Week ahead: US Retail Sales and UK CPI data enter the spotlight

-

After US CPIs, US retail sales may also impact Fed hike expectations.

-

Will the UK inflation numbers increase the chances for another BoE hike?

-

Aussie and Kiwi traders await Australia jobs report and New Zealand’s CPI.

-

China’s GDP could also impact those commodity-linked currencies.

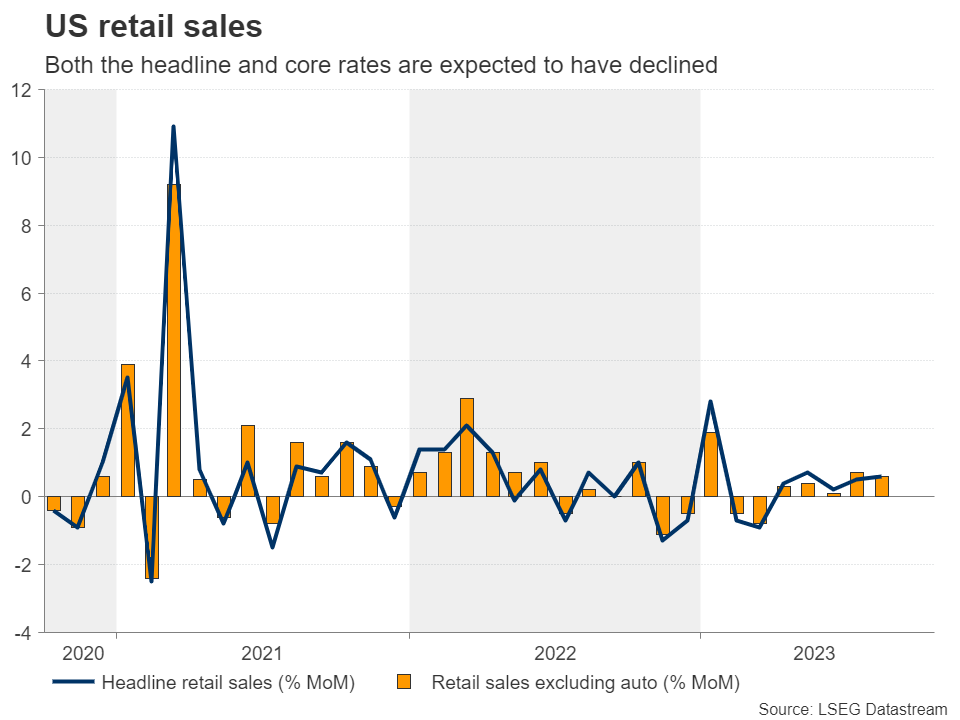

Will retail sales allow the dollar to extend its recovery?

The dollar traded on the back foot for the better half of this week due to dovish remarks by Fed officials who suggested that the surge in Treasury yields since they last met has done the work for them, implying that another hike before the end of the year may not be needed.

However, Thursday’s CPIs revealed that headline inflation held steady at 3.7% y/y, instead of slowing to 3.6% as expected, encouraging market participants to bring rate hike bets back to the table. From 28%, the probability for a final quarter-point rate increment increased to around 40%, while the rate reductions penciled in for next year have been reduced by around 10bps. This helped the dollar rebound.

As they try to further clear the fog, investors are likely to keep their gaze locked on more Fed speeches next week, with several officials scheduled to step onto the rostrum. It will be interesting to hear what they have to say in the aftermath of the inflation numbers.

That said, although their view on interest rates may be a priority for market participants, economic data may also be closely monitored for updated indications on how the world’s largest economic powerhouse has been faring.

On Tuesday, headline and core retail sales for September are forecast to have slowed to 0.2% m/m and 0.1% m/m respectively after both growing by 0.6% in August, while industrial production is also expected to have decelerated. On Thursday, although housing starts are seen increasing, the more forward-looking building permits are forecast to have slid, while on Friday, existing home sales are expected to have declined, suggesting that the housing market continues to cool down.

