Week ahead – All eyes on US CPI and trade talks amid no end to tariff uncertainty [Video]

-

US CPI report takes centre stage to gauge tariff impact.

-

Progress in trade negotiations will also be watched, especially with China.

-

US Retail Sales, UK and Japanese GDP on the agenda too.

![Week ahead – All eyes on US CPI and trade talks amid no end to tariff uncertainty [Video]](https://editorial.fxsstatic.com/images/i/cpi-shopping-cart_XtraLarge.png)

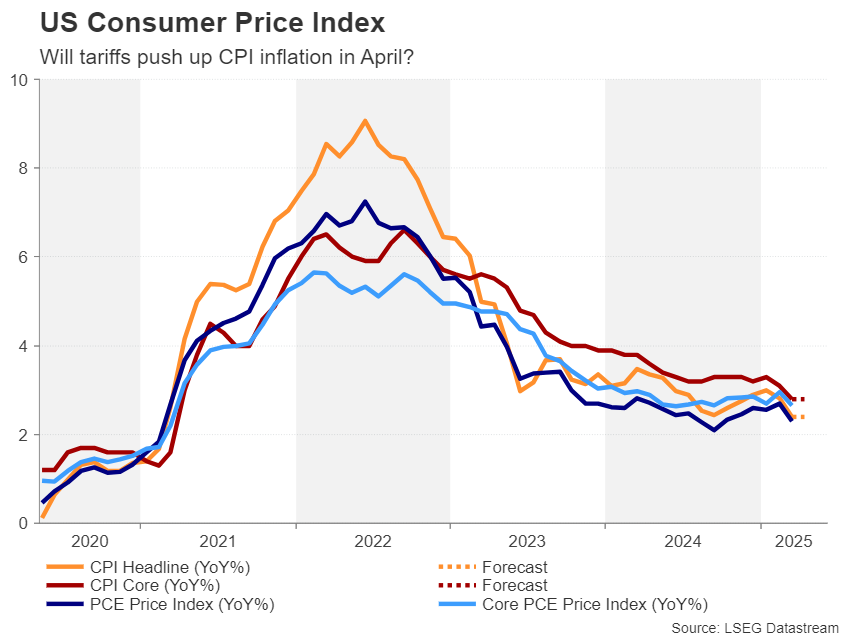

Will reciprocal tariffs show up in April CPI?

Despite lingering worries about a recession, the available data suggests the US economy is at worst, headed for a slowdown. There are no signs yet either that inflation is accelerating, as both the CPI and PCE measures declined in March. However, the cooldown in inflation is likely to be temporary as the broad-based reciprocal tariffs kicked in on April 9. Although the higher levies that were set above the 10% universal rate were delayed for 90 days and some other exemptions were announced too, the price of most imports is expected to have gone up by at least the same amount, with many imports from China facing steeper 145% tariffs.

Yet, it’s expected that very little of those costs were passed on to consumers in April. Many businesses frontloaded their imports before ‘Liberation Day’, while others are likely hoping that most of the tariffs will disappear soon and are holding off from raising prices. But this is contingent on the Trump administration reaching trade deals with its main trading partners within months, something that may not be very realistic.

However, it does mean that the April CPI report won’t be the disaster it could have been. The consumer price index is expected to have increased by 0.3% month-on-month, staying unchanged at 2.4% on a yearly basis. Core CPI is also forecast to have risen by 0.3% over the month and to remain unchanged at 2.8% year-on-year.

The Fed warned of rising risks to both inflation and unemployment at its May policy meeting so any upside surprises to the data on Tuesday could lead investors to further pare back their rate cut expectations for 2025.

US Retail Sales, UoM survey also eyed

But with the Fed also having full employment as part of its dual mandate, rate cut bets are a tradeoff between inflation and what’s happening in the rest of the economy. At the moment, the Fed is being careful about managing inflation expectations, hence, it’s holding firm on its wait-and-see stance. But any sudden deterioration in the economy would prompt it to reconsider this position, as has already been indicated by some Fed officials.

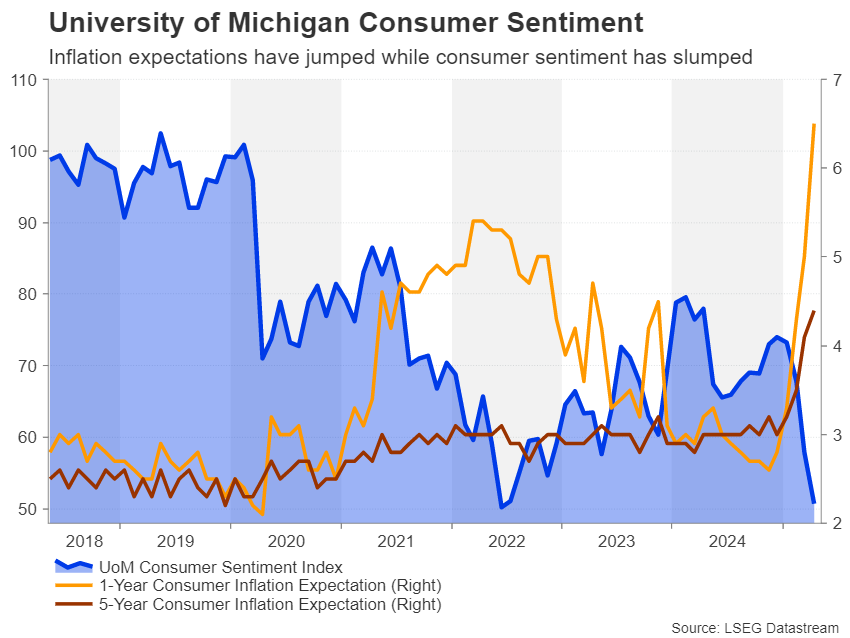

Retail sales is one such dataset that could go in the opposite way of the inflation report. After surging by a revised 1.5% m/m in March, retail sales probably increased by just 0.1% in April. Those figures are out on Thursday alongside producer prices, industrial production and the Philly Fed manufacturing index. There’s a further flurry of releases on Friday, including building permits, housing starts, the Empire State manufacturing index and the University of Michigan’s preliminary consumer sentiment survey.

The latter will be particularly important as the UoM’s inflation expectations metrics have jumped significantly in recent months, likely contributing to the Fed’s caution.

Hopes are high for US-China trade progress

But as investors desperately dissect all the data for clues, it’s possible that tariff-related headlines might have a bigger impact on the markets. US Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer are due to hold talks with senior Chinese officials in Switzerland on Saturday.

This is the first high-level meeting between the two countries since the escalation of trade tensions in February and the stakes are high. Markets are for the moment simply cheering the fact that two sides have agreed to engage in direct talks. But there’s plenty to suggest that Washington and Beijing are quite far apart on their starting points, so any disappointment could bring about a reversal in the positive sentiment, pulling risk assets lower at the start of the trading week.

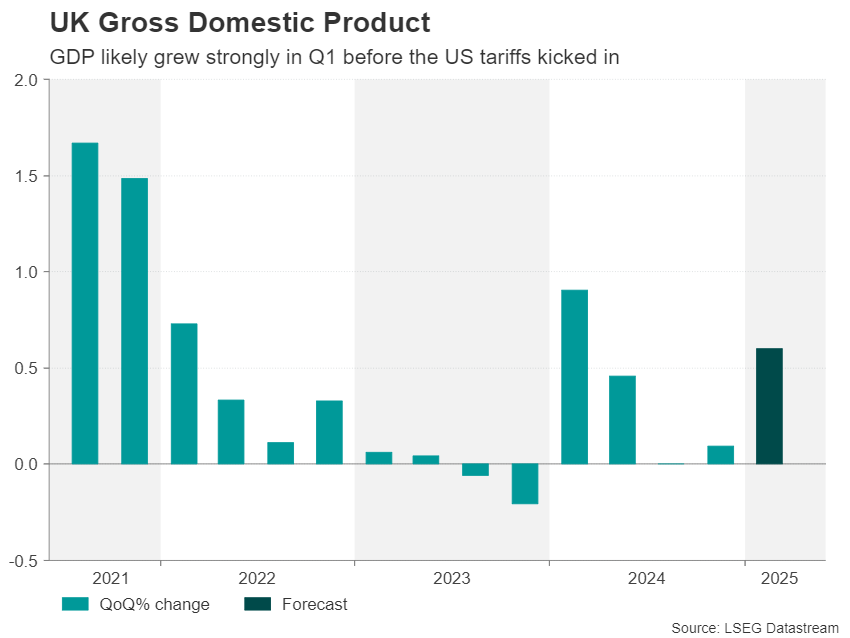

Can UK data propel the Pound higher?

Any potential selloff might be less severe for the pound and UK stocks following the deal reached between the US and Britain on trade that reduces the 25% tariffs on cars and steel to the baseline 10% rate. Whilst it doesn’t appear that the UK has managed to win many concessions in this preliminary agreement, it comes hot on the heels of a deal with India too, as well as improving relations with the European Union.

Subsequently, the pound has established strong support just above the $1.32 level, but at the same time, it’s lacking the momentum to make a convincing break above $1.34. In the absence of a global risk rally, next week’s UK economic releases might not be enough to recharge the bulls.

UK employment numbers for March are out on Tuesday, with the Bank of England keeping a close watch on wage growth, which is proving very sticky. The BoE doesn’t expect inflation to reach its 2% target until 2027 but concerns about growth are keeping it on an easing path. An update on the economy is due on Thursday when first quarter GDP readings are published.

