Vigilance and Cool Heads Ought Prevail? - the U.S. Election and Diversity

The imminent U.S. election has sparked significant debate, social, political and economic. It seems like a long time ago that Trump was seen as an impossible candidate and that Sanders was threatening Clinton's ascendancy. Recently, however, this ascendancy seemed to be under real threat from the impossible candidate, and the markets seemed a little spooked. This article is intended to provide a brief overview of the situation and to consider the question of diversification. Should you diversify your portfolio ahead of the U.S. election, and if so how?

"We intend to immediately renegotiate the terms of that (NAFTA) [...] If they don't agree to a renegotiation, we will submit notice" - Donald Trump

Trump, as a billionaire business owner, his many failings aside, ought to be a solid pro-business candidate, but his rhetoric on trade, migration, and intervention is hardly inspiring for an investor who wants the global world to remain firmly open for business.

With Clinton, while she has back-pedalled on her strong globalism to a degree, this seems an election maneuver, and it's much easier to believe that after a Clinton win, you know what you're going to get.

"We have to trade with the rest of the world. We are 5 percent of the world's population. We have to trade with the other 95 percent. And trade has to be reciprocal. That's the way the global economy works" - Hillary Clinton

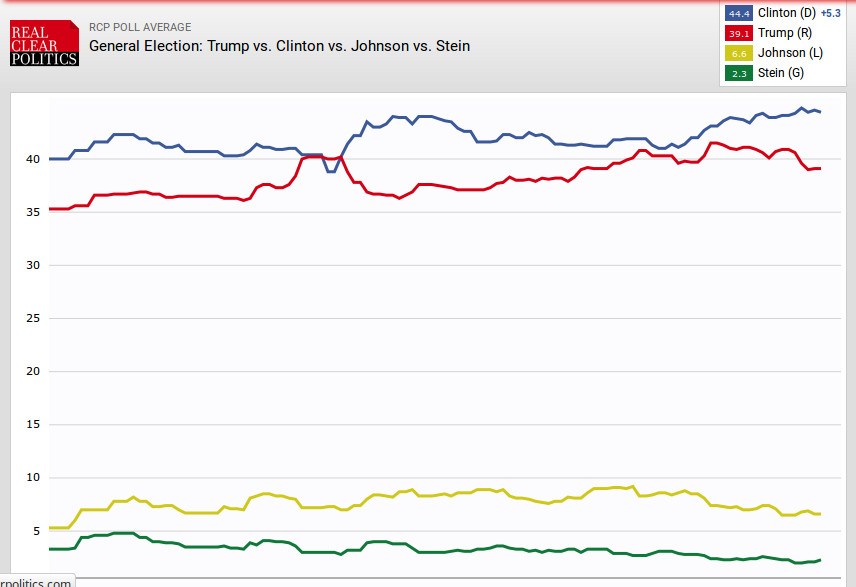

This is not written to prejudice anyone's election stance, though I should make the disclaimer that I am no supporter of the Republican candidate, but in a binary choice and from a business perspective, the steady hand on the tiller is usually the preferred one. The reality, however, is that in the current global climate, many voters seem less interested in stability than they are in expressing their anger, their feeling of disenfranchisement, and their desire for radical change. As a result of this, Clinton's lead of 5.3 points, while substantial, does not make her a dead-cert, even after recent revelations. This volatility, even in the face of what is still a likely Clinton win, brings with it questions about how to manage your assets.

The key question with regard to diversifying your portfolio in line with an election is exposure. What assets do you hold that are at risk depending on the outcome? If, for instance, you have unhedged currency holdings in Mexican Pesos or Russian Rubles, currencies which are acting as indicators for the fortune's of the two U.S. contenders, or holdings in the countries respective stock exchanges, hedging your risk might seem a good option. This does not, however, mean that diversification of your assets beyond their current level is absolutely necessary.

