Warsh calms Wall Street. Korea set to open into a momentum storm

- Warsh eased immediate July hike concerns, but he offered neither easier policy nor a return to forward guidance.

- A 130k payrolls print could look constructive, though World Cup-related hiring may flatter the June headline by roughly 40k jobs.

- Meta’s apparent capex discipline is bullish for Meta, but it raises difficult questions about the durability of AI compute, memory and neocloud demand.

- Korea is set to absorb the sharpest edge of the unwind, where memory exposure, leverage and retail positioning can turn a rotation into a momentum storm.

Korea set to open into a momentum storm

Wall Street took Kevin Warsh’s Sintra remarks as enough permission to keep buying, at least in the broadest sense of the word. Growth still looks firm, oil has fallen back toward pre-war levels, manufacturing is holding up, and the Fed Chair gave investors little reason to start pricing an immediate July hike. With pension-reset flows beginning to stir at the turn of the quarter, that was enough to put a bid under cyclicals and lift most of the S&P 500, even as the index itself spent much of the day wavering around the flat line.

It was the kind of session where the closing level did not tell the whole story. On the surface, Wall Street was calmer. Underneath it, the market’s most crowded trade was beginning to look as though someone had quietly removed a few bolts from the floor.

Warsh did not give the market a dovish pivot, and he certainly did not offer a map toward easier policy. What he did offer was a little more confidence that inflation is no longer travelling in only one direction. “Expectations of inflation over the first four weeks of this period have come down, inflation risks have come down,” Warsh said Wednesday at the European Central Bank’s annual Forum on Central Banking in Sintra, Portugal.

That was enough to take some of the immediate heat out of the rate-hike conversation. He repeated that price stability remains the Fed’s job, but he also repeated that he is not going to provide forward guidance on where policy goes next. Markets can make their own judgments meeting by meeting, just as the Fed intends to do. The two-year yield eased, and the broad read was straightforward enough: there is no immediate case for a July hike, but nobody should confuse that with an invitation to start pricing a clean path toward cuts.

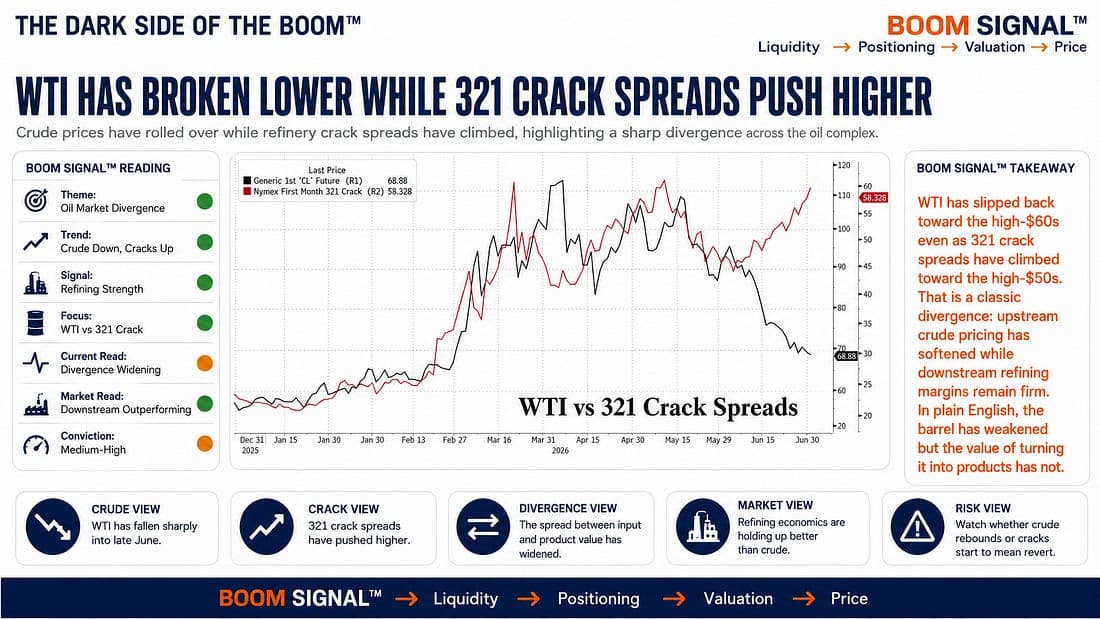

The data gave him room to hold that line. Manufacturing expanded for a sixth straight month, while the ISM prices-paid index recorded its largest one-month drop since July 2022 as the oil shock continued to unwind. With indirect US-Iran talks described as positive and crude sliding back toward its pre-war range, the input-cost picture is looking less threatening than it did only a few weeks ago. The oil market may have stopped panicking faster than the gasoline market has adjusted, with crack spreads still telling a rather different story, but for the Fed the direction of travel matters more than the refinery margins.

The striking divergence between crude oil prices and crack spreads is the refining margins that ultimately help set the price consumers pay at the gasoline pump.

The next important test is payrolls, with consensus expecting 115k jobs in June. I see a risk that the number comes in closer to 130k, which would be above consensus but still below the previous three-month average of 188k. On the surface, that would be a market-friendly result. The labour market would still be expanding, unemployment would remain contained, and the Fed would have little reason to either tighten policy in a hurry or start preparing the ground for easier policy and maybe even a Warsh Goldilocks zone.

The caveat is that this may not be one of those payrolls reports where the headline tells the whole story. A meaningful share of the upside could come from the World Cup, with host-city employment data pointing to stronger hiring between the May and June survey periods in leisure and hospitality, business services, and trade and transportation. The tournament could add roughly 40k jobs to the June number, which is enough to make the headline look healthier without necessarily changing the underlying weather.

A World Cup fills hotels, restaurants, airports, transport hubs and temporary staffing rosters. It puts more people on the clock and more cash registers to work, but that is not quite the same thing as a broad-based acceleration in labour demand. A 130k payrolls number would probably keep the market comfortable, but investors should be careful about treating it as proof that the economy has suddenly found a new gear.

That was the macro setup heading into the day: steady growth, fading price pressure, a Fed that can afford to sit still, and a jobs number that may look a little better than it feels. It should have made for a relatively boring start to July.

Then Meta happened.

Reports that Meta is looking to sell excess compute capacity through a cloud business, while stepping back from the ambition of building the leading frontier model, hit the market like a small sentence with very large implications. Meta surged around 10% as investors welcomed the prospect of greater financial discipline, stabilising free cash flow and a possible revenue stream from data-centre assets that had previously been treated as an expensive act of faith.

The market had always been likely to reward the first hyperscaler willing to hint that the capex race might not be endless. One company’s discipline, however, is another company’s demand destruction.

The phrase that did the damage was “excess capacity.” Once that word appeared, the market no longer had to debate whether Meta’s decision was good for Meta. It had to start asking whether one of the largest buyers of compute was effectively telling investors that the AI buildout may not be as supply-starved as everyone had assumed.

For the last year, the AI trade has worked like a very tidy machine. Hyperscalers spent aggressively, chipmakers and memory producers supplied the machinery, and every new capex estimate gave the whole chain another excuse to trade higher. The spending companies and the suppliers were both rewarded, as though the market had found a perpetual-motion device powered by data centres.

Yesterday, that machine started to cough.

Meta rallied while semis, memory names, and neocloud plays were taken to the wood chipper. High-beta momentum baskets, now loaded with chip and memory exposure after their extraordinary first-half run, suffered one of their worst sessions in years. One major high-beta momentum basket fell around 9%, while the long-short version was down roughly 10%, putting it on pace for its ugliest day since the vaccine shock in 2020.

The winners and losers had suddenly started moving in the wrong direction at the same time, which is usually when traders realise they are no longer dealing with a normal sector rotation. This was a repricing of duration. The market is beginning to ask whether capex growth peaks before earnings estimates have had time to catch up with the optimism already embedded in the chip complex.

Micron has become one of the cleaner fault lines. It has not closed below its 20-day moving average near 1049 since early April, a remarkable stretch for a stock with this much volatility. If it loses that level, the next obvious area sits closer to the 50-day moving average around 842, roughly 20% lower. Reports that Apple may be exploring alternative memory-chip supply channels have not exactly helped the mood, but the larger issue is whether investors are still willing to pay for a memory cycle built on the assumption that demand remains hotter for longer while some of the largest buyers of compute begin talking about unused capacity.

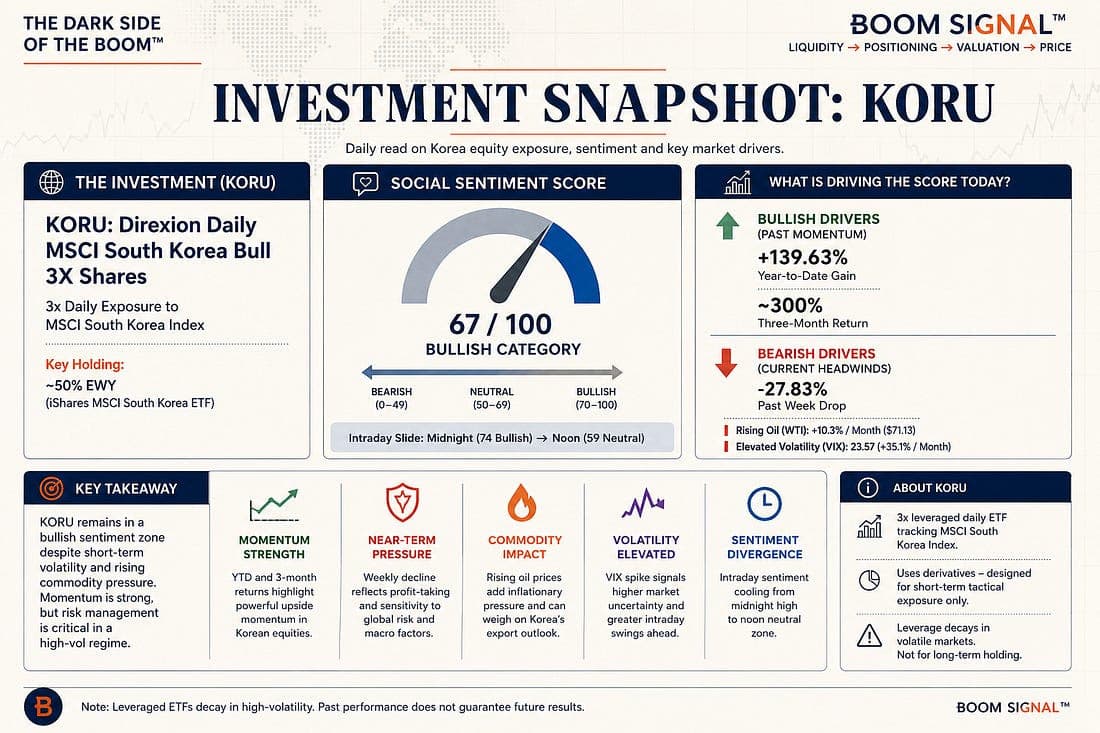

That is why Korea matters so much this morning.

Korea sits directly in the blast radius of the memory unwind. It has heavyweight semiconductor exposure, deep retail participation, sizeable leveraged-product flows and a familiar ability to turn a global growth theme into a domestic trading carnival. When the story is rising, the carnival is glorious. The rides are fast, the crowd gets louder, and nobody is particularly interested in asking whether the ground beneath the tent is softening.

When the story turns, the hyper-leveraged exits narrow very quickly.

KORU's 23% fall is not just another ugly number on the screen. It is a warning that leverage once again collides with a narrative reversal, and that rarely ends gently. The question heading into Seoul today is not whether the market feels the move, but how much of the opening must be processed through forced de-risking, volatility circuit breakers, and traders realizing that a crowded trade does not need a terrible earnings print to unravel.

It only needs the story to stop getting better.

Meta may simply be exercising sensible financial discipline. In another market, that would be a company-specific development and little more. But crowded markets do not trade nuance when the first crack appears. They trade the second-order implication. If Meta is easing off the capex accelerator, who follows? If excess capacity is beginning to show up, how much of the memory shortage was structural and how much was a temporary scramble? And if investors have already capitalised several years of extraordinary AI demand into chip valuations, what happens when the duration of that demand begins to shorten?

There are beneficiaries on the other side of the move. Software rallied as investors looked for parts of the AI ecosystem that benefit when frontier-model spending becomes less of a bottomless well. Bitcoin also caught a bid, bouncing from longer-term support as some of the momentum capital that had been camped in memory and chip names began looking for another home. Elsewhere, money is already searching for the next bottleneck trade, with components such as capacitors suddenly attracting attention.

That is how these rotations work. The money does not vanish. It leaves the crowded room, walks down the corridor and starts trying other doors.

Still, the immediate backdrop is not especially friendly for high-beta momentum. Seasonal work suggests July has been a difficult month for the trade in recent years, often because the short leg begins to rally rather than because the longs collapse on their own. That matters because this was not merely a weak day for semis. It was a violent repricing of the factor that has done much of the heavy lifting for equity leadership this year.

Warsh may have calmed Wall Street with a message of easing inflation risk, resilient growth and no immediate need to tighten policy further. Meta, meanwhile, has handed Korea a much more immediate problem: a momentum carnival where the music is still playing, but more traders are beginning to notice that the floor is not as solid as it looked.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.