Week Ahead – Fed to stand pat but BoE could cut; US and Eurozone Q4 GDP eyed

There will be no shortfall of market-moving events in the coming week, with plenty of top-tier data and crucial central bank meetings shaping the agenda. The Federal Reserve will hold its first policy meeting of 2020 but Q4 GDP and PCE inflation numbers out of the United States are likely to be more helpful for investors in gauging the next move in interest rates. In comparison, the Bank of England’s meeting is expected to be the most exciting in quite some time. Elsewhere, inflation figures from Australia and flash GDP estimates from the Eurozone will set the tone for the aussie and the euro, respectively. Meanwhile, the world will be keeping an eye on the deadly coronavirus as any signs that the outbreak is worsening could further dampen risk sentiment.

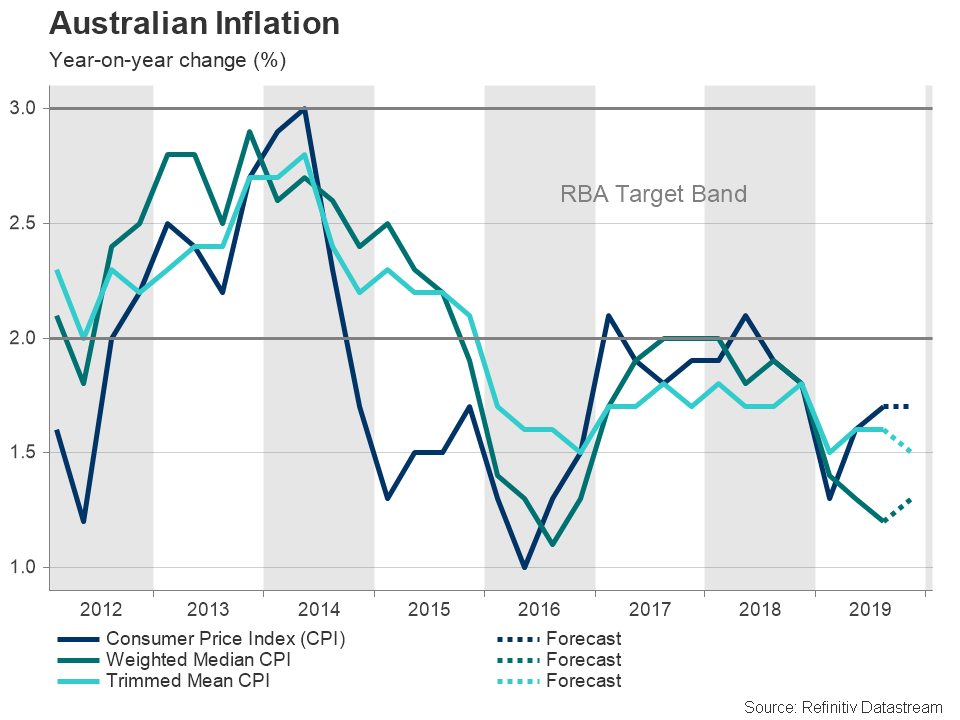

Australian CPI data could ease rate cut dilemma for RBA

Expectations of a February rate cut in Australia continue to see-saw as de-escalating trade frictions, devastating bushfires and better-than-forecast data have seen investors flip flopping between a reduction and no change. The latest consensus is that the Reserve Bank of Australia will hold off from cutting rates at its February 4 meeting after December employment numbers pointed to limited impact so far to the economy from the bushfires that have been ravaging the country since October.

If next week’s report on the consumer price index (CPI) for the fourth quarter is equally impressive, the odds for policy easing in February are likely to diminish further.

The CPI figures are due on Wednesday and will be followed by the producer price index (PPI) for the same period as well as private sector credit numbers for December on Friday. Ahead of those, the NAB business conditions survey for December might attract some attention on Tuesday, which may do a better job of revealing the scale of the damage from the bushfires on businesses.

