as positive for the US economy and, hence, the US Dollar (USD). On the contrary, fewer-than-expected new jobs tends to hurt the US Dollar.

However, nothing is written in stone in the FX market.

Ever since the Coronavirus pandemic, markets’ dynamics have changed. The overextended lockdowns and the subsequent reopenings had an unexpected effect: soaring global inflation.

As prices increased fast, central banks had no choice but to lift interest rates to tame inflation. This is because high rates make it more difficult to borrow money, reducing the demand for goods and services from households and companies and thus keeping prices at bay.

Interest rates reached multi-decade peaks in 2022-2023, and economies cooled. But inflation took long to recede. In fact, most major economies are still seeing how prices grow by more than what central bankers would like to.

In the case of the US, the Fed’s goal is for prices to grow at an annual pace of around 2%. Despite having retreated from the highs posted in mid-2022, price pressures remain above desired.

Ahead of the announcement, the US released a couple of relevant reports: On the one hand, the ADP report on private job creation showed the sector added 122,000 new positions in December, missing expectations of 140,000. Meanwhile, the number of job openings on the last business day of November stood at 8.09 million, according to the Job Openings and Labor Turnover Survey (JOLTS) report. This reading followed the 7.83 million reported in October and came in above the market expectation of 7.7 million.

The optimistic figures hint at another month of solid job creation in the US.

But what does employment have to do with the Fed?

Keeping unemployment subdued is also part of the Fed’s mandate, but a strong labor market usually translates into higher inflation. The Fed is in a tough balancing act: controlling inflation can mean more job losses, while a very strong economy can mean higher inflation.

The Chairman of the Fed, Jerome Powell, has long said the central bank needs a “weaker” labor market, meaning that the economy creates fewer jobs, to trim interest rates.

The US economy has consistently performed very well after the pandemic, creating plenty of jobs month after month. Even though this seems a desirable situation for the country, the Fed read it as a potential risk to inflation. To tame price pressures, US policymakers kept interest rates high for as long as possible.

Finally, the Fed decided to trim interest rates, delivering a 50 basis points (bps) rate cut in September, followed by a 25 bps cut in November and a similar move in December.

Yet, there is one more twist to the story. The US had a presidential election in 2024, which brought Republicans, led by former President Donald Trump, back to the government. Trump will take office on January 20, but his plans have already taken their toll on financial markets and the Fed.

President-elect Donald Trump has pledged to impose massive import tariffs on friends and enemies to “protect” the local economy. As a result, the Fed has shifted the focus back to prices, anticipating higher inflationary pressures amid increased import costs. Not only did the central bank change the North, but it also adopted a more hawkish monetary policy stance, anticipating just two potential rate cuts in 2025.

As a result, employment-related data is having a decreased impact on the US Dollar, as the Fed’s attention remains elsewhere.

What to expect from the December NFP report?

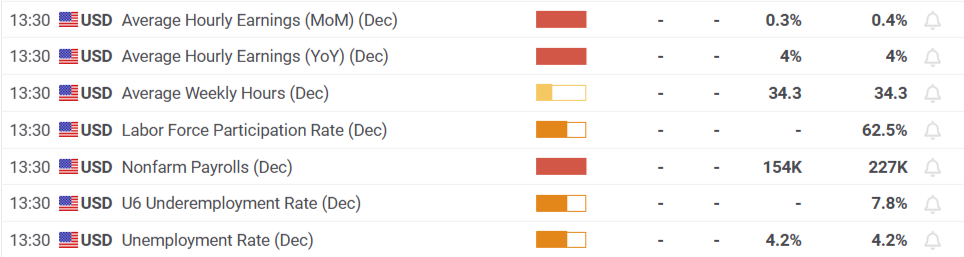

The November NFP report showed that the US economy created 227,000 new jobs in the month, while the Unemployment Rate was confirmed at 4.2%. The US Dollar strengthened with the news, finishing the day with substantial gains against most major rivals, as the upbeat figure fell short of affecting the Federal Reserve’s stance.

For December, economists expect the US economy to have created 160,000 new positions, another solid figure. At the same time, the Unemployment Rate is foreseen to remain steady at 4.2%.

If that’s the case, financial markets will likely welcome the continued job creation and steady unemployment rate, allowing the Fed to maintain its recently adopted path when they meet on January 28-29.

An NFP report showing fewer jobs created than what is expected could spur concerns about the labor market’s performance.

Hence, the USD will then fall.

Finally, a report indicating solid job creation should boost the market’s mood and, hence, the US Dollar, as it would indicate a resilient economy.

As always, regarding macroeconomic data, the divergence between expectations and the actual result will determine the strength of directional movements across the FX board.

The more significant the deviation, one way or the other, the wider the market reaction. Either extremely upbeat or shocking poor readings will exacerbate the directional movements.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.