Week ahead – Fed’s hawkish tilt and Iran deal turn focus to PCE inflation and PMIs

- US PCE inflation data eyed after Warsh’s surprise hawkish debut.

- June PMIs in the spotlight too as US-Iran deal eases energy crunch.

- CPI data for Australia, Canada and Tokyo also on tap.

Warsh signals change and higher rates

New Fed Chair Kevin Warsh didn’t waste any time in his first FOMC meeting in prioritizing the need for the central bank to bring inflation back within the Fed’s 2% objective, unsettling markets just as subsiding geopolitical risks had lifted the mood in the past week.

Far from living up to the belief that Trump’s appointee would have made the case for looser monetary policy, Warsh doubled down on the Fed’s price stability mandate. Moreover, the updated dot plot indicated a significant hawkish tilt compared to the March projections, with the board split on whether to keep rates on hold or to raise them by year-end.

Investors quickly responded by bringing forward their rate hike bets to October and pricing in a substantial probability for a second 25-bps increase in March 2027. The US yield curve flattened, with short-term yields jumping higher. But the 30-year yield plunged on expectations that tighter policy now will bring down inflation in the long run.

However, Wall Street didn’t appreciate Warsh’s unwavering commitment to the 2% target, although uncertainty about his reform agenda also weighed on stocks. Warsh has set up task forces to review the Fed’s communication, the size of the balance sheet, the methodologies for collecting data, and the inflation framework.

These changes are unlikely to take place before the end of the year, but markets are mostly upset about Warsh’s decision to ditch forward guidance, which had become a key policy tool in the post-financial crisis era.

Renewed focus on inflation

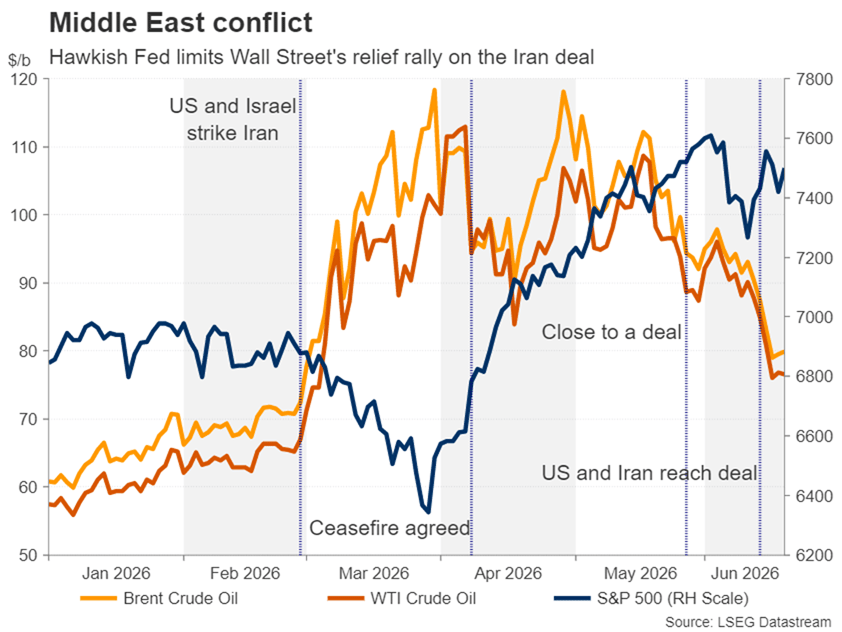

Investors have also been taken aback by the fact that this hawkish pivot has come even as the Middle East conflict appears to be nearing the end. With the US and Iran putting pen to paper to their framework deal that potentially paves the way for lasting peace if there is agreement on reigning in Tehran’s nuclear ambitions, traffic along the Strait of Hormuz is slowly returning to pre-war levels.

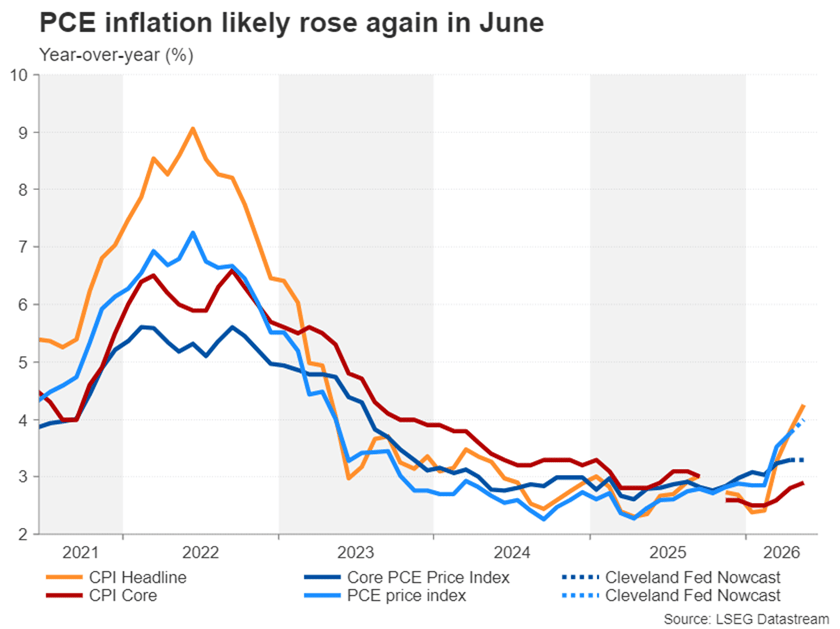

Subsequently, oil prices have crashed almost 11% in June, adding to May’s 17% slump. Central bank hawks would argue that the damage has already been done and it’s too early to dismiss the threat of second-round inflation effects. This is even more true for the Fed given that inflation in the US has been running above its 2% target for the past five years.

Markets were under the assumption that the Fed would be comfortable looking through the latest uptick in both CPI and PCE measures, but Warsh’s surprise determination to return inflation to 2% has shifted attention firmly back on the data.

The core PCE price index, which the Fed currently attaches the most weight to, is out on Thursday, along with the personal income and spending numbers for May. Core PCE is forecast to have stayed unchanged at 3.3% in May according to the Cleveland Fed’s inflation Nowcasting model, while headline PCE is projected to have edged up to 4.0% from 3.8%.

The final GDP readings for Q1 and durable goods orders for May are also due the same day, while ahead of Thursday’s data barrage, the S&P Global PMIs for June will be watched on Tuesday.

Aussie and Loonie eye May CPI as rate hike bets fade

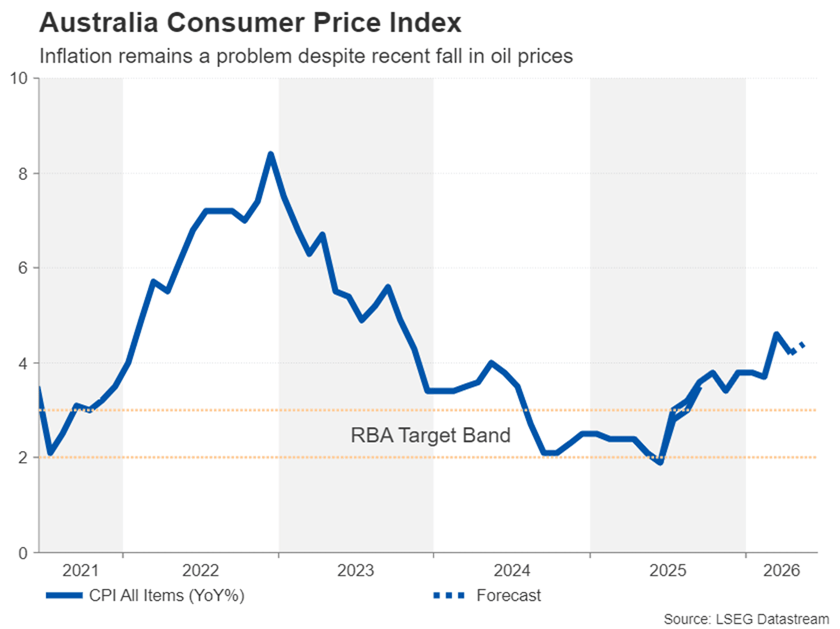

Inflation will also be on the agenda in Canada and Australia where the two countries are experiencing varying degrees of impact from the war in the Middle East. In Australia, there are some signs that the pickup in inflation is peaking, but the economy remains broadly solid. The RBA didn’t sound too concerned about the recent rise in the unemployment rate when it kept rates on hold last week and was more worried about inflation being so high, at 4.2% in April.

The May numbers are out on Wednesday, and the employment report will follow on Thursday. The risk is that inflation could head back up again after May’s encouraging decline, while the unemployment rate continues to climb. This would put the RBA in a real bind.

However, if oil supplies begin to flow again through the Strait of Hormuz and energy prices extend their drop, the RBA would probably ease up on inflation and prioritize its employment mandate. Investors have already scaled back their expectations of additional rate hikes by the RBA and are no longer fully pricing in a 25-bps increase.

Any further paring back of tightening bets next week could make it difficult for the Australian dollar to hold above $0.70.

In Canada, the US-Iran deal probably means that the Bank of Canada can avoid a rate hike altogether. A weak economy, sluggish jobs market and muted underlying inflation look set to keep the BoC on the sidelines during the energy price shock. Monday’s CPI numbers for May are unlikely to change the price outlook much, unless there’s a big overshoot from the forecasts. Hence, the Canadian dollar will continue to face pressure from a resurgent US dollar, which this week shot past C$1.41.