The Australian dollar is in danger of being pulled lower again if the price indicators disappoint. The aussie will also be swayed by China’s official manufacturing PMI due on Friday, which will provide investors with the first glimpse on how the Chinese economy performed in the first month of the year. The Chinese market will be closed for the rest of the week as the country celebrates the Lunar New Year. But the nation will not be able to escape the headlines as authorities battle to contain the spread of the new virus.

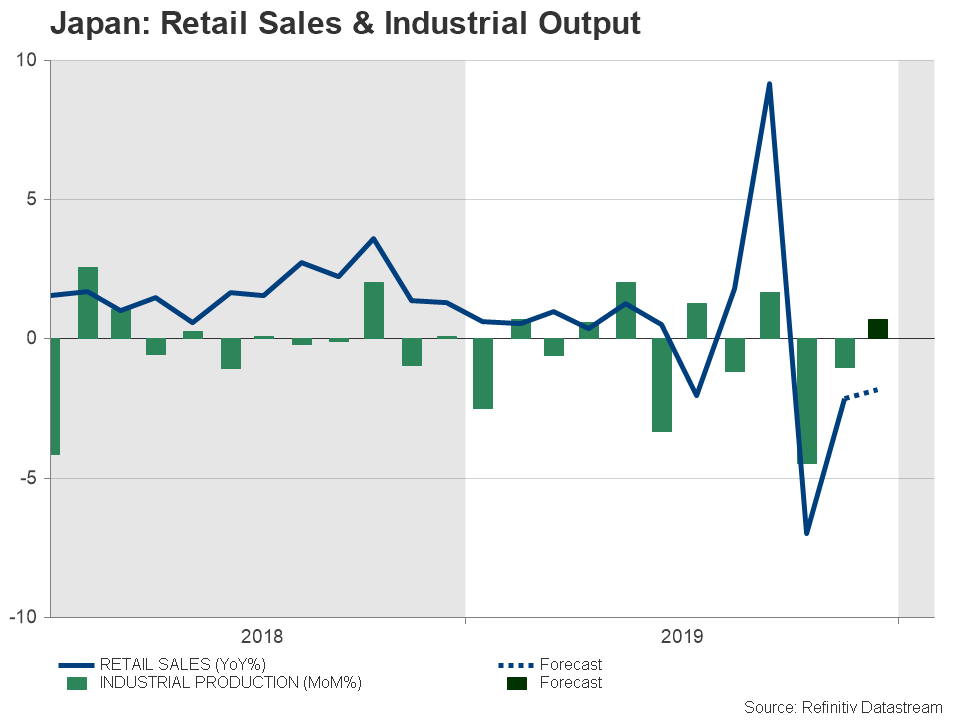

Japanese data to be watched for signs of rebound

Industrial output, retail sales and unemployment figures due in Japan on Friday will be important amid fears the economy is struggling to find its footing following the October sales tax hike and the endless slump in exports. If the preliminary industrial output and retail sales readings for December fail to turn positive after the previous month’s negative prints, it would cast doubt on the Bank of Japan’s recent upward revisions to its growth forecasts. The BoJ, meanwhile, will shed more light on its last policy decision when it publishes a summary of the January meeting on Wednesday.

However, as far as the yen is concerned, the main driver for the safe-haven currency will be how well risk appetite holds amid a possible pandemic from the coronavirus.