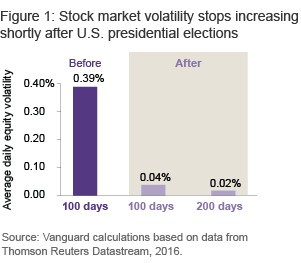

Vanguard Investment Strategy Group suggests 'that presidential elections typically don't have a long-term effect on market performance', noting that 'volatility typically stops increasing shortly after Election Day once the markets have had a chance to digest the news.' Yet, if you've been taking risks on a particular position and thereby increasing your potential exposure, in the run-up to the election it might be advisable to pull back from some of these more speculative positions, however a strong and stable portfolio ought to be sufficiently diverse to weather all but the most unexpected election news.

While it is true that Wall Street isn't keen on a Trump win, and it is also true that at the moment a Clinton White House seems in prospect, the danger during election season is to overvalue election-related issues at the expense of other potential market triggers such as rate rises. Even so, in the run-up to this U.S. vote, if you are worried about the effect of your holdings there are some things you might consider.

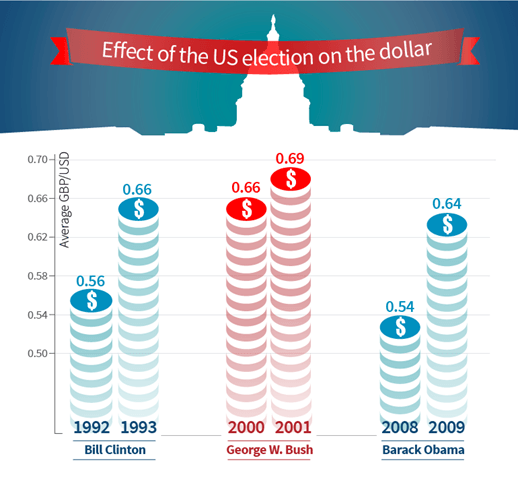

Should you have a strong position in U.S. dollars, or be interested in investing prior to the election, it is worth noting that after the majority of U.S. elections, once the period of uncertainty ends, the dollar typically rises as volatility abates. While there are risks from a Trump presidency, in particular his aforementioned trade stance, the short-term post-election outlook for the dollar, historically at least, would seem likely to be of at least marginal gains. With the U.S. dollar the reserve currency, although volatility can be expected over the short-term, cool heads ought perhaps to prevail.

There is also the question of the relationship between the bond market and the equity market. Diversifying your assets into bonds is by no means a poor choice, however as Michael Lebowitz of Seetitmarkets argues, in an economic climate $13tn bonds have negative yields, in the event of trouble in the aforementioned equity market a correlative rise in bond prices and a fall in yields is not necessarily certain, given the scope for price rises as against the opposite.

As far as U.S. stocks are concerned, again the most reasonable course of action is to do your research. If you've got a high level of exposure to health-care, bio-tech, or energy production, it might be a good idea to move some of your money toward growing asset classes less likely to be influenced in the short term by whoever the new occupant of the White House may be, with exposure to Lithium, or technology stocks for instance, a good long-term bet, also as Lebowitz suggests, the VIX may be 'a prudent place to own protection'. Regarding equities which are unlikely to be directly impacted by the first hundred day policies of the President to be, and with October being a traditionally volatile month, there might be the temptation to ascribe more weight to external factors than is correct. A vigilant wait-and-see approach may just be the sanest course of action.

As for positions to take aside from any potential diversification, there is some suggestion of potential Bearish movements in the market, suggesting the possibility of a sell-off, with HSBC analysis suggesting that 'if the S&P 500 closes between 2,116-1,991 and if the Dow industrials breach the 17,992-17,063 level' there is risk of break in support levels triggering a larger scale drop in share prices. This could be potential good news however for an investor minded to take a risk. A pre-election share price correction, should the markets be happy with the outcome of the election, presents the possibility of profiting from a post-election share price rise. After an election, the average market climb is 8.2 percent, as per S&P. So, even in the event of an imminent downturn, as per Citi's Tom Fitzpatrick, the historically likely post-election bump appears to present opportunities to profit.

Author

Oisin Breen

Accendo Markets