Week ahead – Flurry of key data eyed as markets digest Powell’s cautiousness

After Fed chief Powell all but guaranteed a July cut, things could quiet down a little next week, as the agenda is dominated by economic data. Growth figures from China may shed light on how much damage the trade war has inflicted, while in the US, retail sales numbers will be among the final pieces of the puzzle before the next Fed meeting. Inflation stats from New Zealand and Canada are also on tap, with some UK data perhaps attracting attention as well given a scarcity of Brexit news.

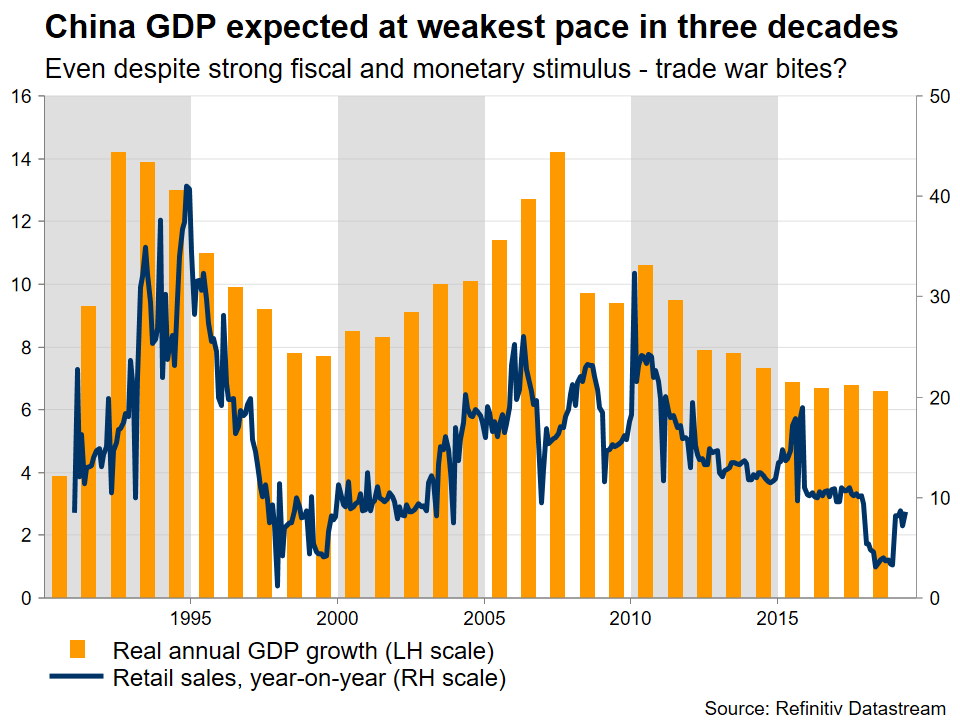

China’s growth to touch three-decade low, despite the stimulus

The world’s second-largest economy will release a raft of data on Monday, with the highlight being the GDP print for Q2. Economic growth is forecast to have slowed to 6.2% in yearly terms, from 6.4% earlier, which if confirmed would be the clearest sign yet that the trade war has really started to bite. The nation’s retail sales, fixed asset investment, and industrial production for June are all coming out as well.

While such a growth slowdown doesn’t seem extreme at first glance, one must consider that economic momentum is losing steam even despite strong stimulus – both fiscal and monetary – from the Chinese authorities. In fact, a 6.2% GDP reading would constitute the weakest print in three decades, implying that it could increase the pressure on policymakers to open the ‘stimulus floodgates’ even wider.

Besides the yuan, these figures could also impact the Australian dollar, as well as risky assets like stocks.

