Week Ahead – Fed decides as pressure grows to pause rate hikes; BoE and BoJ meet too

The Federal Reserve’s policy meeting will be the main attraction next week as speculation grows the US central bank could signal slowing down the pace of rate hikes. Policy meetings by the Bank of England and Bank of Japan are not expected to draw as much attention. Instead, economic data will be grabbing the headlines for the rest of the week as inflation, retail sales and GDP figures are due for a number of major markets, including, Canada, Japan, the United Kingdom and the United States.

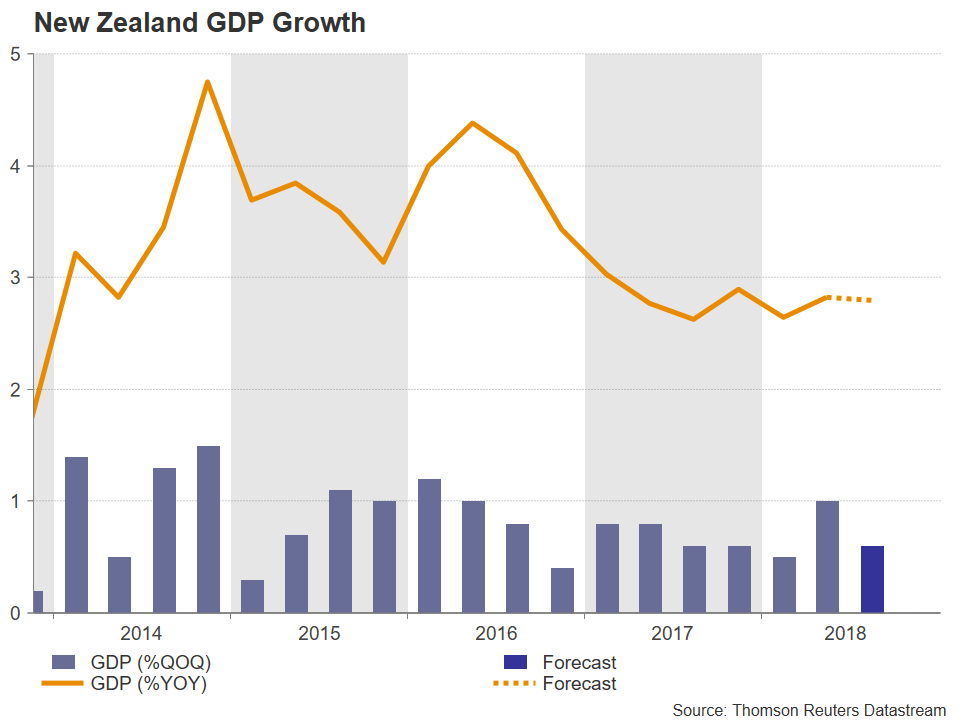

New Zealand to post Q3 GDP numbers

Somewhat late to the Q3 GDP party, New Zealand will publish its estimates of growth on Thursday. Ahead of that, the ANZ business outlook index for December will be watched on Tuesday, as well as third quarter current account figures on Wednesday. More trade stats will follow on Thursday with the release of monthly export data for November.

New Zealand’s GDP probably grew by a solid 0.6% quarter-on-quarter rate in the three months to September as other indicators for the period were mostly positive. However, business confidence remains low and could undermine future growth prospects. Any disappointing aspect from next week’s numbers could therefore push back the expected timing of a rate hike by the RBNZ, which would be negative for the New Zealand dollar.

The kiwi recently scaled a near 6-month high on the back of improving risk sentiment. The Australian dollar was another currency benefiting from the positive market mood. However, a worse-than-expected growth performance in Q3 in Australia later led to a pullback from those gains. Investors will next be looking to Thursday’s November employment report for clues to how the economy is faring in the current quarter, with the aussie likely to be sensitive to any surprises in the figures. Australia’s unemployment rate is expected to have held steady at 5% in November. Prior to the jobs data though, the RBA’s minutes of the December policy meeting will fall under the limelight on Tuesday.

Canadian inflation and retail sales eyed

Sticking to commodity-linked currencies, the Canadian dollar could be sailing through some choppy seas next week as several key releases are due out of Canada. Starting the week are manufacturing sales for October on Tuesday, followed by November CPI figures on Wednesday, and retail sales and GDP numbers for October on Friday.

A positive trend from next week’s economic gauges could help the loonie move off recent 1½-year lows. The currency has been struggling after the Bank of Canada struck a dovish tone at its December meeting, while the very modest rebound in oil prices hasn’t done the loonie any favours either.

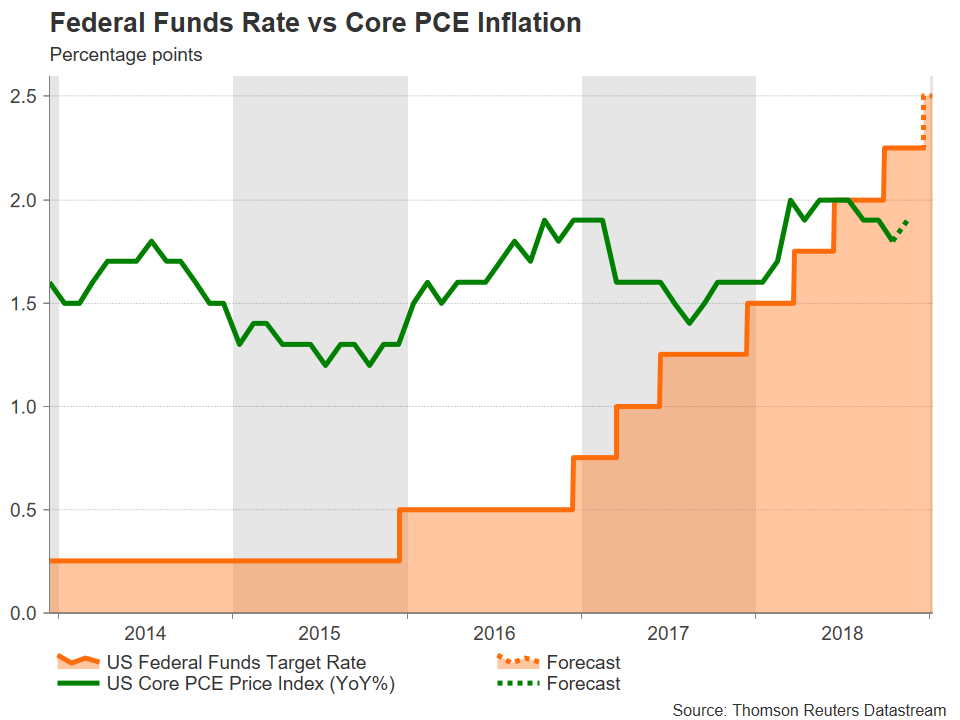

Will the Fed deliver a dovish hike?

The Fed will be the first of the major central banks to conclude its two-day monetary policy meeting on Wednesday. Federal Open Market Committee (FOMC) members are widely anticipated to raise the fed funds rate for the fourth time this year. But there has been rising speculation that the Fed is about to go into slower gear as fears mount of a global economic slowdown in 2019, with the recent slide in oil prices further dampening inflation expectations. Should the Fed forecast fewer rate increases in 2019 and also lower some of its growth and inflation projections, the US dollar could come under the firing line in forex markets.

Fed Chairman Jerome Powell will have to explain the central bank’s revised forecasts first to reporters, at the post-meeting press conference, and then to US lawmakers, at the Congressional testimony on Friday.

US data will also be watched next week with plenty of economic releases on the horizon. First up is the Empire State manufacturing index for December on Monday. On Tuesday, the focus will turn to the housing sector as building permits and housing starts for November are due, with existing home sales coming up on Wednesday. On Thursday, the Philly Fed manufacturing index is out, and on Friday, there will be a barrage of data to wrap up the week, including durable goods orders, final Q3 GDP estimates and the personal income and outlays report.

Durable goods orders are forecast to bounce back by 1.8% month-on-month in November after a 4.3% fall in the prior month, while the final estimate of third quarter growth is predicted to be left unrevised at an annualized 3.5% rate. But the highlight in Friday’s figures will likely be the PCE inflation and consumption numbers. Both personal income and spending are both forecast to rise by 0.3% m/m in November, easing somewhat from October. More importantly, the Fed’s preferred inflation measure, the core personal consumption expenditures (PCE) price index is forecast to edge up from 1.8% to 1.9% year-on-year in November, though this is still below the Fed’s 2% target.

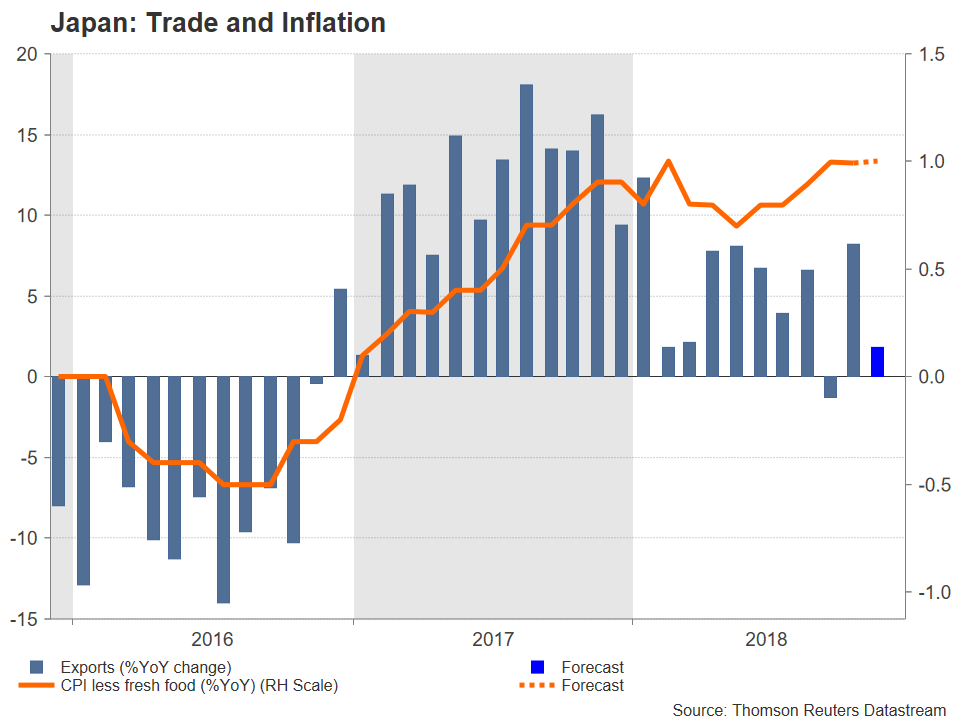

Bank of Japan to stand pat once again

Just hours after the Fed’s decision, the Bank of Japan will announce its policy decision on Thursday. The BoJ is not expected to make any changes to its ultra-loose monetary policy program as inflation has stalled around 1% and is not anticipated to reach the target before 2021. And with the Japanese economy losing some momentum in 2018, the BoJ is unlikely to make further tweaks to its stimulus program anytime soon.

Trade and CPI also due from Japan next week are expected to confirm the subdued growth and inflationary conditions. Data out on Wednesday is forecast to show annual export growth slowed to just 1.8% last month. Inflation figures will follow on Friday, with core CPI projected to stay unchanged at 1% y/y in November.

The yen could see some small reaction from any surprises in the numbers or the BoJ’s statement. However, yen traders will probably be paying more attention to what the Fed says and how the trade war story plays out in the next seven days.

No changes from Bank of England

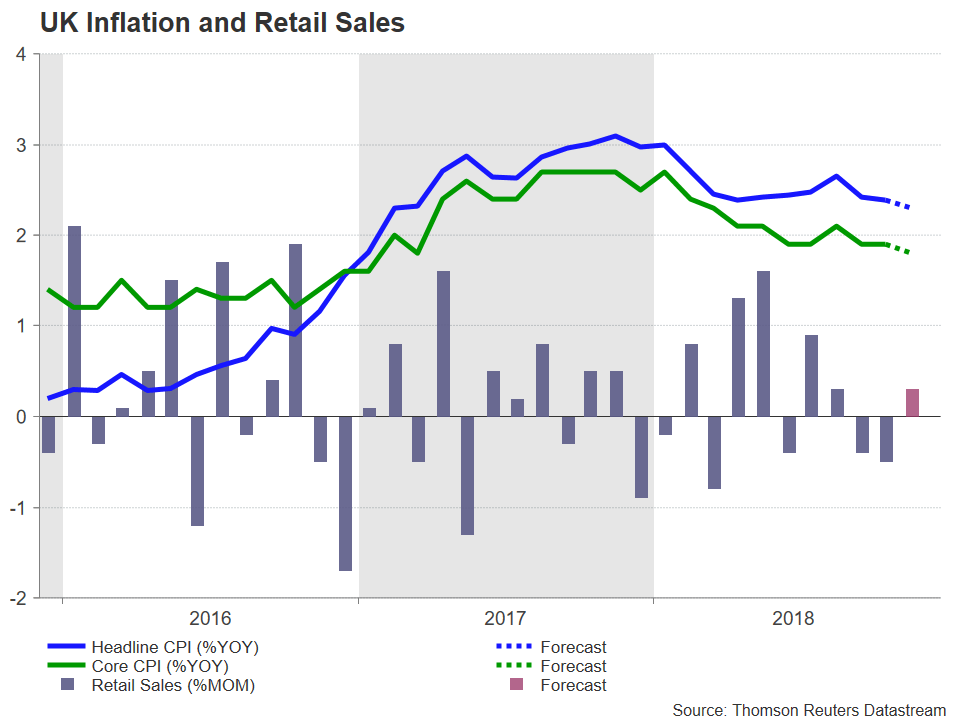

As British politicians continue to wrangle over Brexit, UK economic indicators could once again take the backseat, especially if the prime minister, Theresa May, decides at the last minute to reschedule the vote for her Brexit deal for next week. Nevertheless, the flurry of releases as well as a Bank of England policy meeting run the risk of adding to sterling’s bearishness.

The November CPI report is out on Tuesday and the headline rate is forecast to ease to 2.3% y/y from 2.4%. The core rate is also expected to moderate, to 1.8%. Retail sales will follow on Thursday, and finally on Friday, the second estimate of GDP growth for the third quarter will be published, with no revision being predicted to the initial reading of 0.6% q/q.

Moving back to Thursday, when the BoE will announce its latest monetary policy decision, the meeting could turn out to be a non-event as there will be no press-conference or quarterly projections. However, it’s possible the BoE could sound more cautious in its statement as the Brexit uncertainty and political turmoil have started to take their toll on the UK economy. Any dovish tilt in the wording of the statement would pressure the pound, which this week touched a 20-month low.

Quiet week for the Eurozone

The euro could struggle to break out of its current tight range over the next week or so as the Eurozone calendar is looking relatively light. The only major releases are the final November CPI print (Monday) and the German Ifo business sentiment survey (Tuesday). The closely-watched Ifo business climate index is expected to slip further in December from 102.0 to 101.7. Lastly, the flash reading of the Eurozone consumer confidence index for December is due on Friday.

Also noteworthy in Europe next week is the policy meeting by the Riksbank – Sweden’s central bank – on Thursday. The Riksbank has indicated that it plans to begin raising its repo rate either in December or February. December had been the favourite by many analysts but recent soft data on GDP and inflation have lowered the odds for a hike this month to around 50%. If the Riksbank delays a move but strongly signals an increase in February, the Swedish krona is unlikely to suffer significant losses. However, if the central bank lowers its forecasts for the repo rate, the krona could come under selling pressure.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.