Week ahead – Fed minutes and Eurozone PMIs on the menu [Video]

-

Fed minutes on Tuesday will be scrutinized for clues on rate path.

-

Eurozone business surveys to shed some light on recession risks.

-

Japanese inflation stats also in focus as yen attempts to recover.

![Week ahead – Fed minutes and Eurozone PMIs on the menu [Video]](https://editorial.fxstreet.com/images/Macroeconomics/MonetaryPolicy/FED/washington-dc-federal-reserve-headquarters-close-up-38866062_XtraLarge.jpg)

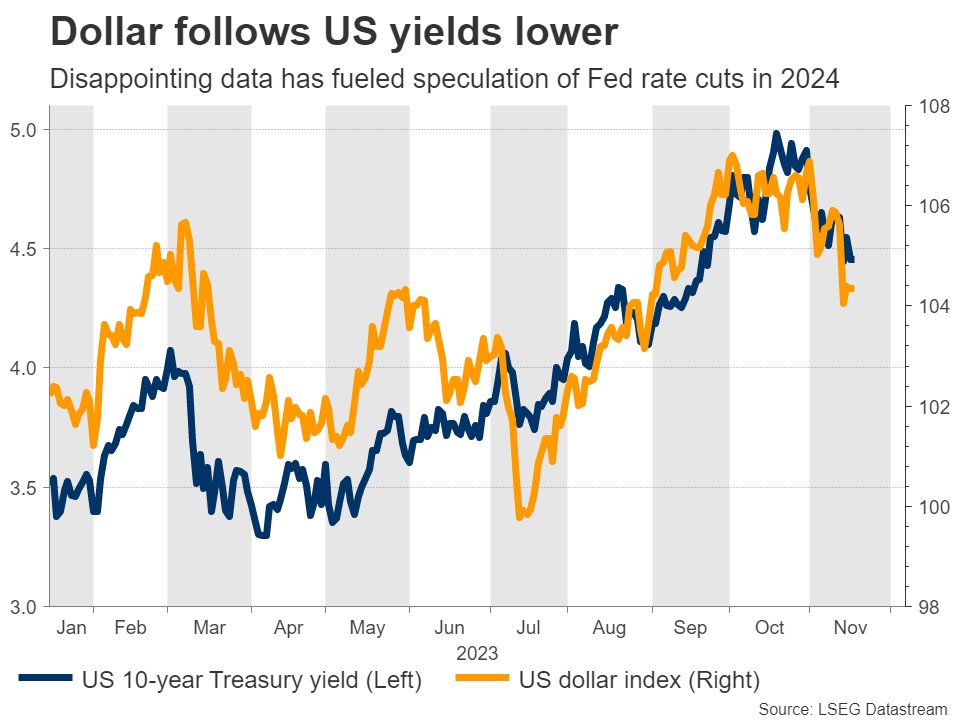

Bruised Dollar awaits FOMC minutes

It’s been a tough month for the US dollar. A string of disappointing data releases coupled with an announcement that the Treasury will shift its debt issuance towards shorter-dated maturities came together to engineer a heavy decline in US bond yields, which in turn has reduced the dollar’s interest rate advantage.

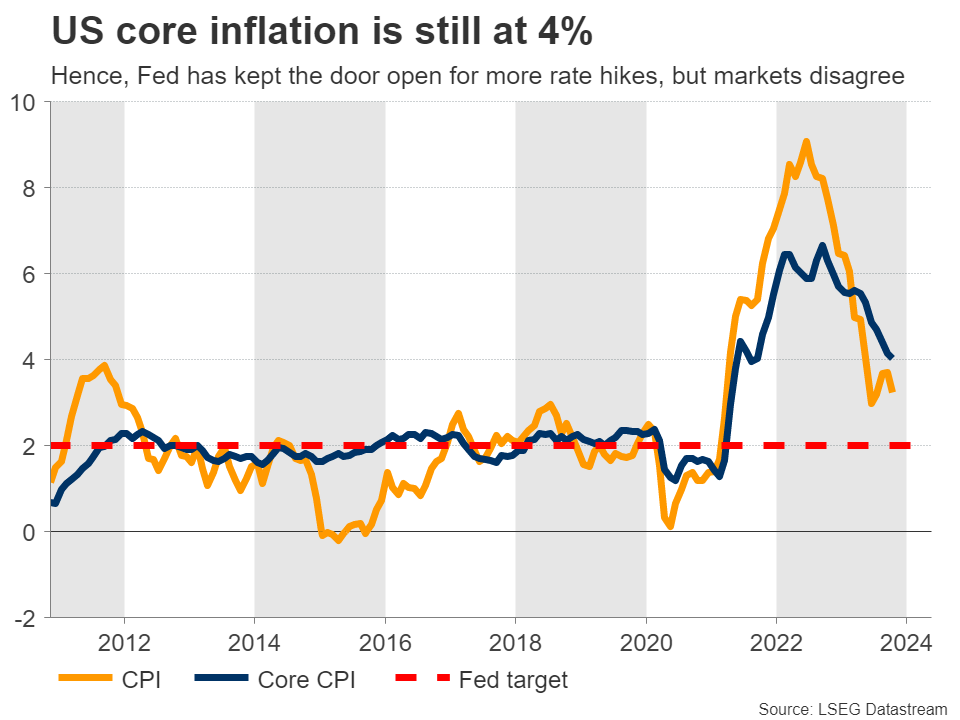

On the macro front, the labor market finally seems to be loosening. The unemployment rate has been grinding higher for several months now, providing some relief to Fed officials, as weaker employment conditions often translate into cooler inflation. Indeed, core inflation has declined steadily this year, but it remains elevated at 4%, so the Fed cannot declare victory yet.

With consumer spending also staying resilient, Fed officials have kept the prospect of another rate increase on the table. However, market pricing suggests the tightening cycle is already over and that the next move will be a rate cut, most likely in the second quarter of 2024. In light of this disparity, the upcoming FOMC meeting minutes could be crucial.

The minutes will be released on Tuesday, earlier than usual because Thursday is a public holiday in the United States. This was the meeting when the Fed kept rates unchanged and struck a neutral tone, highlighting that it is not certain whether rates are sufficiently high to bring inflation back under control.

Traders will dissect the minutes for any clues on the likelihood of further rate increases. However, even if the Fed provides such hints, it’s questionable whether markets will take them at face value, considering the series of disappointing data releases since this meeting. Hence, any upside reaction in the dollar from this release could be muted.

Beyond the minutes, there are several data releases on the agenda, including durable goods orders on Wednesday and the preliminary S&P Global PMIs for November on Friday.

All told, the question for FX traders heading into next year is which central banks will cut rates first and the deepest, since that will decide which currencies win or lose. That’s a setup that favors the dollar. The resilience of the US economy, especially when compared to Europe, suggests that the Fed might be among the last ones to launch an easing campaign.

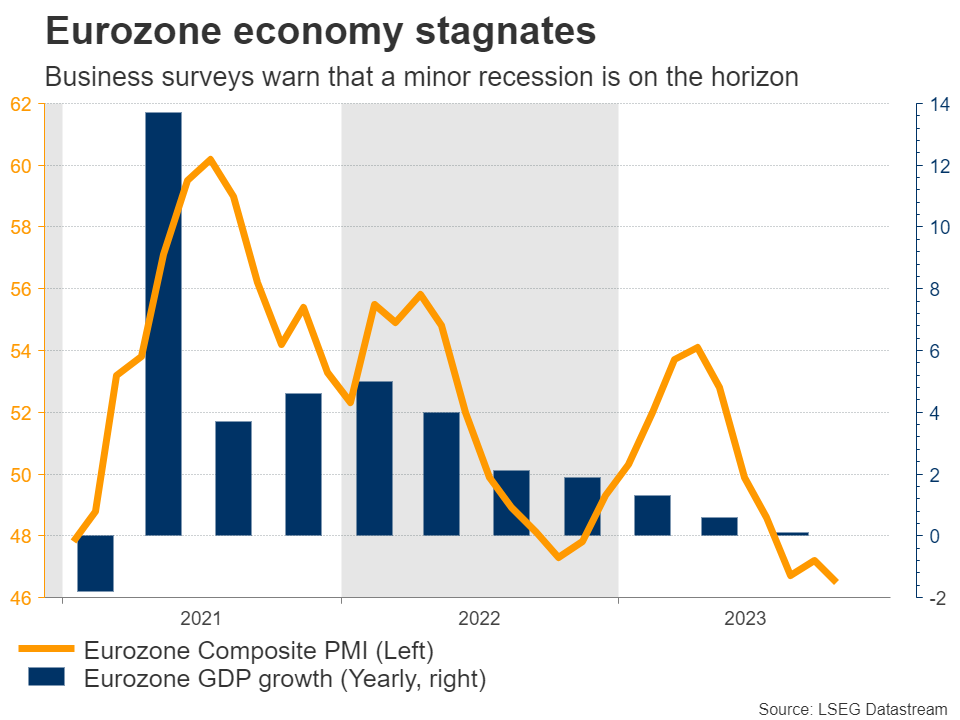

Euro and Sterling turn to PMI surveys

In the Eurozone and the United Kingdom, all eyes will fall on the latest round of business surveys on Thursday. Both economies are in similar shape, in the sense that economic growth has been stagnant for most of this year and might turn negative soon according to previous editions of these business surveys.

