What China’s ‘two sessions’ mean for the climate and commodities

China's biggest political event of the year, the 'Two Sessions', highlighted the need to enhance energy security - a new priority that will come at the expense of the energy transition in the short term. But the shift to renewables remains a key goal for the long term.

Energy security in the spotlight

Food and energy security featured prominently in China's 'Two Sessions' as the Russia-Ukraine war exacerbates concern over inflation and supply chain pressures.

On energy security, the government announced plans to accelerate the exploration and production of oil, gas, and minerals. In the near term, we will likely see China increasing purchases of crucial commodities from global markets in order to ensure adequate supply in the event of further disruptions. Therefore, the tighter global supply dynamics we are currently seeing, combined with potential Chinese stock building, suggest that commodity prices will remain well supported in the short term.

With energy security now a higher priority, the government has not set limits on energy consumption per GDP or coal production, signalling its intention to ensure flexibility in the event of a severe energy shortage.

Yet China is still doubling down on renewable energy. The Two Sessions highlighted the progress that was made in reducing pollution last year, with the average concentration of fine particulate matter in big cities dropping by 9.1% while the capacity of renewable energy power generation exceeded 1 billion kilowatts.

And clean energy continues to be a key element of China's energy policies. For example, it was confirmed that its wind and solar power programme will grow to at least 450 gigawatts in size, larger than most countries’ total power fleets. And the Ministry of Finance has said it will provide funding for new clean energy projects.

Clean energy continues to be a key element of China's energy policies.

Plans mentioned during the Two Sessions include the construction of large-scale wind and solar bases and improvements to the grid's ability to absorb renewable energy power generation. Green energy will be measured by total carbon emissions and intensity. The government work report also emphasised improving pollution control in important rivers, lakes and bays, and to continue to control and prevent soil pollution, as well as strengthening the treatment of solid waste and new pollutants in 2022. It also plans to replace clean coal with other clean power sources to save energy and reduce carbon emissions.

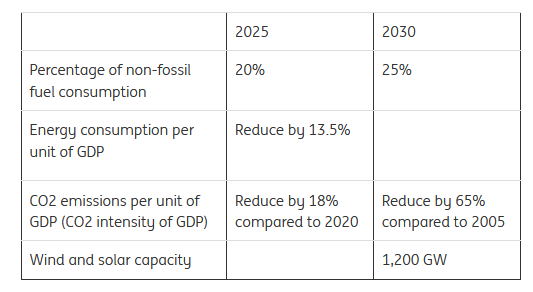

Still, China didn’t provide an update on its energy and climate-related targets during the Two Sessions. Premier Li Keqiang only mentioned that China would “take orderly steps” towards its goal of realising peak emissions by 2030 and carbon neutrality by 2060, while sticking to the Action Plan for Reaching Carbon Dioxide Peak Before 2030 released last year prior to COP26. The current targets are as follows.

Are the targets achievable?

According to estimates from the International Energy Agency (IEA) and Carbon Action Tracker, China is on track to meet its 2030 peak emissions target and could even achieve this goal in the mid-2020s with current policies. Carbon neutrality is also within reach. The analysis sends a positive signal but could also indicate that the country’s targets are not very aggressive and that the policy being set is actually only keeping China on track to achieve the minimum targets. This means that China will likely continue to face pressure from the international community to strengthen climate goals, especially after it joined a last-minute intervention at COP26 to change the wording of the conference's declaration from phasing out coal to phasing it down.

To attain the announced pledges, significantly higher spending will be required. The IEA forecasts that China's annual investment will need to climb to $640 billion in 2030 and $900 billion in 2060. These investments will add around two percentage points to GDP every year, and should also lead to higher quality growth in the long term.

The challenge is more on green financing. As many economies have set their own CO2 emission targets, the supply of green bonds and green loans is increasing. To keep up with the genuine definition of “green”, issuers and borrowers must show that they can achieve the green targets. This should crowd out the poor quality green finance but will take time.

Another challenge is that a shortage of semiconductors could delay the manufacturing of wind and solar energy infrastructure and a more energy-efficient grid. We expect that these shortage issues could be resolved in 2024 when big semiconductor producers have completed their new plants.

