USD/JPY Weekly Forecast: The fallacy of devaluation or the BoJ is out of ideas

- USD/JPY jumps to two-decade high as the BoJ doubles down on accomodation.

- Monetary policy divergence between Fed and BoJ intensifies.

- Negative first quarter US GDP belied by strong consumption.

Years of failure have not deterred the Bank of Japan from continuing the endless monetary accommodation that has not revived the economy or ended deflation. The Japanese yen dropped to a two decade low on Thursday as the central bank pledged to defend its zero rate policy with unlimited government bond purchases, falling further out of step with its central bank colleagues around the world.

-637868389999793141.png)

Since the first of the year the yield on the 10-year Japanese Government Bond (JGB) has increased 15 basis points from 0.072% on December 31 to 0.218% at Friday's Tokyo close. By comparison, the US 10-year Treasury yield has added 143 points from 1.436% at year end to 2.863% at Thursday’s close. In the same period the USD/JPY has climbed 12.9% from 115.10 to 130.05 in early Friday trading.

The most intense rise in USD/JPY from the March 4 close at 114.81 to 130.05 coincides with a widening of the 10-year spread from 158 basis points (3/4/22 close: US 10-1.721%, JGB-0.143%) to 265 points (4/28/22 close: US 10-2.863%, JGB-0.218%). No other explanation is needed for this historic collapse of the Japanese yen.

-637868390608608670.png)

Japan’s base rate has been at -0.1% for more than seven years. National annual CPI has reached 1.5% twice in that time and has averaged less than 1%, frequently dipping to outright deflation. The increase in yearly prices from -1.1% last April to 1.2% in March has little to do with BoJ policy and everything to do with the pandemic onset and response.

The BoJ’s long-term goals of stable inflation at 2% and stimulating the economy by keeping the 10-year JGB yield around 0%, with an implicit 0.25% rate cap defended by unlimited bond purchases, have been failures, but the governors have elected to double down rather than see reality.

Though the policymakers are not about to admit it, the collapsing yen, which makes imports more expensive, is probably seen as an ally in the bank’s deflation fight. Bank officials have made their traditional complaints about the speed of the currency moves but intervention is most unlikely.

First, BoJ intervention cannot work. The global currency market is far too large for one central bank, no matter how determined, and the BoJ is the picture of policy diffidence, to have any more than passing impact. If the BoJ decided to buy the yen it would only be guaranteeing profits to the traders on the other side of its deals. Second, while a weaker yen will do nothing to help Japan’s long term demographic and structural problems, the real source of the economy’s malaise, it will somewhat counter deflation and boost exports, which the bank can point to as successes.

The BoJ’s latest assertion of policy futility will not bring inflation to its 2% target, though global price increases might, at least for a time, and it will not create an economic revival. Zero rate obstinance will however, keep the pressure on the yen which is headed to further losses as the US-Japan yield spread continues to widen.

Industrial production in Japan fell 1.7% on the year in March and rose 0.3% for the month, respectively much weaker than the 0.5% and 2% April results. Retail Trade (sales) were better than forecast in March but evinced no trend.

The BoJ maintained its base rate at -0.1% and promised to defend its yield-curve-control policy with unlimited purchases of 10-year JGBs.

In the US, Durable Goods Orders in March were better than expected and Initial Jobless Claims remained at near historic lows. The initial shock of -1.4% GDP in the first quarter, far below its 1.1% forecast, had almost no negative market impact. A widening trade deficit and lower inventory restocking by businesses subtracted about 4% from the GDP accounting while consumer spending remained healthy at 2.7%, promising a better performance in the second quarter.

Personal Consumption Expenditure prices rose to 6.6% in March, slightly more than predicted but core PCE prices were 5.2%, a bit less than forecast. Personal Income and Spending were marginally stronger than anticipated in March and revised upward for February giving credence to the idea that however unhappy consumers say they are in sentiment surveys, they are not about to stop spending.

