Week ahead: US CPI inflation takes centre stage

The December 2024 US employment situation report crowned last week’s busy economic data slate. Non-farm payrolls surprised to the upside, with the economy adding 256,000 new jobs from November’s downwardly revised reading of 212,000. December’s print comfortably surpassed the market’s median expectation of 160,000 and the maximum estimate of 200,000 and helped dash hopes of further policy easing from the US Federal Reserve (Fed) this year.

As you would expect, the US dollar (USD) immediately rallied higher following the jobs report but failed to gain much follow-through, which may have been due to softer earnings growth. In a mailer sent to Traders ahead of the event, I noted that given the possible inflationary implications of Trump’s anticipated plans, Friday’s jobs report would place greater emphasis on earnings growth. The softer earnings data could be why the USD failed to find acceptance at higher levels. Granted, 256,000 is a meaningful payroll jump, and the unemployment rate unexpectedly ticked lower to 4.1% from 4.2% in November. but earnings decelerated on a month-on-month (MM) and year-on-year (YY) basis to 0.3% and 3.9%, respectively.

Jobs growth, coupled with inflation expected to remain sticky and Wednesday’s FOMC meeting minutes (Federal Open Market Committee) highlighting concern regarding the impact on inflation that US President-elect Donald Trump’s proposed policies may bring, I feel there is little reason for the Fed to cut rates anytime soon. Markets are now pricing in 28 basis points (bps) of easing this year – one rate cut – compared to 40 bps before the data release, with a 25 bp cut now pushed out until September’s meeting (24 bps). Several desks have already trimmed rate cut forecasts, with Bank of America (BofA) now expecting the Fed to stay on hold for 2025. You will recall that the latest projections from the Fed (derived from the Summary of Economic Projections) were hawkish, suggesting a slower pace of cuts for 2025 and 2026. FOMC participants revised the funds target rate lower to 50 bps in 2025 from 100 bps.

US CPI inflation eyed

Top of the agenda for the US this week will be US CPI inflation data for December 2024, released on Wednesday at 1:30 pm GMT. Economists polled by Reuters forecast YY headline CPI inflation to tick higher to 2.8%, up from 2.7% in November (this was the second consecutive month price pressures accelerated). The estimate range is currently between 2.9% and 2.6%. Excluding food and energy, core inflation is anticipated to rise 3.3%, matching November; estimates range between 3.3% and 3.1%.

If inflation proves more persistent than expected, it may further raise doubts about the Fed’s plans to lower interest rates, especially in light of the inflationary effects of Trump and his proposed policies. Such developments could negatively impact the bond market (send US Treasury yields higher) and contribute to a stronger USD.

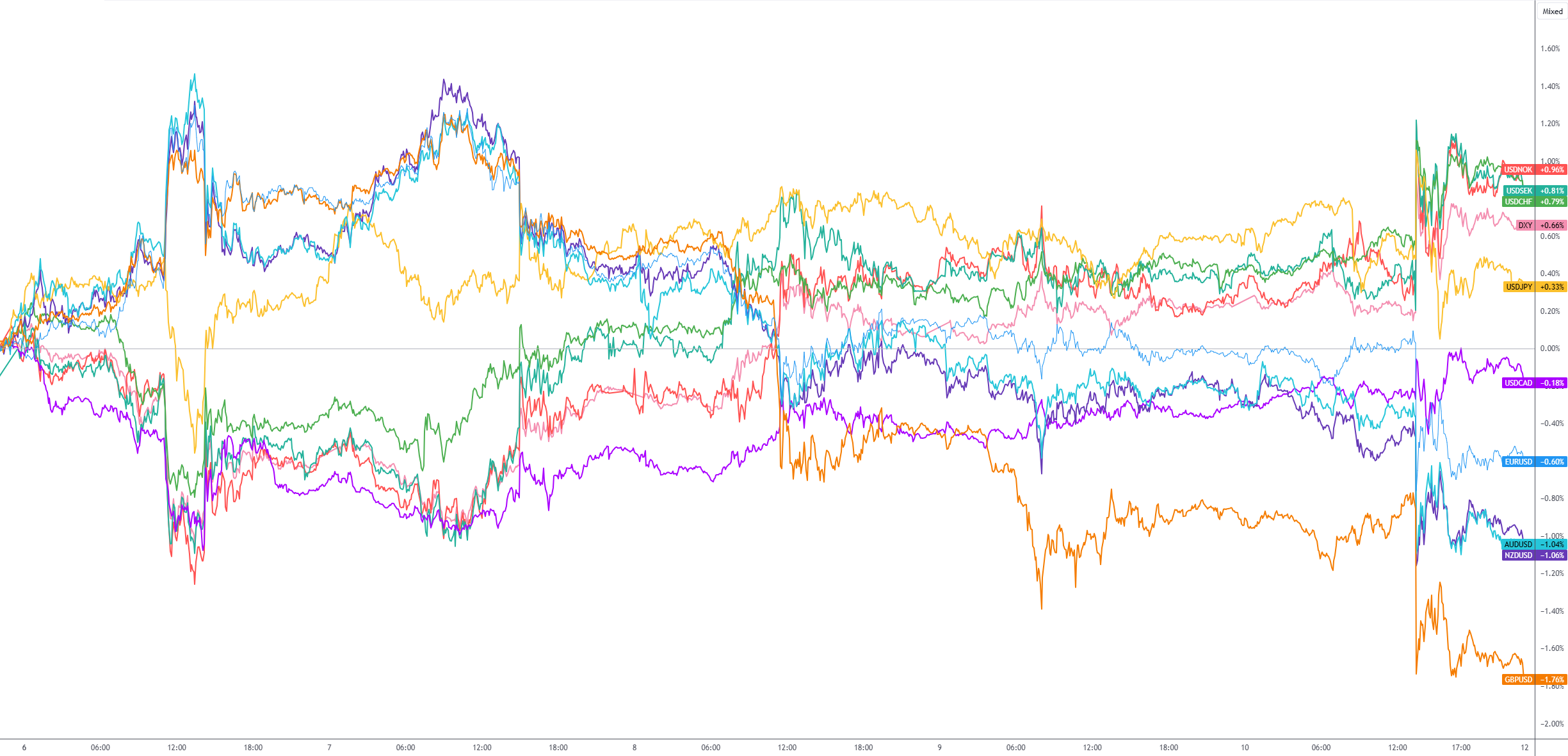

Weekly G10 FX performance

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,