Week Ahead: Beginning of End for Trade War and Brexit Uncertainties?

Economic data will be winding down as year-end approaches, although there are still a few important events scheduled for next week. Investors certainly seem to be in a buoyant festive mood as we head towards Christmas. The US and China finally agreed to a phase one trade agreement, which will be signed when the two sides work through the legal process. On top of this, political uncertainty has receded in the UK with the Conservatives winning majority of the votes in Thursday’s election.

Here are the highlights of what’s coming up over the next 5 and half trading days:

Manufacturing and services PMIs

- Monday will see the release of the latest Purchasing Managers’ Indices (PMI) data from around the world, including Australia, Japan, the Eurozone, UK and US. Given that the major central banks are now in a wait-and-see mode, any noticeable changes in incoming data may impact markets’ expectations over interest rates, and in turn currencies. This is where the PMI data comes handy as they provide leading indication of economic health, with purchasing managers tend to react first to changing market conditions.

- Among them, it is the Eurozone PMIs which are perhaps the most important to watch given the recent protests in France and uncertainty over Brexit. On top of this, there are concerns over weak economic performance in the single currency block, partially as a result of the damaging trade war between the US and China and ongoing currency crises in Latin America hurting demand. All this may mean another month of weakening activity in Eurozone’s manufacturing and services sectors. So, there is a risk the EUR/USD could fall back after rising for two weeks.

- Note that the latest US-China trade and Brexit developments will unlikely show up in the PMIs, as the surveys were likely conducted days ahead of the Thursday’s UK election and Friday’s news of US and China agreeing to a phase one deal (see below).

Central banks likely to hold fire

- Following this week’s central bank bonanza (for the lack of a better word) there are only two major bank meetings to look forward to: Bank of Japan and Bank of England. As it turned out, inaction from both the ECB and Fed failed to provide any major volatility this week as we had suspected, while the Turkish lira whipsawed after the nation’s central bank slashed its benchmark interest rate for the fourth time this year to 12%, more than 12.5% expected.

- In light of the UK election, the Bank of England will now be looking for a quick rebound in UK data, since it has been election and Brexit uncertainties that have led to the recent soft patch in UK data. However, it is far too early for UK data to show improvement from the outcome of the elections, and it could be months before we see the potential rebound. So, the BoE will likely remain cautious and keep monetary policy unchanged – but may provide a more upbeat outlook over the short-term economic performance. However, if domestic data does not improve in a few months’ time, then a rate cut could be on the cards in mid-2020 regardless of the Brexit situation. But our assumption is that we may see households and businesses – who have repeatedly delayed their purchases and investments – splash the cash and boost growth. The potential for pent up demand means the economy should grow a little more robustly which in turn could support sterling’s recovery towards high $1.30s or low $1.40s in 2020.

- Bank of Japan has resisted the temptation to go further lower in negative territory for interest rates while other banks loosened their policies. Receding concerns over a disorderly Brexit and signs of progress in US-China trade talks means there is less pressure on the BOJ to unleash more stimulus at this meeting, even if domestic data continues to deteriorate.

Other important macro events this week:

- China: Industrial Production, Fixed Asset Investment and Retail Sales y/y (all on Monday)

- Australia: RBA Monetary Policy Meeting Minutes (Monday) and Employment Change (Thursday)

- New Zealand: ANZ Business Confidence (Tuesday), GDP (Thursday)

- UK: Average Earnings Index and Jobless Claims (Tuesday), CPI and other inflation measures (Wednesday), and Retail Sales and BoE rate decision (both Thursday).

- Canada: CPI (Wednesday) and Retail Sales (Friday)

- US: There’s a data dump on Tuesday when we have the latest Housing Starts, Building Permits, Industrial Production, JOLTS Job Openings and IBD/TIPP Economic Optimism. Then another one on Friday, which includes Final GDP, Core PCE Price Index, Personal Spending and Personal Income.

So, there should be lots of news-driven moves for currencies of the above nations. Outside of the above economic data releases, further developments in the US-China and Brexit situations will likely move the markets.

Brexit: Getting there…

Following the Tories’ big win in the elections, further delays to Brexit look unlikely now, meaning households and businesses can plan accordingly – this is exactly why the markets have reacted in the way they have, with both the pound and FTSE rising sharply, before profit-taking saw the pound gave back a sizeable chunk of its overnight gains on Friday. The pound could see short-term dips being bought next week as traders continue to price in the prospects of UK’s softer exit from the EU. But the longer-term outlook remains murky given that negotiations on trade haven’t even started yet – and a lot could go wrong.

Phase I: Done

The US-China trade optimism continued to drive stock prices higher this week, although markets were struggling to hold onto their gains on Friday after China confirmed that they had reached a consensus on the text of phase one trade deal with the US, and that they will work on setting a date for signing it. China said it will boost US imports of energy, agriculture, pharmaceutical products and financial services. This comes after President Trump approved the terms of the phase one trade deal and suspended the additional 15% tariff on Chinese products that were set to go live on Sunday. The US will also cut existing duties on another $120 billion in imports to 7.5%. However, it will leave 25% tariffs on $250 billion in place.

Phase II: Begins

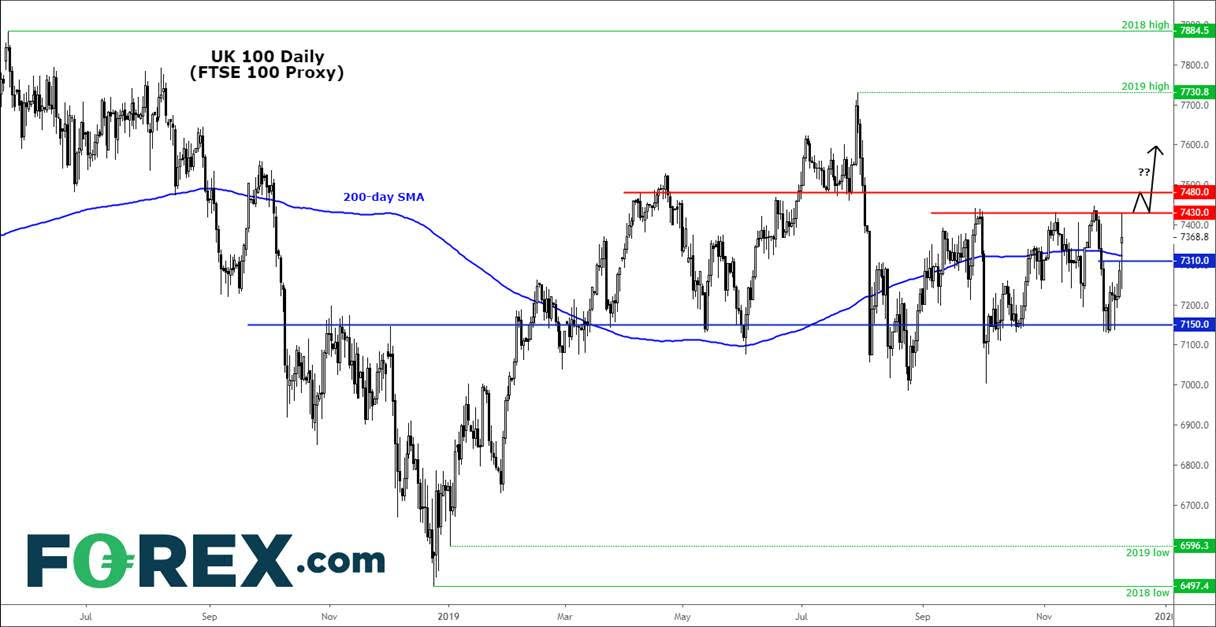

The latest trade development is certainly a big deal for the markets given how important China is to the global economy, not least the Eurozone where shipments to the world’s second largest economy have been hit hard. So, a partial trade deal should alleviate some of the growth concerns. However, it should be noted that the markets have been pricing in such an outcome for a while now. Thus, the move should have been priced in. It will be interesting to see how much further the US markets will rally on the back of this next week. I have a feeling, not very much. But the European markets could play catch-up, not least the FTSE, with Brexit uncertainties receding somewhat (see chart below). The focus will now turn to phase 2 of the deal, which according to Trump will begin immediately. Negotiations for phase two deal will depend on the implementation of phase one deal, says China. This could be another long, back and forth, type of a situation, keeping investors on their toes. The issue of intellectual property theft may prove very difficult to resolve.

So, we are far from seeing the end of the trade war, but it could be the beginning of the end. The same could be said of Brexit. Perhaps it is time for the underperforming FTSE to play catch up with the rest of the world.

Author

Fawad Razaqzada

TradingCandles.com

Experience Fawad is an experienced analyst and economist having been involved in the financial markets since 2010 working for leading global FX, CFD and Spread Betting brokerages, most recently at FOREX.com and City Index.