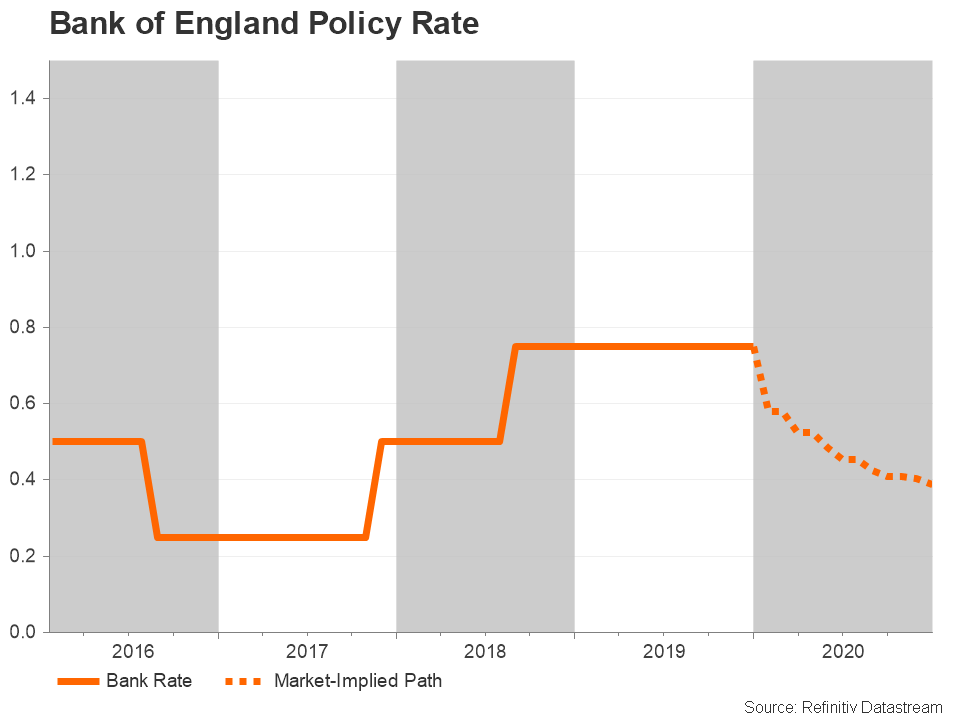

Bank of England ponders rate cut

The Bank of England will announce its latest policy decision on Thursday, now commonly dubbed as ‘Super Thursday’ as it is the meeting where the Bank will also publish its quarterly Monetary Policy Report and hold a press conference. While politicians at Westminster finally enjoy some calm as Boris Johnson’s Withdrawal Agreement completes its passage through Parliament and becomes law, the economy is stagnating as it reels from the Brexit turmoil that gripped the country in 2019.

The UK is now on course to formally leave the European Union on January 31, though in practice, aside from no longer holding a seat at the EU’s decision-making table, nothing will change until the end of the year when the transition period ends. The transition period will kick in at 23:00 GMT on January 31 and the streets are sure to be filled by passionate Leavers celebrating Britain’s historic exit from the world’s largest trading bloc.

However, it will be a much more sombre mood at the BoE where policymakers will be debating whether to cut interest rates or not. Expectations of an interest rate cut shot up earlier this month when Governor Mark Carney and two other monetary policy committee (MPC) members flagged lower rates. Their dovish views were reinforced by weak economic indicators for November/December. But more recent data has been somewhat more encouraging, and markets are now split about 50-50 as to whether the BoE will ease next week.

The pound is vulnerable to a big tumble in its initial reaction if there is a cut given that it hasn’t been fully priced in. But investors will also be looking at the Bank’s predicted rate path for the coming period for the prospect of future easing and any sell-off could be short-lived if policymakers are not overly gloomy about the outlook.

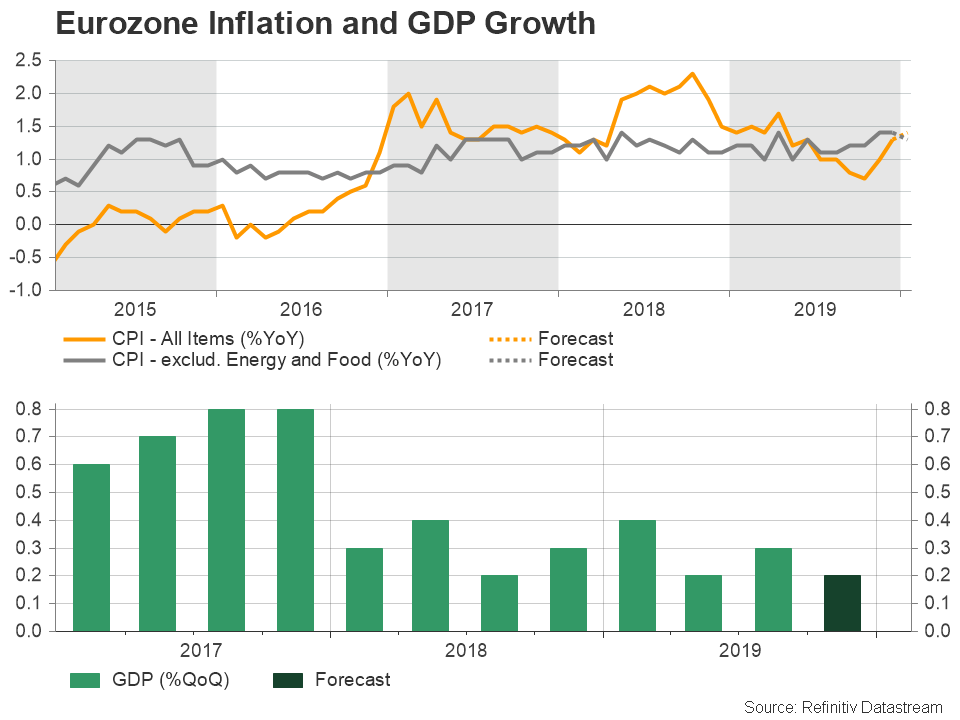

Eurozone economy chugging along (very slowly)

Preliminary fourth quarter GDP numbers for the euro area will come under the limelight on Friday but ahead of that, January business surveys will be the order of the day. Germany’s Ifo business climate index is out on Monday and the European Commission’s economic sentiment indicator is released on Thursday. Both are expected to show increases for January, consistent with the trend seen by other surveys such as the IHS Markit PMIs.

Moving to Friday’s data, which also includes flash inflation readings, the focus will be on how the Eurozone economy fared in the final three months of 2019. GDP is projected to have expanded by 0.2% quarter-on-quarter in Q4, slowing slightly from the prior 0.3% rate. If confirmed, it would underscore the view that growth in the region is stabilizing and that a rebound may be just around the corner.

The flash CPI report is also expected to support an improving economic picture. The headline rate of inflation is forecast to inch up from 1.3% to 1.4% year-on-ear in January, though the core rate is anticipated to tick down slightly to 1.3% y/y.

The euro, which has been drifting lower since the start of the year, is likely to accelerate its declines if the GDP print disappoints.

A more upbeat Fed?

Over in the US, it will be a packed week for data, but investors will also get to hear from the Fed, which will conclude its two-day monetary policy meeting on Wednesday. Starting with the economic releases for December, new home sales will kick-off the week on Monday, durable goods orders will follow on Tuesday, pending home sales are out on Wednesday and the personal income and outlays report will be closely watched on Friday.

Another solid increase in personal income and consumption is forecast for December, though the other key component of this report – the core PCE price index – is not anticipated to impress as the Fed’s favourite price gauge is expected to have held steady at 1.6% y/y.

In terms of surveys, the Conference Board’s consumer confidence index and the Chicago PMI will be monitored on Tuesday and Friday, respectively.

But the main highlights of the week will be the Fed meeting and the advance GDP estimate. The US economy is forecast to have grown by an annualized rate of 2.1% in the three months to December, the same pace as in the prior quarter. With earlier forecasts predicting a sharp slowdown in Q4, such a figure would be welcomed by the markets as well as Fed policymakers.

The recent brightening of the global growth outlook on the back of the trade war ceasefire will likely lead to the Fed sounding more confident about the American economy in its statement as it keeps policy unchanged.

The combination of an upbeat Fed and positive data would help the US dollar extend its latest gains as it scales 7-week highs against a basket of currencies. But safe-haven flows could also benefit the dollar if fears of a new pandemic were to intensify.

North of the border, it will be a relatively quiet week apart from Canada’s monthly GDP reading for November.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl