Week Ahead – Central banks and US Q3 GDP in focus; BoC poised to raise rates

Central bank meetings will take centre stage in the coming week as economic data will be in short supply. With four policy meetings lined up, comprising the European Central Bank, the Bank of Canada, the Riksbank and the Norges Bank, only the BoC is anticipated to take action next week. The preliminary reading of third quarter GDP growth in the United States will likely be the most highly awaited release of the week, followed by the October flash PMIs in the Eurozone, the US and Japan.

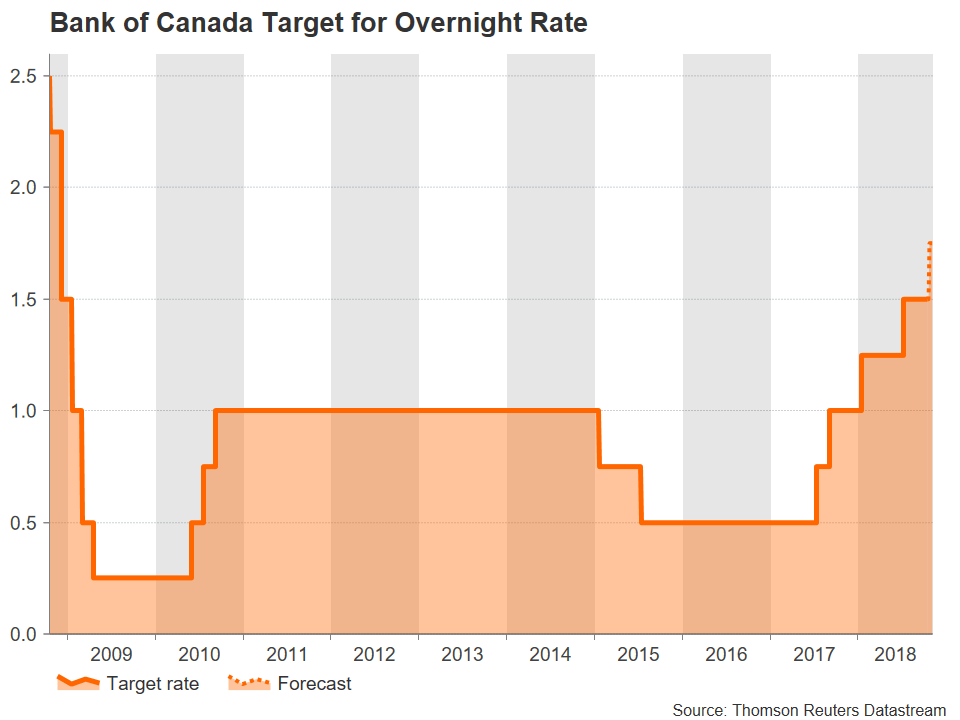

Bank of Canada to hike again

The BoC has been one of the few central banks among advanced economies other than the Federal Reserve that’s been able to raise interest rates beyond crisis era levels. Having increased rates four times since 2017, the BoC is expected to deliver another 0.25% rate hike on Wednesday when it announces its latest policy decision. The market odds for a rate increase have been rising since the successful conclusion to the NAFTA renegotiation earlier in the month and a bullish quarterly business survey by the BoC this week. However, the Canadian dollar has been weakening after that initial lift from the trade deal as oil prices have been on a downtrend in October. The loonie may be able to get on a stronger footing if the BoC accompanied its rate hike with a hawkish outlook.

ECB to meet amid Italy tensions and growth worries

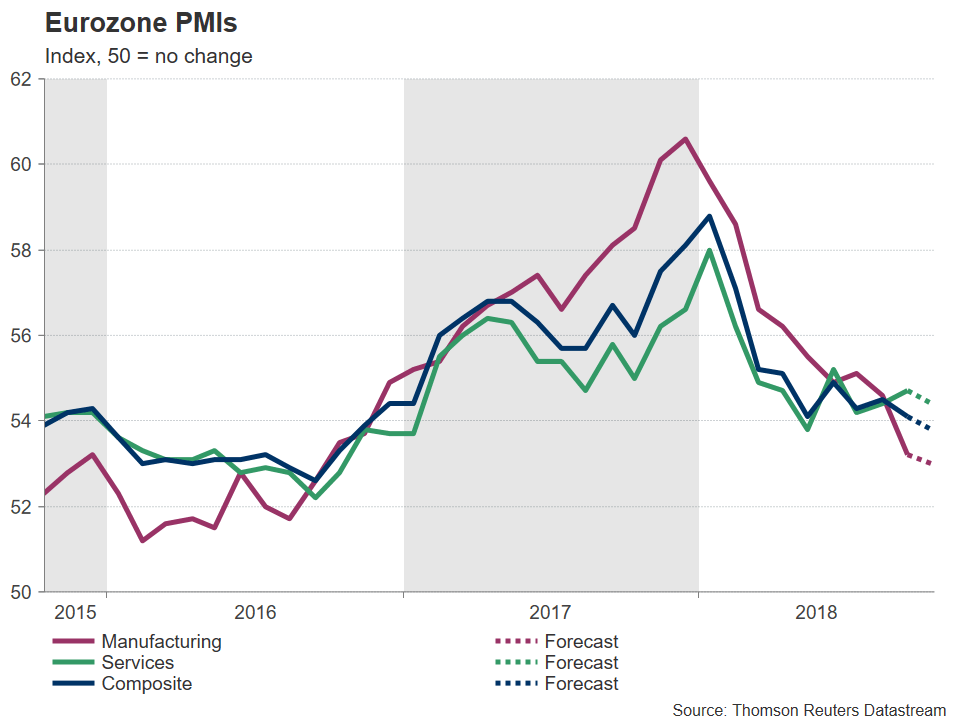

The euro will be under the spotlight next week, as apart from the ongoing drama with the Italian budget, the flash PMIs for the Eurozone and an ECB meeting will be drawing investors’ attention. The Eurozone’s economy has been unable to regain steam after a notable slowdown at the start of 2018. The ECB has insisted the region’s fundamentals remain strong as it readies to conclude its asset purchase program at the end of December. However, investors are more sceptical about the growth outlook and this cautiousness is one of the reasons why many analysts are bearish on the single currency for the next few months. Another reason is the stand-off between Italy and the European Union over Italy’s budget deficit targets, which looks set to escalate in the coming weeks as the EU will likely reject the submitted plans.

ECB chief Mario Draghi will probably have to address these concerns when he holds a post-meeting press conference on Thursday. As for the policy decision itself, the ECB is widely anticipated to keep policy on hold in October.

Reassuring comments from Draghi may provide some support to the euro, but traders shouldn’t expect any reprieve from economic indicators. The flash estimates of Eurozone PMIs by IHS Markit, due on Wednesday, are set to show further deterioration in economic momentum. The manufacturing PMI is forecast to decline further in October, falling to 53.0 from 53.2, which would be a two-year low if confirmed. The services PMI is also forecast to drop, from 54.7 to 54.4, suggesting no rebound in sight just yet for the euro area. Another important business sentiment gauge will be the German Ifo survey on Thursday. The Ifo’s business climate index is not expected to buck the trend, slipping from 103.7 to 103.2 in October.

Riksbank and Norges Bank to stand pat

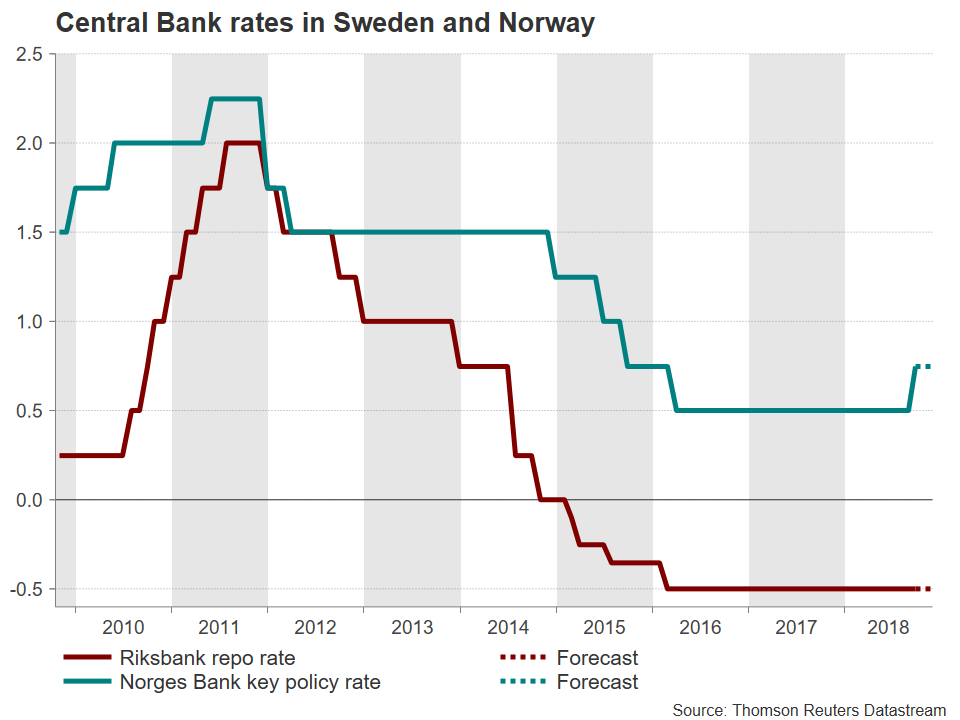

Sweden’s central bank, the Riksbank, will announce its policy decision on Wednesday ahead of the ECB’s announcement. Inflation in Sweden has been slowly edging up in recent months but at its last policy meeting in September, the Riksbank pushed back the timing of the first rate hike since 2011 to December/February from earlier forecasts of October/December. Although stronger-than-expected CPI readings for September raised the odds of a rate hike arriving in December, February remains very much in play and policymakers will possibly use next week’s meeting to provide clearer guidance.

