The ECB dilemma: Higher inflation, weaker growth and no clear rate path

The European Central Bank (ECB) raised interest rates on Thursday as the war in Iran and energy disruptions revive inflationary pressures in the Eurozone. The key question for traders, which Lagarde dodged elegantly, is whether this is just a one-off hike to preserve credibility or the first of many increases.

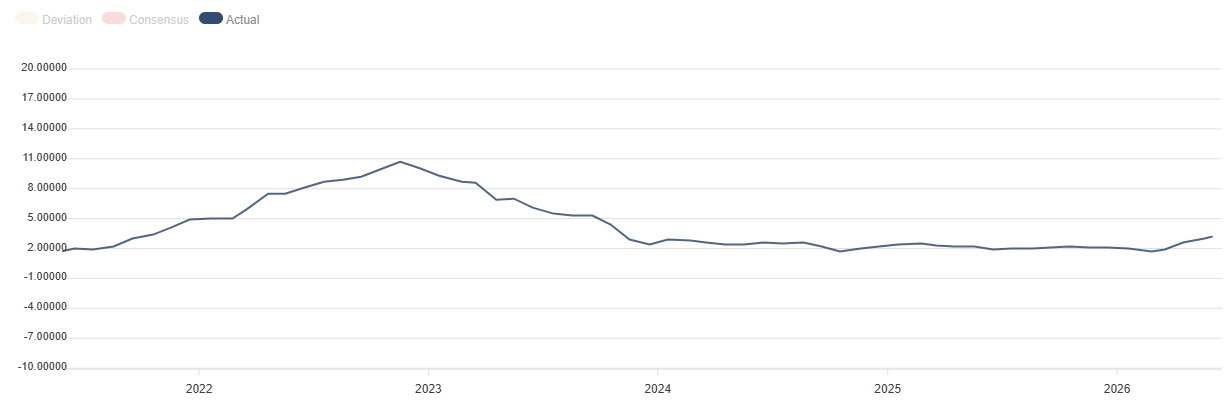

After several quarters of monetary stability, the Frankfurt-based institution acted as inflation accelerated to 3.2% YoY in May and core inflation rose to 2.5%.

The 25-basis-point increase marks the ECB’s first rate hike since September 2023, after an easing cycle that brought the deposit rate down from 4% to 2%.

A rate hike that was fully priced in

The sharp rise in energy prices, linked to the war in Iran and disruptions around the Strait of Hormuz, has shifted the balance of risks for the ECB. The institution is not facing an inflationary spiral comparable to 2022, but it must prevent the current energy shock from passing durably into wages, services and industrial goods prices.

The ECB’s updated projections reinforced the rationale behind Thursday’s decision. In the baseline scenario prepared by Eurosystem staff, headline inflation is now expected to average 3% in 2026, 2.3% in 2027 and 2% in 2028. Core inflation is projected at 2.5% in both 2026 and 2027 before easing to 2.2% in 2028. Compared with the March projections, inflation forecasts for 2026 and 2027 were revised higher due to a more persistent energy price shock.

However, the ECB also highlighted the unusually high degree of uncertainty surrounding the outlook through updated alternative scenarios. In the adverse scenario, where energy disruptions prove more persistent, headline inflation would average 3.3% in 2026 and remain elevated at 3% in 2027. Conversely, in a newly introduced mild scenario, inflation could fall more quickly if energy prices decline faster than expected, averaging 2.9% in 2026 before dropping to 1.8% in both 2027 and 2028. This would see inflation fall back below the ECB’s 2% target as early as next year, illustrating the wide range of possible outcomes policymakers are currently facing.

What happens after June?

The main issue for markets is not what happened today, but what will happen next. ECB President Christine Lagarde offered few clues regarding the timing of any future move. She repeatedly stressed that the Governing Council would remain data-dependent and continue to assess incoming information meeting by meeting.

While she acknowledged that inflation risks remain tilted to the upside and that price pressures are beginning to broaden beyond energy, she also highlighted weaker domestic demand, cooling labor market conditions and downside risks to growth stemming from the Middle East conflict. Importantly, Lagarde said the Governing Council did not discuss alternative policy options and insisted that Thursday’s decision should not be viewed as an “insurance hike.”

Analysts at UniCredit say the timing of any further hike will largely depend on the war, shipping through the Strait of Hormuz and energy prices. The bank forecasts limited tightening, with a final hike in September bringing the deposit rate to 2.5%.

This cautious approach is also supported by several economists who stress that the current environment is very different from 2022. At that time, inflation was already very high before the energy shock triggered by Russia’s invasion of Ukraine, households had more excess savings, and fiscal measures provided stronger demand support. Today, the Eurozone is facing fragile growth, tighter credit conditions and still-limited signs of second-round wage effects.

The risk of excessive tightening

The ECB is nevertheless facing a delicate dilemma. No action could be interpreted as a lack of determination against inflation running above the 2% target. But excessive tightening could worsen the economic slowdown in an already vulnerable Eurozone.

The new macroeconomic projections highlighted the ECB’s difficult balancing act. The central bank revised its inflation outlook higher, while warning that higher energy prices could continue to feed through into other sectors of the economy. At the same time, growth projections remain subdued, with Eurozone Gross Domestic Product (GDP) expected to expand by just 0.8% in 2026, before accelerating modestly to 1.2% in 2027 and 1.5% in 2028. The ECB explicitly stated that risks to inflation remain on the upside, while risks to economic growth are skewed to the downside.

This combination of higher inflation and weaker growth increases the risk of stagflation. It complicates the ECB’s task, because monetary policy can curb demand but cannot directly solve an energy-driven supply shock.

A hike, but not necessarily the start of a long cycle

The most likely scenario after the June rate hike is cautiously restrictive communication. The ECB signaled that it remains prepared to respond if inflationary pressures intensify further, but Lagarde carefully avoided suggesting that additional rate increases are already planned. She emphasized that there would be no pre-set rate path and no forward guidance under the current circumstances. While the central bank acknowledged that inflation is beginning to broaden and that short-term inflation expectations have risen, it also noted that longer-term inflation expectations remain broadly anchored around the 2% target.

Some institutions, such as Nordea, expect several consecutive hikes, with the deposit rate potentially reaching 3% in October. Others, such as ING and UniCredit, favor a much more limited scenario, with one or two additional hikes at most. Market consensus currently appears to sit between these two views, with two to three moves possible over the full year.

Thursday’s decision should therefore be seen less as the mechanical start of a new tightening cycle than as a credibility test for the ECB. If energy prices remain elevated, core inflation continues to accelerate and inflation expectations deteriorate, the institution may have to extend the move. However, if energy tensions ease during the summer and the economy slows further, the June hike could remain largely a short-term adjustment.

For investors, the tone of Christine Lagarde’s press conference ultimately proved as important as the rate decision itself. While the ECB delivered a clearly hawkish message on inflation, it stopped short of validating expectations for a sequence of imminent hikes.

The ECB attempted to strike a delicate balance, acknowledging that the inflation outlook has deteriorated and that further action may be required if price pressures broaden, while simultaneously insisting that future decisions will depend entirely on incoming data and developments in energy markets.

Economic Indicator

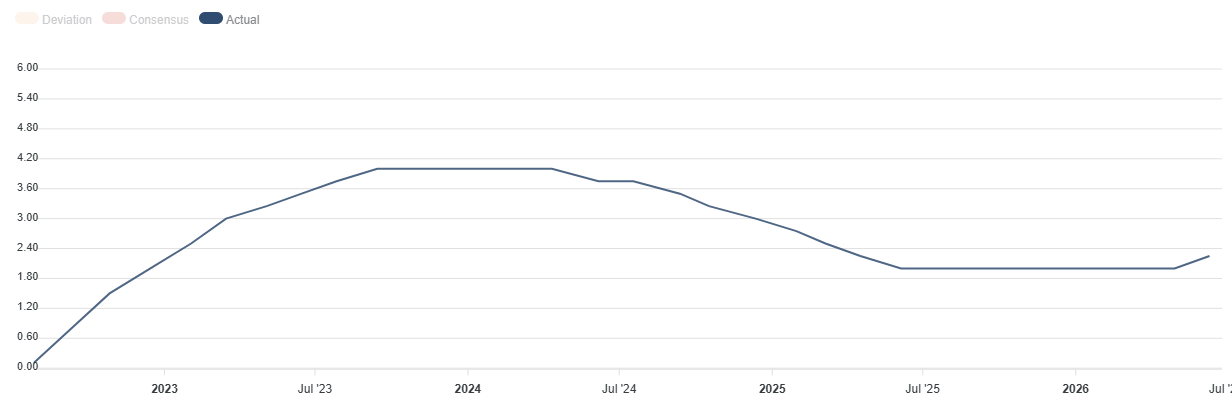

ECB Rate On Deposit Facility

One of the European Central Bank's three key interest rates, the rate on the deposit facility, is the rate at which banks earn interest when they deposit funds with the ECB. It is announced by the European Central Bank at each of its eight scheduled annual meetings.

Read more.Last release: Thu Jun 11, 2026 12:15

Frequency: Irregular

Actual: 2.25%

Consensus: 2.25%

Previous: 2%

Source: European Central Bank

ECB FAQs

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy for the region. The ECB primary mandate is to maintain price stability, which means keeping inflation at around 2%. Its primary tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

In extreme situations, the European Central Bank can enact a policy tool called Quantitative Easing. QE is the process by which the ECB prints Euros and uses them to buy assets – usually government or corporate bonds – from banks and other financial institutions. QE usually results in a weaker Euro. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The ECB used it during the Great Financial Crisis in 2009-11, in 2015 when inflation remained stubbornly low, as well as during the covid pandemic.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the European Central Bank (ECB) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the ECB stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Euro.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.