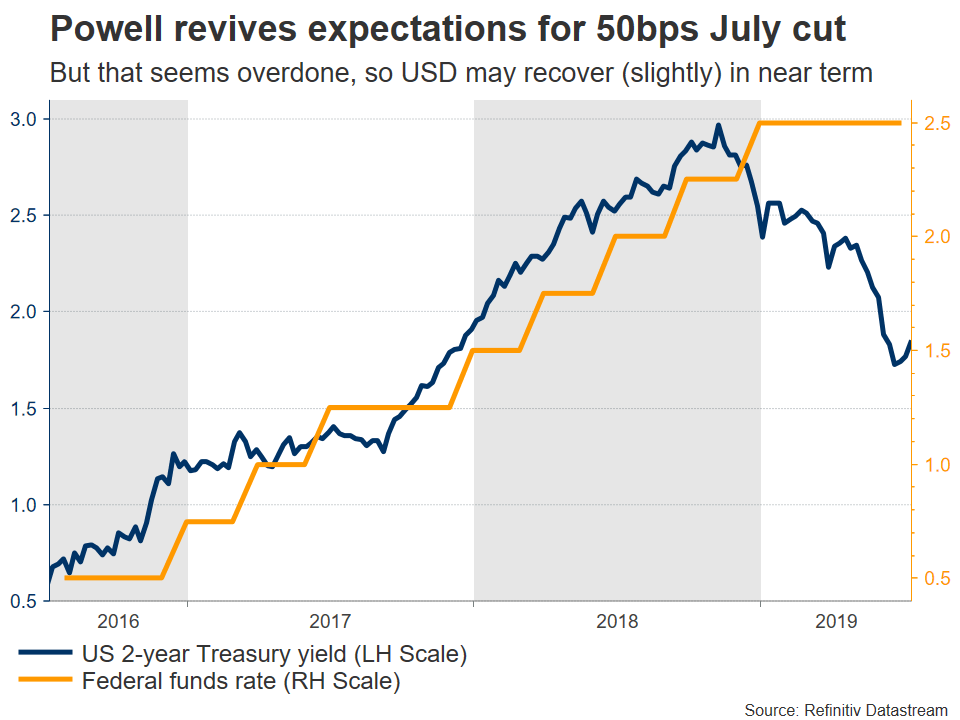

US retail sales among the final pieces of the Fed’s easing puzzle

In America, retail sales on Tuesday will provide the last piece of evidence on the consumer, before the Fed’s two-week ‘quiet period’ begins ahead of the July 31 rate decision. Forecasts suggest that retail sales slowed on a monthly basis in June, but remained in positive territory for a fourth straight month, which would be encouraging in itself.

Admittedly though, there’s not much that can stop the Fed from cutting rates in July, even if these numbers are stronger than expected. Chairman Powell made it painfully clear that the Fed will deliver an ‘insurance cut’, even though the domestic economy doesn’t seem to be in dire need of monetary stimulus yet. His proactive stance is likely a signal of how aggressively the Fed will react moving forward – policymakers don’t want to be caught ‘behind the curve’ in a recession.

As for the dollar, while it may rebound slightly ahead of July 31 as expectations for a ‘double’ rate cut are priced out again, the big picture remains grim. Global central banks are entering an easing cycle, and the Fed has the most firepower with which to ease. That means the potential downside in the dollar is likely much greater than the euro’s or the yen’s, as both the ECB and BoJ have much less scope to cut, given their already-negative rates.

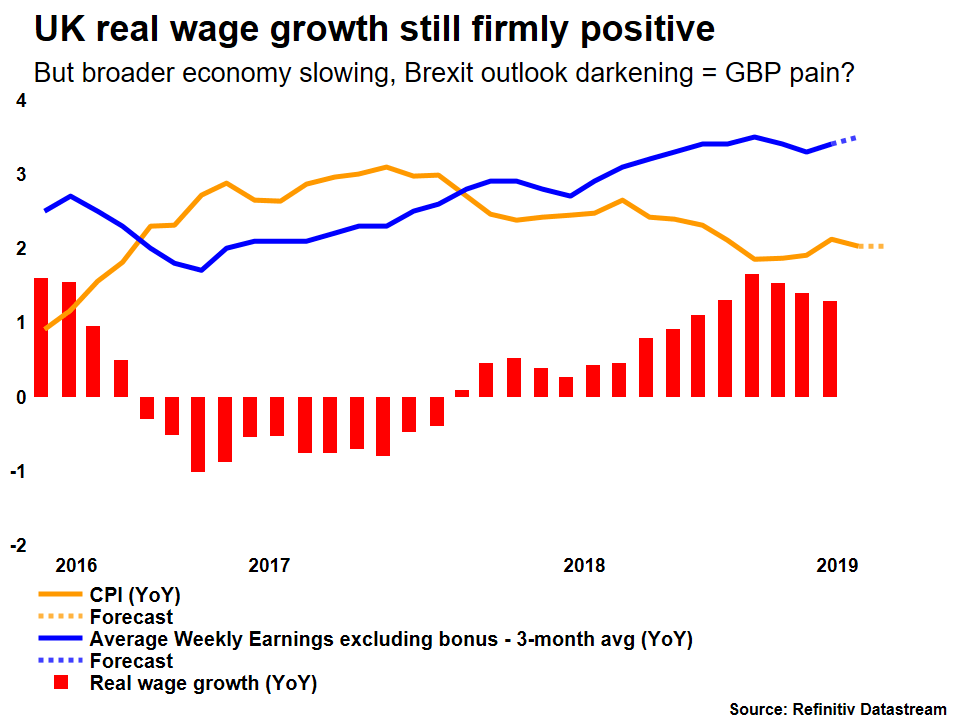

British data back in the spotlight amid Brexit hiatus

With the Conservative leadership contest not expected to conclude until July 22, Brexit news are likely to remain scarce for now, so UK data may come back in the limelight. Employment figures for May will hit the markets on Tuesday, before the inflation prints for June on Wednesday, culminating with retail sales stats on Thursday.

Mark Carney, the Bank of England Governor, changed his tune lately by highlighting that trade tensions have amplified downside risks for Britain. His comments imply the Bank may officially abandon its rate-hike plans soon, though that would hardly be surprising for markets, which currently price in a ~40% probability for a rate cut by December.

The pound, meanwhile, resumed its downtrend as both candidates hoping to become Prime Minister indicated they’d be willing to leave the EU in October without a deal. Granted, part of that may be ‘political theatre’, echoing Theresa May’s famous line: “no-deal is better than a bad deal”. What makes this threat more credible though, and hence scary for sterling, is that the Tories are sinking so severely in opinion polls that their next leader may truly consider a no-deal, for fear of losing more support as a party if Brexit is delayed again.

In this sense, the worst may not be over for the pound. Perhaps the only ‘saving grace’ for the currency may be further weakness in the US dollar, that offsets losses in sterling.

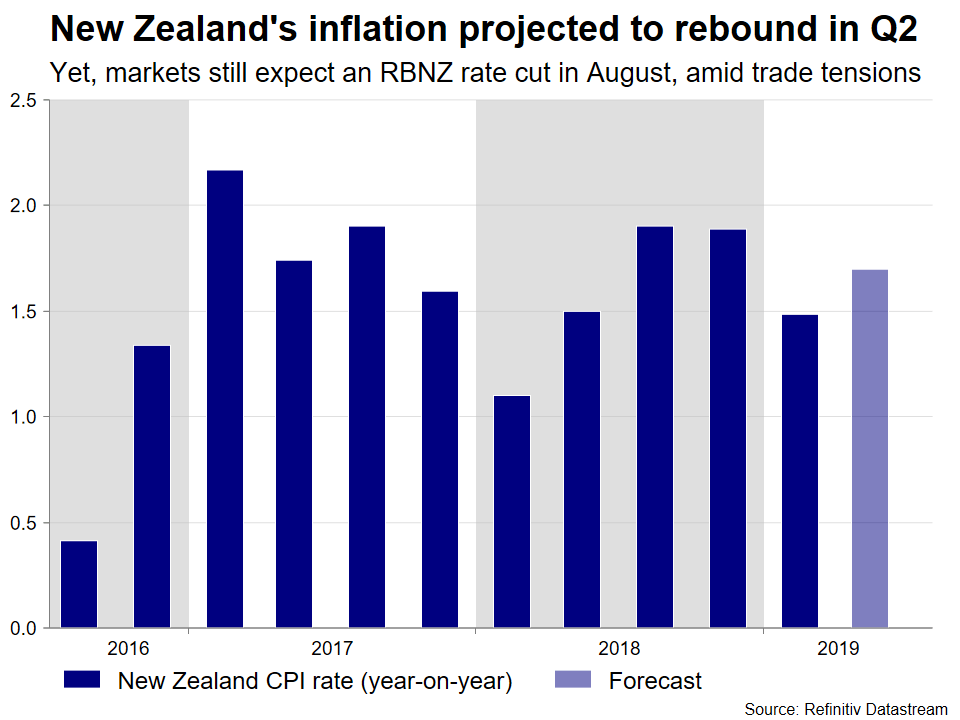

New Zealand inflation and Australian jobs data to guide antipodeans

The main event in New Zealand will be the release of inflation data for Q2 on Tuesday. The RBNZ already cut rates back at its May meeting and markets are pricing in a ~73% chance for another move at the August gathering, so these figures will be crucial in shaping expectations.

In Australia, jobs numbers for June are due on Thursday. The RBA also reduced rates, at both of its last two meetings, but appeared reluctant to signal more cuts. Instead, officials noted that labor market developments will guide their next move, which elevates the importance of the upcoming data.

The minutes from the latest RBA meeting are also due on Tuesday.

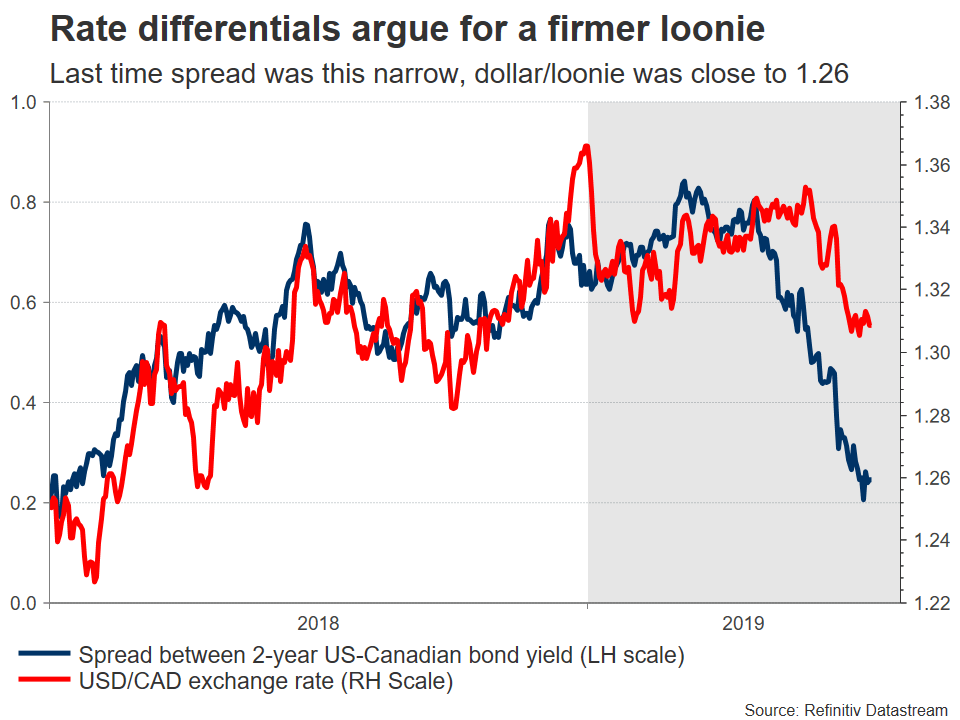

Canadian CPIs and retail sales coming up for loonie

The Bank of Canada (BoC) adopted a slightly more cautious tone this week, noting that trade tensions are becoming a bigger threat. Although policymakers still maintained a neutral stance overall, that could change quickly if the US-China negotiations turn sour. The loonie dropped but recovered quickly to touch a fresh high for 2019.

The next highlight for the currency will be the inflation data for June, due on Wednesday. Retail sales for May will follow on Friday.

While a lot will depend on trade, as long as the BoC-Fed policy divergence narrative holds, the outlook for the loonie remains positive overall.

Japanese inflation prints unlikely a game-changer for yen

In Japan, inflation numbers for June will hit the wires on Friday, but as usual the yen is unlikely to react much to economic data. Rather, the haven currency may take its cue mainly from any signals in the trade talks.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service