Europe seems to be entering a phase of stagflation, where the economy falls into a mild recession but inflationary pressures remain hot. That’s a nightmare scenario for any central bank, as cutting rates could refuel inflation but keeping them elevated could inflict more damage on the economy. This is particularly true in the UK, where core inflation is still running at 5.7%.

With all this in mind, the upcoming PMIs for November will provide an update on the health of these economies. Any further signs that the Eurozone and the UK are moving closer to a recession could dampen buying appetite in the euro and the pound, putting the brakes on the latest rebound.

Aside from the business surveys, the minutes of the latest European Central Bank meeting will also hit the markets on Thursday. This release is usually not a huge event for markets, but it could attract attention this time as traders attempt to decipher how quickly the ECB will start cutting rates. After that, the focus will turn to Germany’s Ifo survey on Friday.

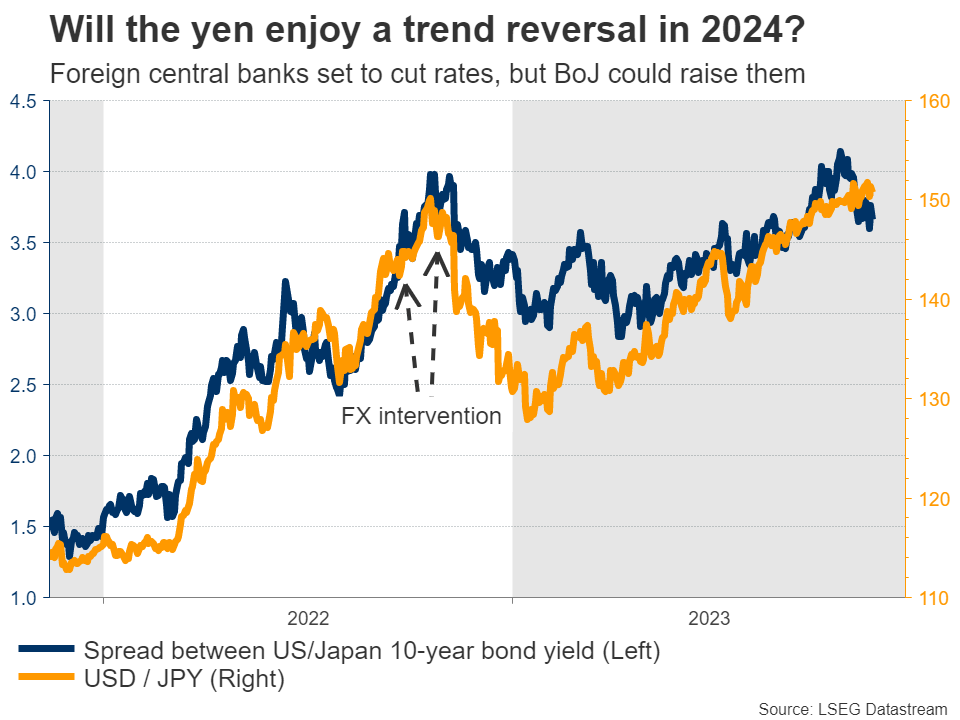

Japanese inflation numbers coming up

In the world’s third-largest economy, inflation stats for October will be released on Friday. The yen has been devastated this year, almost touching a three-decade low against the US dollar as interest rate differential widened against it.

Now, the question is whether the yen will get some relief next year, and perhaps even stage a trend reversal in an environment where foreign economies begin to cut interest rates while the Bank of Japan raises them. Market pricing suggests the BoJ will exit negative interest rates in the spring, helping to compress interest rate differentials.

Whether that happens or not will depend on the inflation outlook, which raises the importance of the upcoming data. Forecasts suggest that core inflation accelerated in October, something corroborated by a similar acceleration in Tokyo’s inflation that is considered a leading indicator of nationwide inflation. If this is the case, it could help the battered yen to recover some ground.

Meanwhile, inflation data will also be released in Canada on Tuesday, ahead of the latest edition of retail sales on Friday. Finally in Australia, the minutes of the latest RBA meeting are due out on Tuesday.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service