Euro and Pound on backfoot ahead of flash PMIs

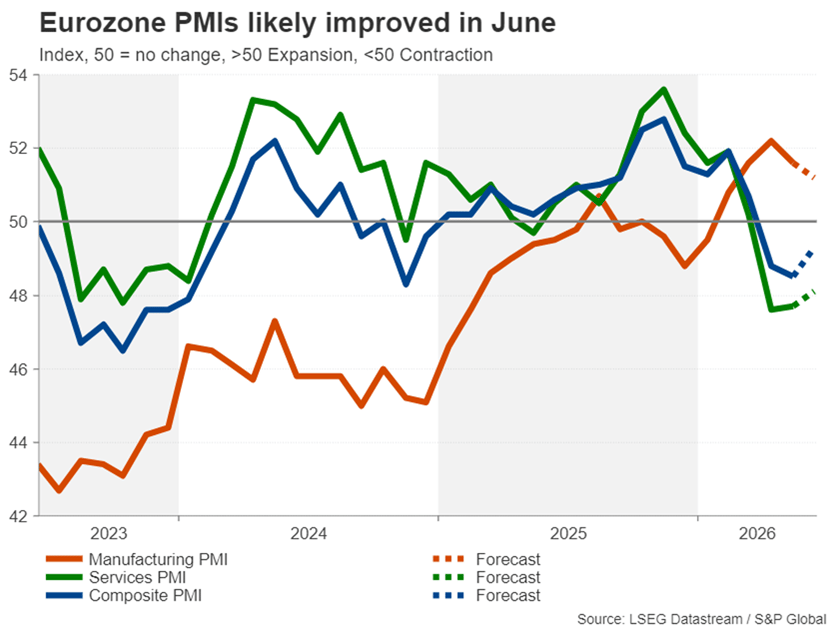

Eurozone manufacturing activity has maintained a steady recovery during the Iran conflict, but the services sector has been hit hard by the surge in energy prices. However, the services PMI likely recovered slightly in June when hopes of a deal began to rise and oil prices retreated further. If there’s no marked improvement in June, this would likely add pressure on the European Central Bank not to rush into hiking rates for a second time.

ECB policymakers have not shut the door to further hikes as there is still a huge degree of doubt about the full normalization of energy flows from the Gulf. Nevertheless, stronger-than-expected PMI readings could offer the euro some respite from the selling pressure as the dollar rallies on the back of the Fed’s hawkish shift.

The UK’s services PMI has also taken a dive from the Mideast turmoil, while manufacturing has grown. Similarly, any rebound in June would signal that the worst of the economic impact of the war is over, potentially bolstering the pound. Though, with the Bank of England evidently reluctant to hike interest rates, any boost is likely to be limited.

Yen flirts with danger again

The Bank of Japan lifted interest rates to a 31-year high this week, as the combination of the weak yen and higher fuel prices have raised the risk of second-round effects on inflation, while real wage growth has also accelerated.

Yet, despite policymakers’ increasing concerns about an inflationary buildup, the yen stabilized at best rather than attract any bullish traction. More to the point, the Fed’s unexpectedly hawkish hold on Wednesday has more than offset any temporary relief for the yen from Tuesday’s hike.

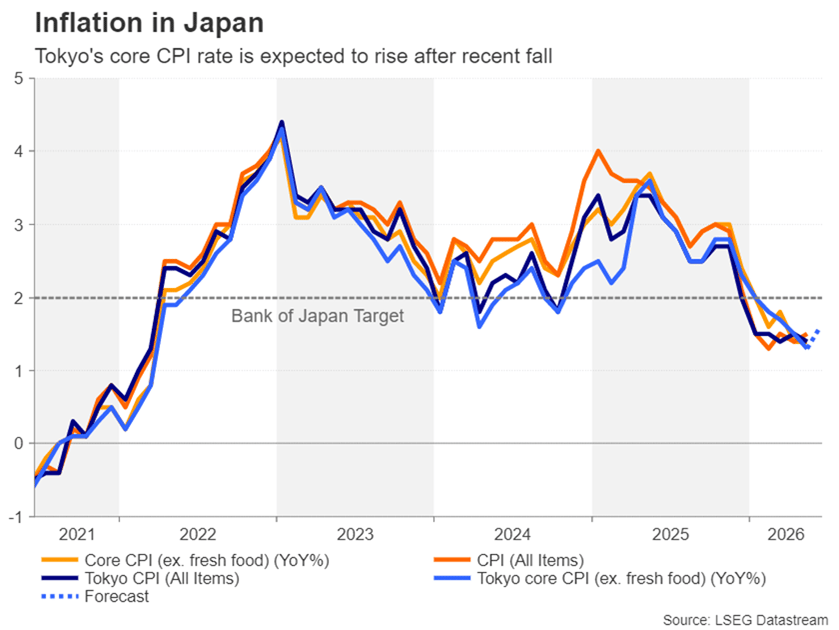

With the dollar once again flirting with the 161.00-yen level, the odds of intervention by Japanese authorities are very elevated. Friday’s preliminary CPI figures for the Tokyo region are unlikely to provide much of a boost to the yen, even if they show core CPI heading higher following six months of decline.

A better chance for the yen to halt its slide is if Wednesday’s Summary of Opinions of the BoJ’s June meeting reveals some previously undisclosed hawkish views, fuelling rate-hike expectations.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.