USD supported ahead of FOMC, but will a hike suffice?

There’s plenty of event risk for traders to consider this week, although volatility has largely remained contained as we wait for the big events to hit our screens. The highlight is arguably tomorrow’s FOMC meeting, but we also have BOE and ECB meetings on Thursday along with all-important CPI reads for UK and US to consider (among others). So whilst these potentially high volatility events have limited our watchlist in some ways, when volatility returns it could open new opportunities.

Tomorrow marks Yellen’s last press-conference FOMC meeting before handing over the reins to Jeremy Powell in February, where there’s a widespread belief the FED will raise rates to mark the fifth hike as part of this cycle. Yet as markets are forward looking, the anticipated hike is more than likely priced into the Greenback which leaves it vulnerable to a sell-off if anything less than a hawkish meeting materialises. So bullish USD setups require the Fed to exceed expectations, whether it be via economic forecasts, statement, press conference or the Dot plot.

Markets are currently pricing in at an 87.6% chance of a hike on Wednesday and a 59% chance of another hike in March, according to the CME FedWatch tool. Whilst the accuracy of these numbers at times are debatable, they can provide a proxy for how the markets and sentiment may be positioned ahead such events. And as expectations require fulfilling, anything less can result in market volatility or new trends if the reality is too far from consensus.

Will Yellen go out with a bang?

Being Yellen’s last press conference, she has little to gain by rocking the boat especially when the makeup of the Fed is going to look very different next year. Therefor its unlikely Yellen will diverge too much from the usual script of ‘transitory inflation’ and for the economy to continue to pick up gradually. However, it’s also debatable as to how hawkish the Fed would want to appear with the threat of tax reforms and underwhelming inflation lingering in the background. So, whilst the USD Index remains supported below last week’s highs, there’s room for disappointment for Greenback bulls if a business as usual meeting is to materialise.

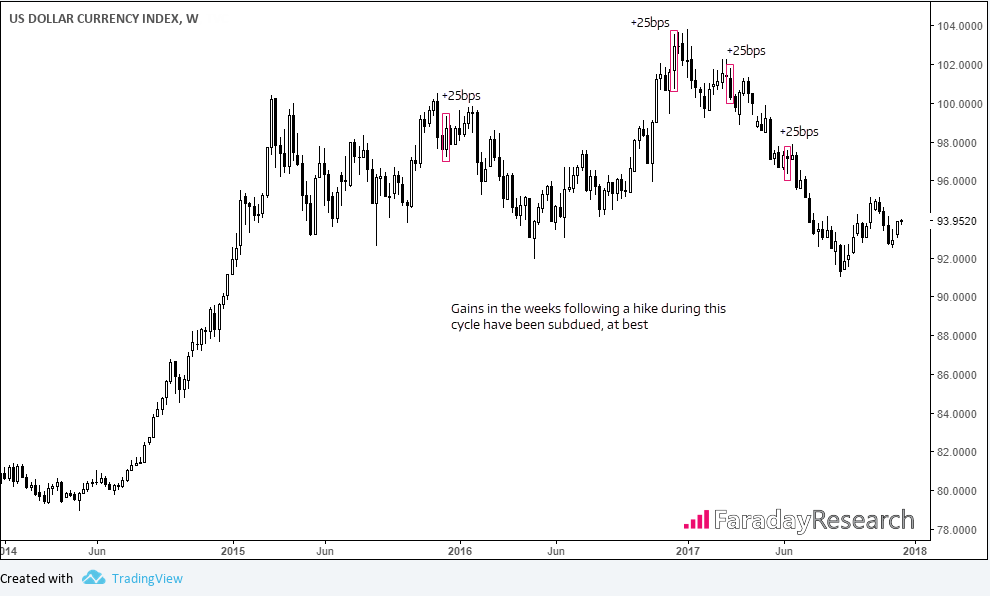

If we look at how the US Dollar Index responded in the weeks and month’s following the prior four hikes, we can largely agree it’s not been great for the bull-camp. In fact, the most notable bullish reaction following the Dec 2015 hike came when Trump was elected and promised to make “heads spin” with tax cuts and promise all will be “tired of winning”. So, traders likely need to feel a March hike is on the cards and there are no causes for concern to provoke a notable bullish reaction on the day. Although it’s more than likely tax reforms which would prove to be the catalyst to help it sustain a rally further out though.

Until the event happens, it’s difficult to say how this could play out with so many moving parts. And due to the potential complexity surrounding the FOMC release, USD crosses are on the back-burner until the event has passes.

Author

Matt Simpson, CFTe, MSTA

CityIndex

Matt Simpson is a certified technical analyst who combines charts and fundamentals to generate trading themes.