The obstinacy of the BoJ in the face of reality and the constancy of the US consumer facing inflation are the twin themes of the week.

USD/JPY outlook

Rarely has currency direction been more directly and obviously determined than the USD/JPY rise has been by the yield-curve-control policy of the Bank of Japan. Until the end-point of Fed rate increase is better understood the bias in USD/JPY must be higher.

Treasury futures predict the fed funds at 2.75% or higher by the end of the year. How soon that is achieved is undetermined and not known to the Fed governors themselves. A 0.5% hike next week is assured but whether that continues in June depends on the rate of inflation and the disposition of the US consumer. Thus far Americans have, despite all, continued to show confidence in the future. Domestic consumption has remained strong.

The Federal Open Market Committee (FOMC) is also expected to start a passive reduction of its $9 trillion balance sheet. If that does not take place, or the governors elect an active role, selling from the bank's portfolio rather than letting bonds roll-off at maturity, markets will respond by selling or buying the dollar. Nonfarm Payrolls for April are not expected to provide any fireworks with results in line with the past several months.

The area above 130.00 provides little guidance as references from trading activity two decades distant is pure conjecture. Traders should be aware that clear technical signposts will take some time to build and volatility chasing profits is likely to be more common than usual.

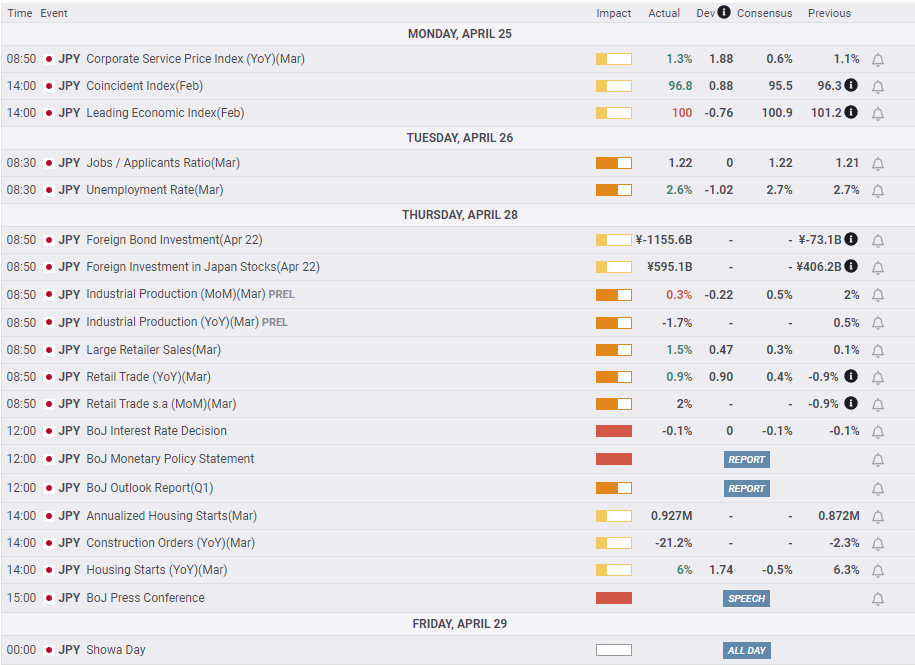

Japan statistics April 25–April 29

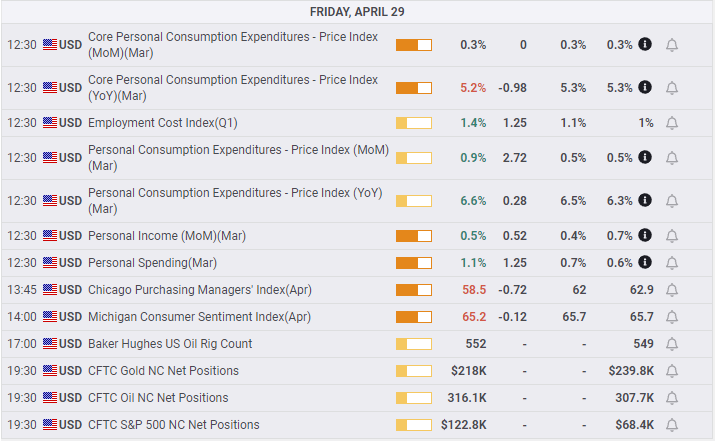

US statistics April 25–April 29

FXStreet

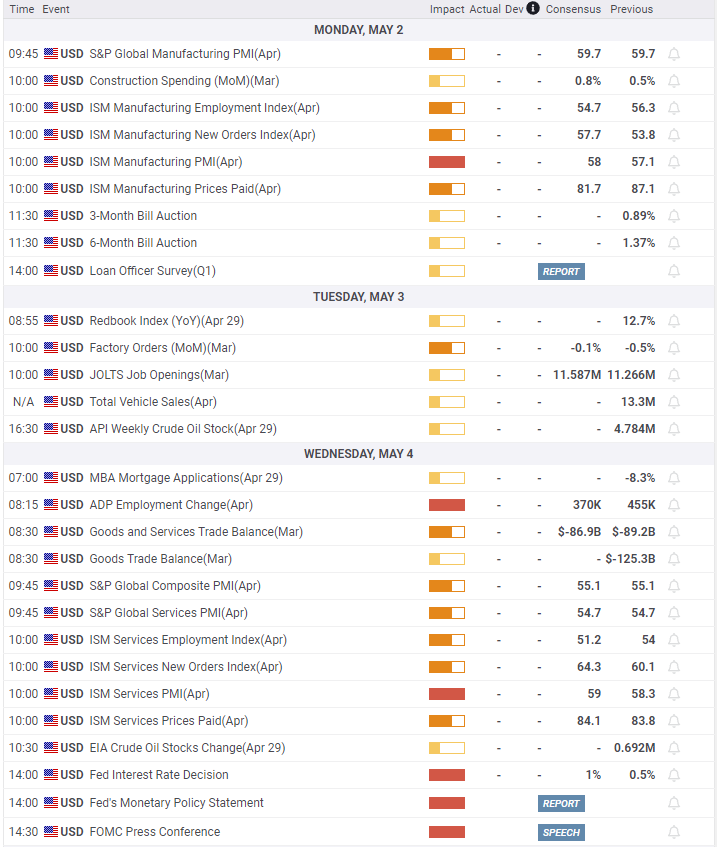

Japan statistics May 2–May 6

FXStreet

US statistics May 2–May 6

FXStreet

USD/JPY technical outlook

The technical layout is dominated by the dollar to a degree that is rare in analysis. The basis of the dollar's ascendancy is fundamental but the expression is technical. The MACD (Moving Average Convergence Divergence) has been above 2 continuously for almost two weeks. There are few examples of such dominance in the last 30 years. The Relative Strength Index (RSI) has been overbought for even longer. The natural mean reversion implied by these readings is unlikely to take place until permitted by a fundamental catalyst. The FOMC Wednesday meeting is one possibility. If the Fed opts for a 0.25% increase rather than 0.5%, or delays the start of balance sheet reduction the chance of a USD/JPY reaction is high. The Average True Range (ATR) level depicts the high level of volatility expected with the highest range in twenty years.

tech 1-637868416138531505.png)

The hourly chart shows the beginning of support at 130.40, 130.00 and 129.70. That these levels did not hold at first blush does not mean they will not be revisited in the future, building strength and importance with each occasion.

tech 2-637868419350292276.png)

Resistance: 131.00, 131.25, 131.50, 132.00

Support: 120.70, 129.00, 128.45, 127.70

Moving Averages: 21 day-126.41, 50 day-121.50, 100 day-118.15, 200 day-114.98

tech 4-637868424510051650.png)

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.