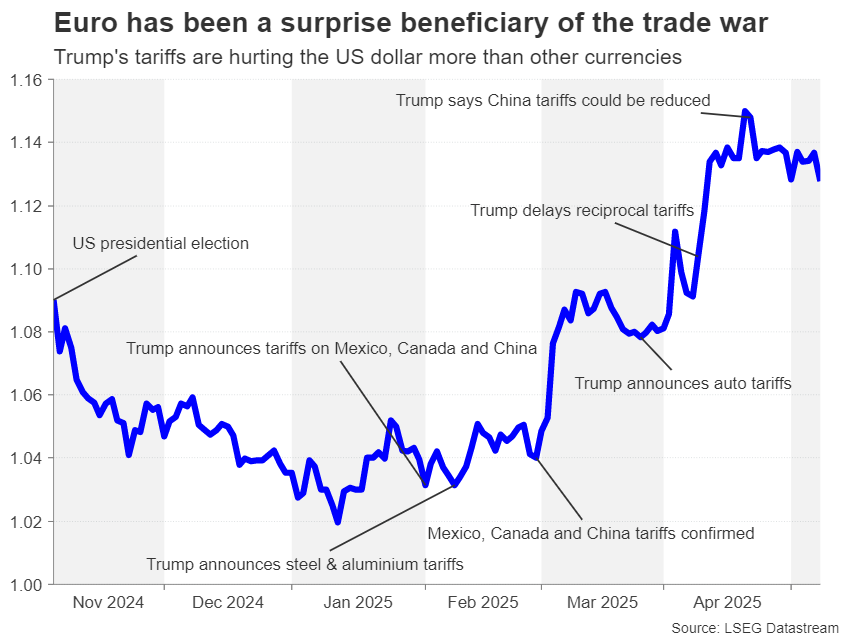

Euro uptrend loses steam as US trade talks drag on

Across the channel, it will be a relatively quiet week for the euro area, with US-EU trade negotiations likely being the main focus for investors. The EU is reportedly mulling higher tariffs on up to 95 billion euros worth of US goods that the bloc could impose should the talks fail. On the other hand, any signs of progress could spur the euro, which has been consolidating its trade war-led gains over the past three weeks.

On the data front, the ZEW economic sentiment index out of Germany might attract some attention on Tuesday, while on Thursday, quarterly employment and the second estimate of Q1 GDP growth for the Eurozone will hit the wires.

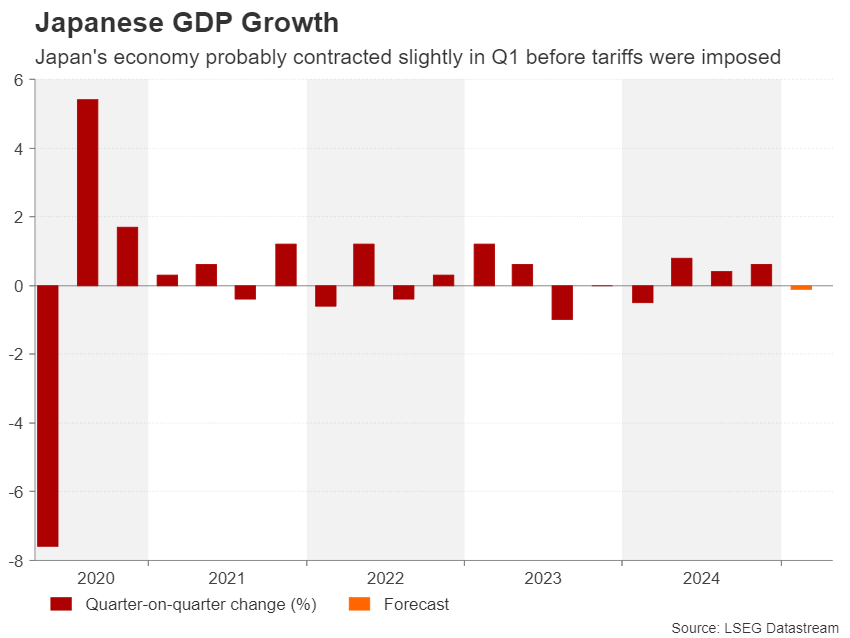

Japanese GDP might dent BoJ rate hike bets

Japan is also eager to reach a new deal on trade with the United States as the fragile economic recovery likely ran into trouble in the first three months of 2025. GDP figures out on Friday are expected to show that the Japanese economy contracted mildly, by 0.1%, in Q1.

The sluggish performance even before Trump’s tariffs have come into effect is one of the reasons why the Bank of Japan has turned less confident about hiking interest rates again. Having said that, policymakers are becoming increasingly concerned about the stickiness in food inflation, which may eventually push up underlying price pressures.

Hence, a rate hike is by no means off the table and any unexpected strength in the economy would increase the likelihood of further tightening later in the year, boosting the yen.

There might also be some hints on rate hike prospects in the BoJ’s Summary of Opinions of the April-May meeting that will be published on Monday. The Summary should shed some light on how strongly board members are sticking to their determination to normalize policy.

Australian employment on tap

Finally, in Australia, the labour market will be in the spotlight, as Q1 wage growth numbers are out on Wednesday, to be followed by the employment report for April on Thursday. Investors have priced in about a 90% probability that the Reserve Bank of Australia will cut rates for only a second time at its policy meeting later in May. It’s hard to see the job figures materially shifting those odds.

Nevertheless, any big surprises could move the Australian dollar, although at the start of the week, the aussie’s focus will be on the developments from the weekend’s US-China trade talks, as well as on China’s CPI and PPI release on Saturday.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl