6.5% producer inflation: The problem rate hikes can’t solve

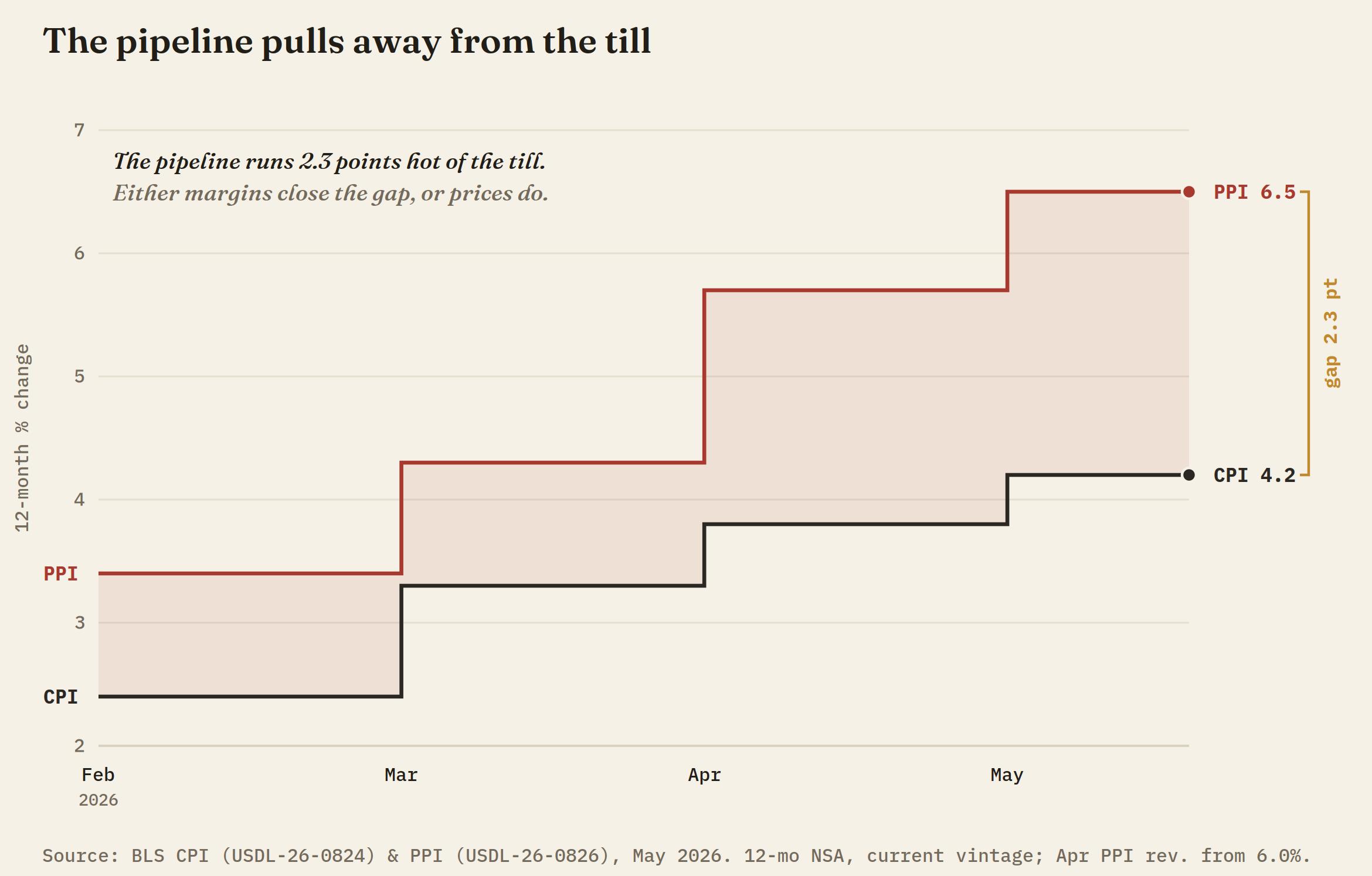

Part one of this series closed on a single question: whether the pipeline agrees with the pump. Thursday answered it emphatically. May's Producer Price Index (PPI) rose 1.1% on the month against a 0.7% consensus, the second straight month at that pace, and the annual rate hit 6.5%, the largest 12-month climb since November 2022. The pipeline agrees with the pump because the pipeline mostly is the pump.