Good COP, Bad COP: Separating heat from light at the climate summit

Still, more coal than clean energy

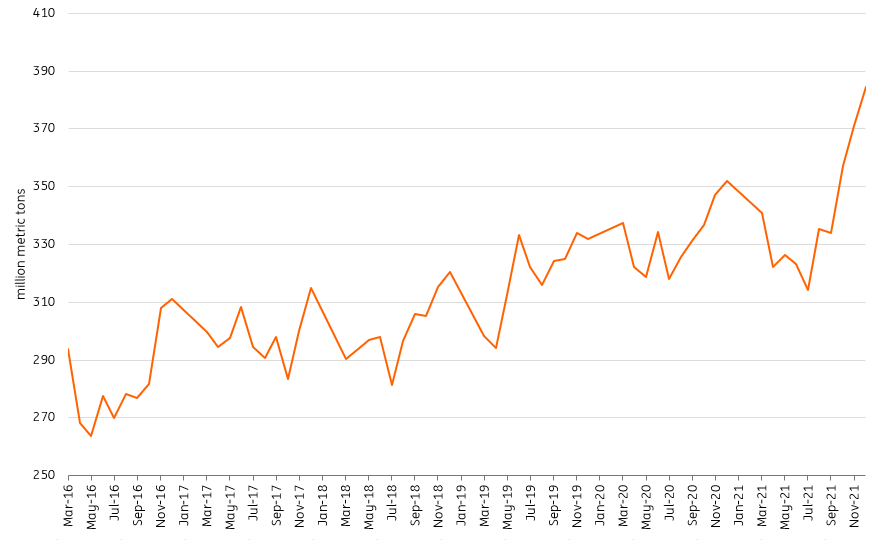

Last year highlighted the difficulties in managing the pace of the energy transition. This is evident with the ongoing energy crisis we are seeing in Europe, while China had its own issues with energy supply last year. The Chinese government had to take quick action to boost domestic coal output in order to end an energy crisis. In 2021, domestic coal output in China hit a record 4.07b tonnes, up almost 17% year-on-year.

China's coal production

Bloomberg New Energy Finance, China National Bureau of Statistics

Given the concerns over energy supply this year and the resulting strength in global energy prices, we are likely to continue to see coal output growing this year. China’s NDRC has already said that it will boost coal production in 2022 as well as increase coal reserve capacity. This approach appears to confirm that China will take a more orderly approach when it comes to finding a balance between ensuring energy security and limiting carbon emissions. This could potentially also mean that natural gas will play a more important role in the transition for the power sector. Up until now, natural gas has played a fairly limited role in the power mix.

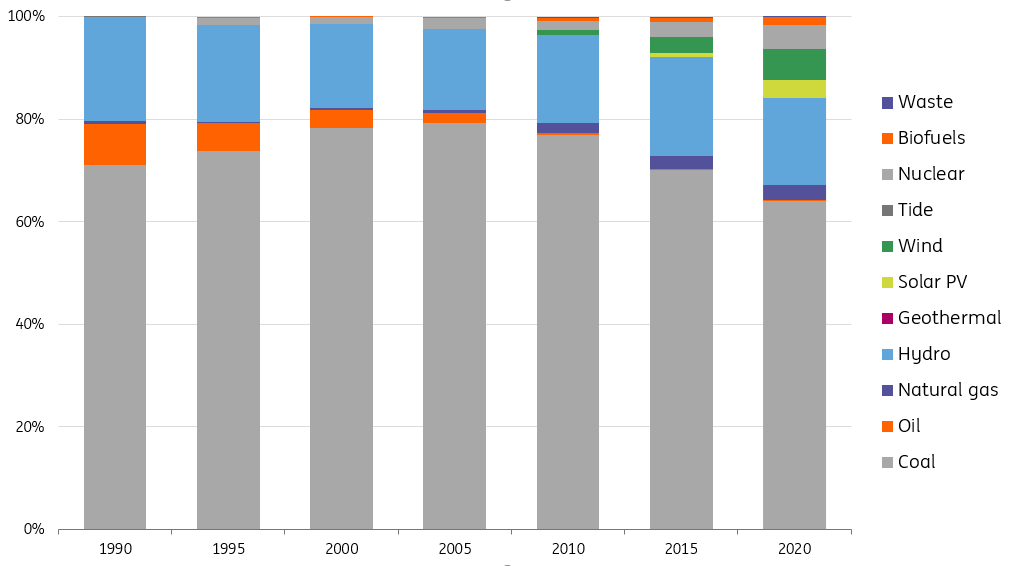

Coal looks set to remain dominant in China in the short to medium term.

With no hard targets and rising energy security concerns, coal looks set to remain dominant in the country in the short to medium term. Coal accounted for more than 60% of the country's electricity generation mix in 2020, and the IEA estimates a similar contribution in 2024. Nevertheless, annual coal capacity additions are projected to decrease in the next few years, resulting in a slow greening of the power mix.

China's electricity generation by source

International Energy Agency

Demand for metals from infrastructure

China is once again turning to infrastructure spending to stimulate the economy in 2022. However, the focus of investment will be narrower than in the past, with less rampant investment in speculative and unsustainable projects.

Officials have discussed plans for both old and new infrastructure projects, which should boost demand for metals to varying extents. Traditionally, zinc is largely exposed to old infrastructure though this has become less clear cut. Still, the metal's use in galvanised steel should continue to benefit from old infrastructure projects. Copper, on the other hand, is set to benefit from new infrastructure power projects such as Ultra High Voltage electric grids and the charging infrastructure for electric vehicles, with both areas continuing to see substantial growth. The UHV projects also mean more consumption of aluminium and steel. Other projects such as railway, gas and oil pipeline projects could see increasing demand for stainless steel or special alloys.

While the construction of infrastructure should boost demand for metals in China this year, overall demand growth could vary depending on the individual exposure of metals to different sectors.

Read the original analysis: What China’s ‘Two Sessions’ mean for the climate and commodities

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.