The Swedish krona has firmed by around 2% versus the US dollar and the euro since last week’s inflation data and could extend those gains if policymakers signal a rate hike before year-end.

But as the Riksbank hesitates whether or not to tighten policy, neighbouring Norway’s central bank has already begun the process, raising rates in September from 0.50% to 0.75%. The next hike is not anticipated until the first quarter of 2019 and the Norges Bank is almost certain to keep rates unchanged at its meeting on Thursday. The Norwegian krone is therefore unlikely to see much reaction to the central bank’s decision unless there’s a surprise tweak to the projected rate path.

US GDP likely slowed in Q3

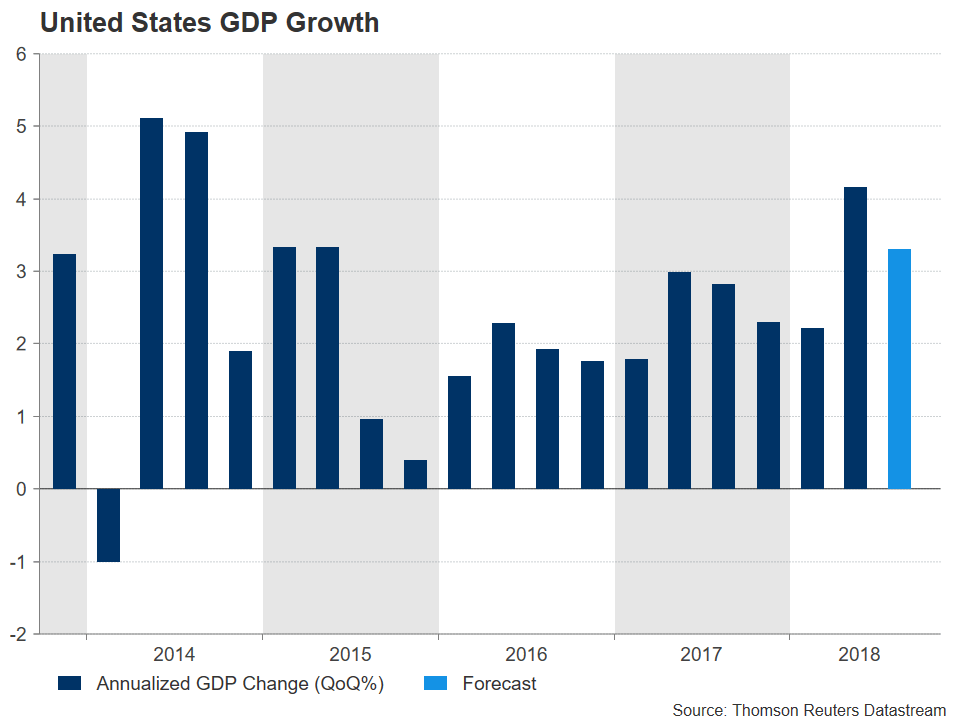

The US will have the busiest calendar next week with Friday’s GDP numbers being the highlight. Before then though, attention will fall on October flash PMIs and September new homes sales on Wednesday. IHS Markit’s manufacturing PMI is expected to stay unchanged at 55.6 in October’s preliminary reading, while the services PMI is projected to rise slightly from 53.5 to 53.9. On Thursday, the latest durable goods orders are due along with the advanced trade balance and pending home sales, all for September. Durable goods orders are forecast to have fallen back by 2.3% month-on-month in September after a 4.4% gain in the prior month. However, core capital goods orders, which are a more accurate indication of the business spending component of GDP, are expected to have increased by 0.3% m/m in September.

On Friday, investors will get the first look at US growth for the three months to September. Following the robust 4.2% annualized expansion of the second quarter, growth is forecast to have moderated to 3.3% in the third quarter, which still represents above trend growth for the US economy. The dollar, which against a basket of currencies has been consolidating since mid-August, could resume its uptrend if there is an upside surprise to the GDP figures. Though, with US stocks being sensitive to big jumps in Treasury yields, another potential sell-off on Wall Street could cap gains for the greenback if strong data drive up long-term Treasury yields to uncomfortable levels.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.