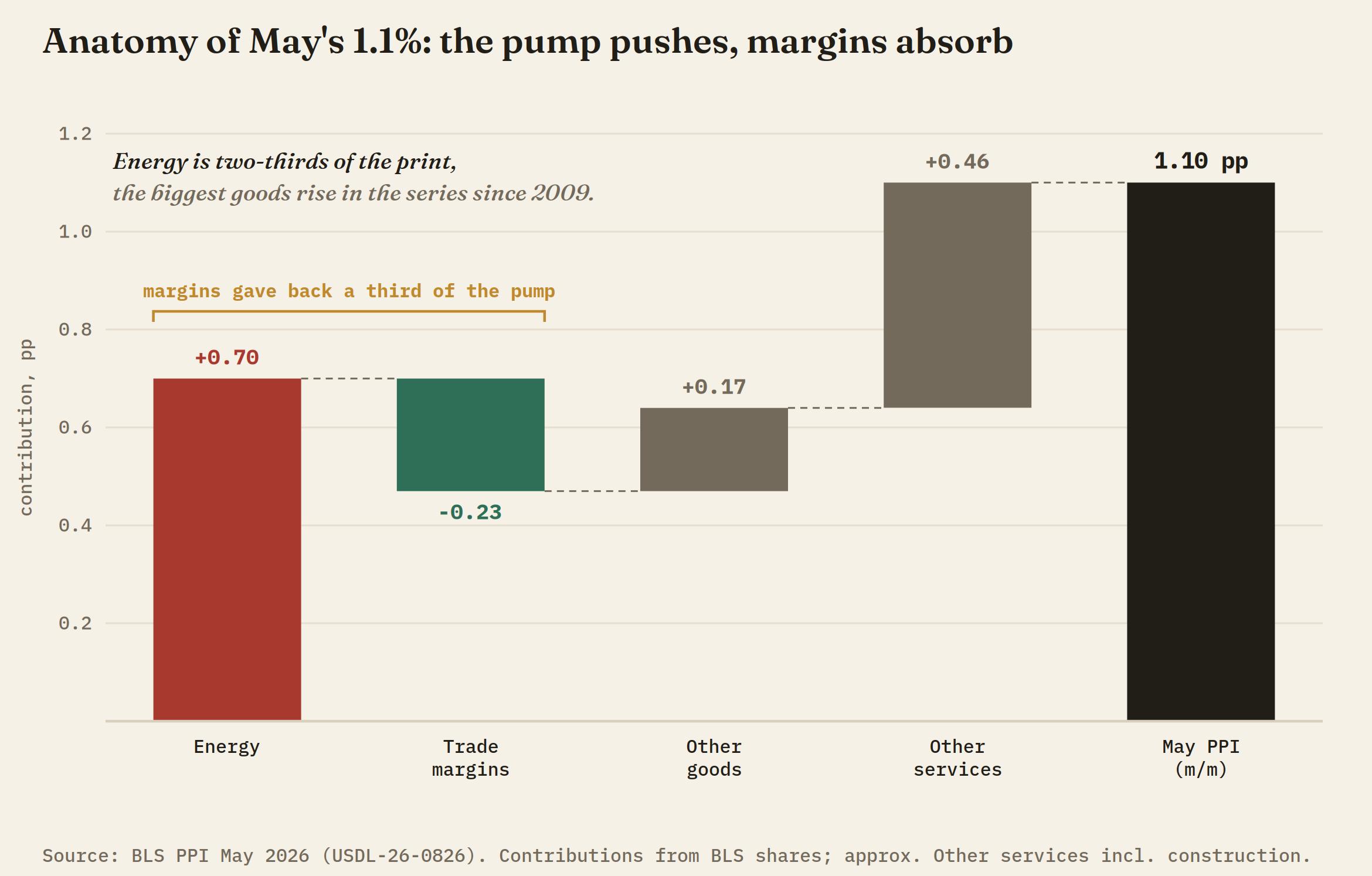

The Bureau of Labor Statistics (BLS) traced nearly 80% of the monthly advance to goods, which jumped 2.8%, the largest rise in the series going back to 2009, and roughly 80% of that to energy alone, up 10.7%, with wholesale gasoline rising 23.4% in a single month. Strip the war out and the core pipeline missed on both axes. So the print answers a better question than the one part one asked: not whether costs are rising, but who is being made to pay them. For the Federal Reserve (Fed), that distinction is the whole game.

The pipeline is the pump

Diesel, jet fuel, plastic resins, industrial chemicals and natural gas liquids all followed gasoline higher, the full fingerprint of a crude shock working through the cost base. Even history is being marked by the war: April's monthly jump was revised down to 1.1% from the 1.4% first reported, and the annual rate still printed its hottest since 2022. With the Strait of Hormuz shut, Brent back through $95 and West Texas Intermediate (WTI) above $92 overnight, June's wholesale energy line is already half-written.

Margins are eating the war tax

Core PPI rose 0.4% in May against a 0.5% consensus, and the annual rate held flat at 4.9%, half a point under the 5.4% the market expected. The sharper signal sat one line lower: trade services margins fell 1.1% on the month, with machinery and equipment wholesaling margins down 1.9% and fuel retailing margins lower outright. Wholesalers and retailers are absorbing the energy shock, not passing it. That is the producer-side twin of Wednesday's consumer print, where transportation services fell during a month when gasoline rose 7%.

Margin compression only ever resolves two ways. Either firms eventually push the cost through, which is the lagged inflation the hawks are warning about, or they cut costs instead, which is how a price shock turns into a labour story. Initial jobless claims printed 229K on Thursday, a three-month high against a 219K consensus, an early vote on which exit is being used.

The hawks' card is real this time

Honesty requires the other column. Excluding food, energy and trade services, producer prices rose 0.8% in May, the hottest monthly reading since March 2022, and 5.1% on the year, the most since October 2022. Transportation and warehousing services jumped 2.6% as fuel worked through freight rates, which makes wholesale logistics the second confirmed passthrough channel after the airline fares flagged in part one. Upstream, prices for processed goods in intermediate demand rose 3.5%, so the queue behind the headline is not empty.

The skeptic's reply is about composition, not direction. The hot ex-trade core leans on fuel-adjacent freight and on portfolio management fees, up 4.8% after a strong month for stocks, which is asset-price beta rather than an overheating economy. Two confirmed channels, and both smell of jet fuel. A rate hike can make money dearer; it cannot make a tanker cheaper to insure.

Frankfurt jumped first

The European Central Bank (ECB) raised rates by a quarter-point on Thursday, its first hike since 2023, lifting the deposit rate to 2.25% and revising its inflation projections higher on the energy path to 3% this year. It did so into an economy that contracted in the first quarter, with markets already leaning toward another move before year-end. Part one called this the Trichet test, after the ECB's July 2008 decision to hike into a supply-driven Oil spike. Frankfurt has now taken that test live, and Kevin Warsh gets to watch the result land before his own committee sits.

The war loop ran on schedule too. The strikes President Donald Trump promised on Wednesday arrived overnight, Tehran answered at US bases and declared the strait closed, and Oil gapped higher in Asia. By the New York morning, Washington was calling the round complete and talking up a diplomatic lane, and some of the premium bled back out. The single largest input into the next inflation print is still being set by ordnance, not by the funds rate.

The bid did not blink

The US Dollar Index (DXY) gave up the 100.00 handle overnight, spent Asia underneath it, bought it back through the London morning and has not surrendered it since. The 12:30 GMT release wicked the tape both ways and resolved higher within the hour. Wednesday's soft consumer core bought the bears three hours; Thursday's soft pipeline core bought them minutes.

As New York trades, the index sits near session highs roughly midway between the handle and the 100.50 spring ceiling, firmer on the day, the intraday tape as it stands a study in dips being bought. Both engines from part one are still running: the December hike refuses to price out of the strip, and the war premium refreshed itself overnight before the talks headlines let some of it bleed. A market this unwilling to sell either a hot headline or a soft core has decided which number the Federal Open Market Committee (FOMC) answers to.

Levels and the lean

100.00 has flipped from Wednesday's battleground to Thursday's floor. The lean stays higher while the handle holds on a closing basis, and dips remain for buying. Lose it and 99.50 is the first shelf, with 99.00 still the line in the sand at the 50 and 200 EMA cluster; below there the hike premium built since mid-May starts unwinding toward 98.00. Above, 100.50 is the spring ceiling and the April cap, and a daily close through it on hot expectations data pulls the December pricing forward and reopens the second-hike conversation.

The last input before the meeting lands Friday at 14:00 GMT, when the University of Michigan (UoM) survey updates household inflation expectations from the 4.8% one-year reading the hawks have been anchoring to. Then the FOMC sits on Tuesday and Wednesday, with the decision and Warsh's debut press conference on June 17.

Part one asked what a December hike would be aimed at. The pipeline has now answered: a war tax the Fed cannot repeal, and a margin squeeze a hike can only deepen. Frankfurt chose to be seen fighting the wrong inflation rather than be accused of ignoring it. Next Wednesday, we find out whether Warsh reads that as cover or as a warning. The funds rate prices money; it does not price the strait.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.