Nonetheless, with the Atlanta Fed GDPNow being upwardly revised to indicate that the US economy has expanded 5.1% in Q3, the dollar is unlikely to take another strong hit from slightly softer data, especially if Fed officials start talking about one more hike before the end credits of this tightening crusade roll. Even if the greenback pulls back again, such a retreat may be seen by the bulls as an opportunity to add to their positions at more attractive levels.

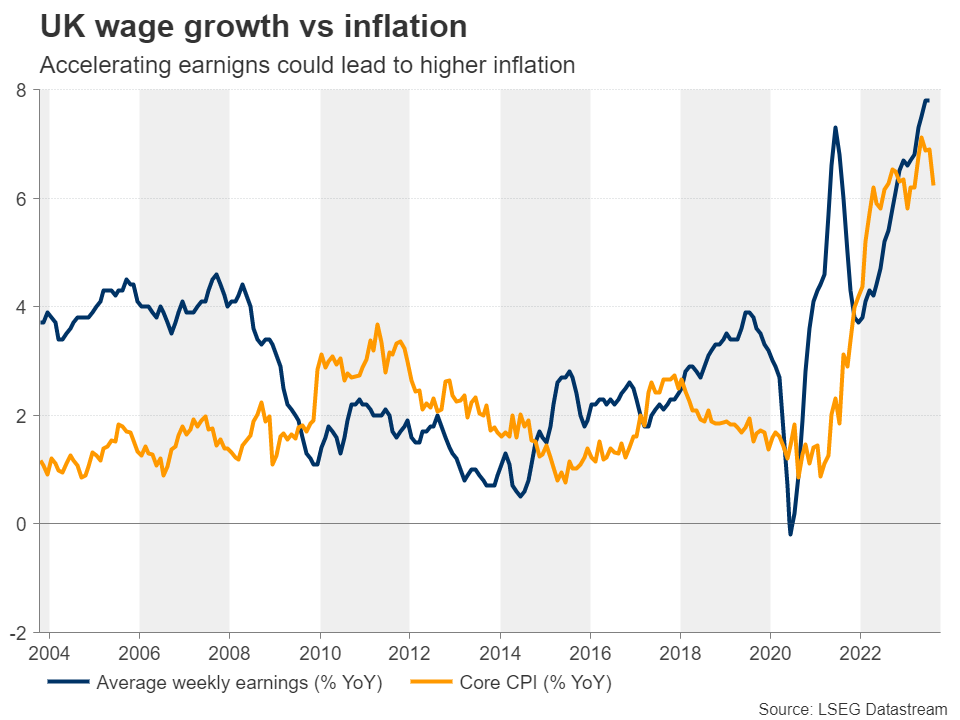

UK jobs, CPI, and retail sales data to shake the pound

The British pound will also enter the spotlight next week, with the agenda including the UK employment report for August on Tuesday, the CPI figures for September on Wednesday, and the retail sales for the same month on Friday.

At its latest gathering, the BoE kept rates steady citing slowing economic activity and a cooling labor market, and with the data since then keep painting a gloomy picture, investors are assigning a 78% probability for policymakers to remain sidelined at their next meeting in November, with the remaining 22% pointing to one last 25bps hike. They believe that a final hike is more likely to happen after the turn of the year, with a 55% probability assigned to the March 2024 decision.

The only data point corroborating more interest rate hikes by the BoE is wage growth, which remains elevated. Thus, for the hike probability to rise, just another print of strong weekly earnings may not be enough to change investors’ opinion. The CPI data may need to indicate that inflation is stickier than previously thought and retail sales may need to accelerate.

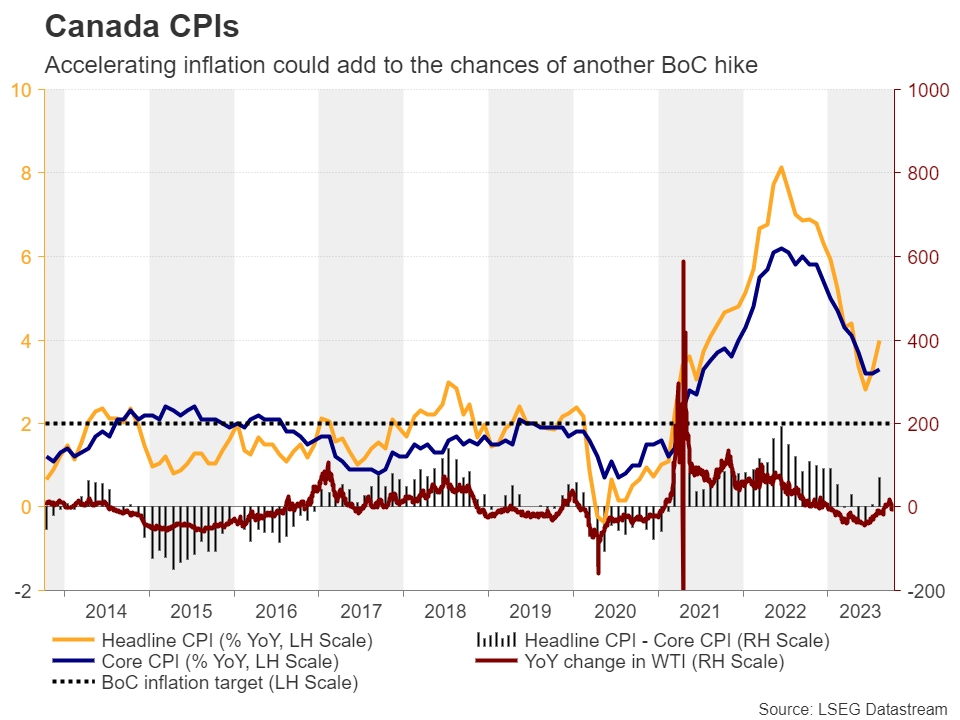

Loonie also awaits inflation numbers

Canada also releases its inflation numbers on Tuesday. In early September, the Bank of Canada kept interest rates untouched but noted that they remain concerned about the persistence of underlying inflationary pressures, and that’s why they remain prepared to raise rates further if needed.

Still, investors are not expecting any action at the upcoming meeting on October 25, assigning only a 23% probability for a 25bps increment, while the chances for hitting the hike button one last time by March 2024 are those of a coin toss. Even if participants are not convinced that another hike may be warranted this year, they could raise the probability for an increase being delivered at the turn of the year if the CPI numbers confirm the BoC’s concerns, something that may allow the loonie to recover some ground against its neighboring greenback.

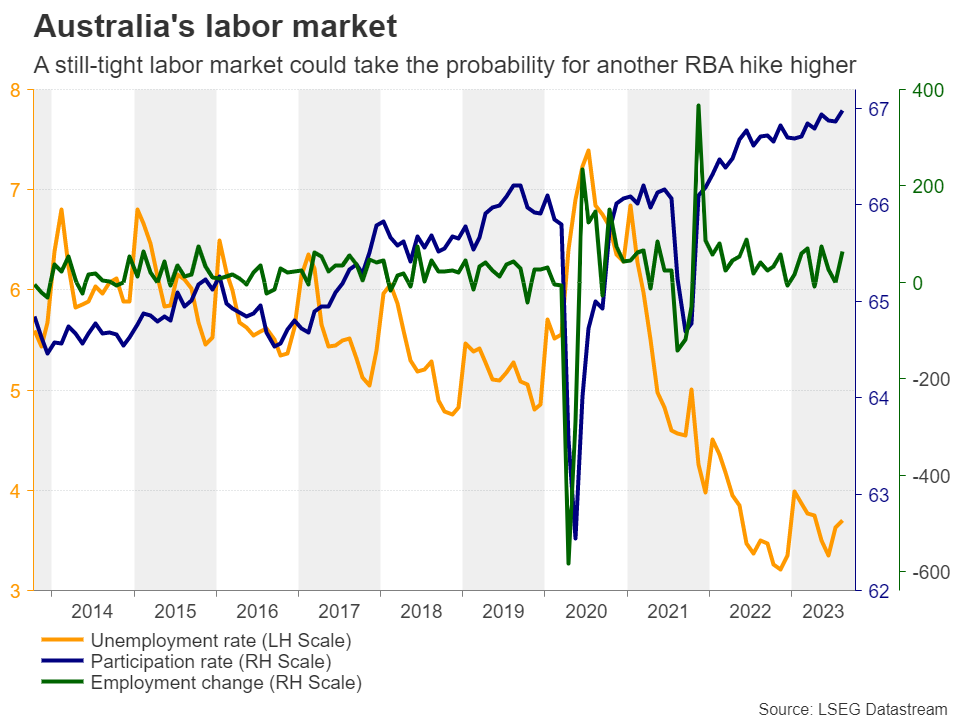

Aussie and kiwi traders may have a very busy schedule

Traders of the other risk-linked currencies, the aussie and the kiwi, may also stay busy next week.

On Tuesday, the RBA releases the minutes of its latest gathering, where officials kept interest rates untouched for the fifth consecutive month but added that some further tightening of policy may be required, while on Thursday, Australia’s jobs data will be released.

Although investors see an 83% probability for the Bank to remain sidelined in November as well, they are assigning a decent 60% chance for another 25bps hike to be delivered by May 2024. Thus, numbers pointing to a still-tight labor market may encourage aussie traders to add to their long positions.

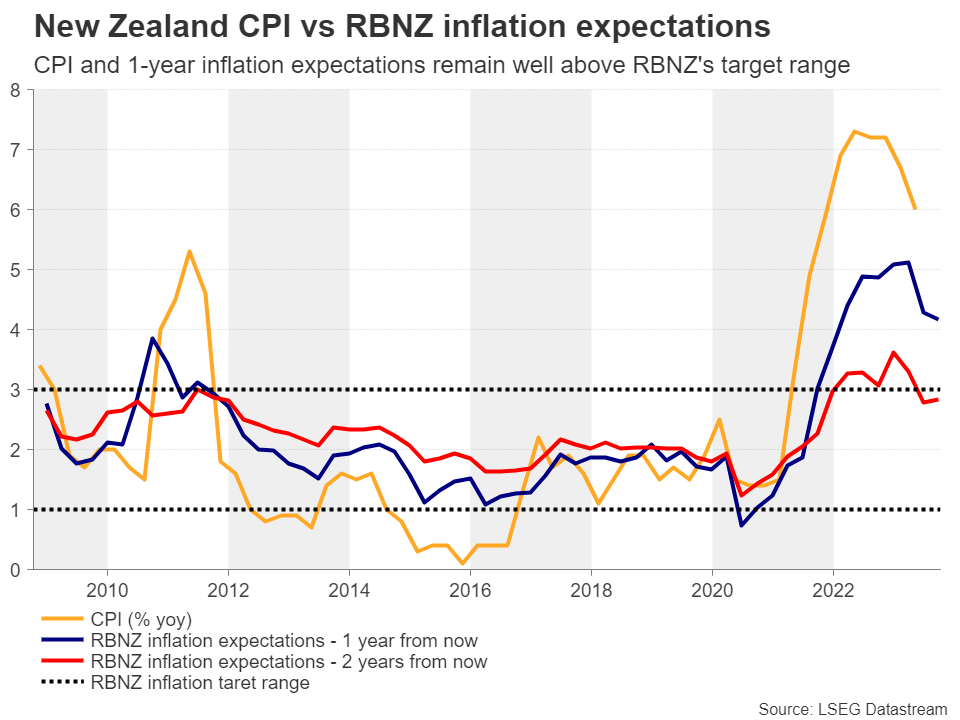

Kiwi traders may do the same if New Zealand’s CPI for Q3 comes in hotter than expected. The RBNZ stayed sidelined earlier this month and offered no hints on whether they are considering additional rate increases following the much-better-than-expected GDP data for Q2. However, similarly to the RBA, investors are assigning a more than 50% probability for one last 25bps hike by May.

Having said all that, due to the close trade ties Australia and New Zealand have with China, both currencies could also stay sensitive to developments and data concerning the world’s second largest economy. On Wednesday, China’s GDP for Q3 is on the agenda, accompanied by the industrial production, retail sales and fixed asset investment figures for September. Should these releases corroborate the view that the Chinese economy is stabilizing, the aussie and the kiwi could benefit.

Earnings season kicks off

In the equity arena, the earnings season is kicking off today with results from major US banks, while on Wednesday, Tesla and Netflix will make their numbers public after the closing bell.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.