USD/CAD Forecast: Welcome to the statistical derby

- Dovish Bank of Canada rate statement weakens currency.

- Economy slows on in the second half more than expected.

- Outlook turns doubtful on domestic and global concerns.

- USD/CAD will turn on economic performance.

The Bank of Canada kept its base rate steady at 1.75% on Wednesday in a move that had been widely anticipated. But its assessment of the economy and a change in the wording of the accompanying statement seemed to open the way for an accommodative policy in the future and gave the Dollar Canada its only movement of the week.

“Data for Canada indicate that growth in the near term will be weaker, and the output gap wider, than the Bank projected in October…Some of the slowdown in growth in late 2019 was related to special factors that include strikes, poor weather, and inventory adjustments. The weaker data could also signal that global economic conditions have been affecting Canada’s economy to a greater extent than was predicted,” said the statement.

The bank also dropped an assertion that the current rate was appropriate that had been current since April.

Currency markets took the economic uncertainty of the bank immediately to the Canadian dollar. The USD/CAD rose almost a figure to a high of 1.3141 immediately after the announcement.

Prior to the 10:00 am EST rate announcement the loonie had reached 1.3036 against its American colleague but some of those gains had been shed after core CPI for December and wholesales sales for November at 8:30 am EST came in softer than forecast.

Probably the key factor in the BOC’s changing judgement on the economy has been the decline in job creation. In the first half Canadian firms hired an average of 41,250 new workers per month, from July to December that average dropped to 12,250.

Wednesday’s rush higher in the USD/CAD divided a week whose halves had the same limited volatility albeit a figure apart. Monday and Tuesday averaged 34 points around 1.3060 and Thursday and Friday averaged 25 points around 1.3150.

While the BOC highlighted the weakness in the Canadian economy the governors are, like their Federal Reserve counterparts, awaiting the effects of the US-China trade agreement. The completion of the deal has long been priced into the markets but the initial results will take until the end of the first quarter to become apparent.

In the interim the Canadian dollar will be at a slight disadvantage against the US as the BOC is newer to the worry game and the Fed is firmly in neutral. Every weak Canadian statistic will lead to speculation that the BOC’s next move will be a rate cut.

Canadian and US statistics this week, January 20-24

The BOC concerns were borne out in the few releases this week.

Manufacturing sales for November on Tuesday at -0.6% were twice as weak as forecast. Though the prior month was revised higher to -0.2% from -0.7% that is the third month in a row that sales have fallen and the fifth negative in the last six month.

Wholesale sales in November, mentioned above, were also much poorer than anticipated at -1.2% and the October figure was revised to -1.2% from -1.1%. Sales have fallen in three of the last four months.

Core inflation in December was 1.7% year over year, lower than the 1.9% prediction and the November’s result. The pace of price gains has fallen from 2.1% in May. On the month prices dropped 0.4%, double the estimate. Headline CPI was 2.2% as expected and unchanged from November. Prices on the month were flat missing the 0.1% prediction but up from the 0.1% loss in November.

Retail sales for November on Friday were a mixed bag. Overall sales were more than twice the 0.4% forecast at 0.9% and the October score was revised to -1.1% from -1.2%. But the ex-autos result, a more general reading on the consumer, came in at 0.2% half its consensus prediction and November was adjusted to -0.4% from -0.5%.

In the US housing continued its strong recent showing as annualized existing home sales, about 90% of the market, climbed to 5.54 million units, its best rate since March 2018. Initial jobless claims registered 211,000 in the January 17 week bringing the four-week moving average down to 213,250 which remains near its five decade lows.

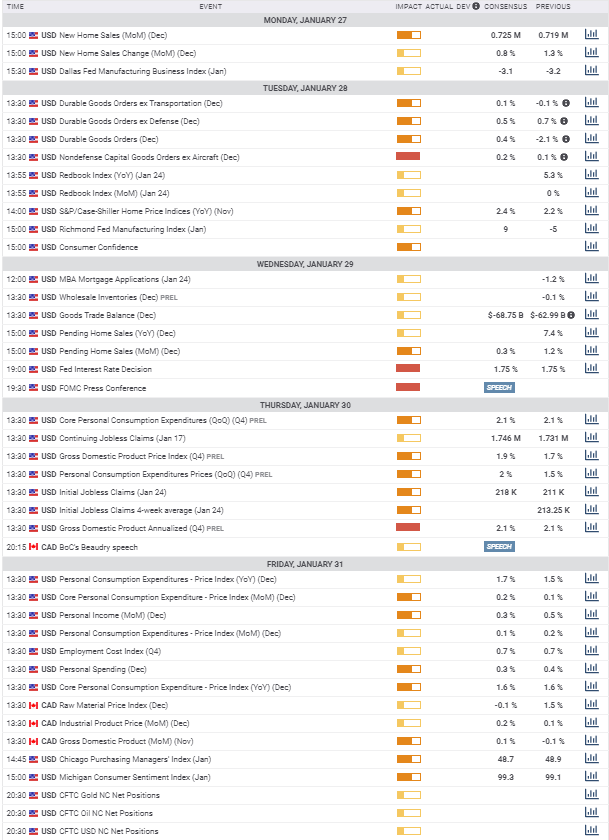

Canadian and US statistics next week, January 27-31

It is a very thin week in Canada. On Friday are price indexes for raw materials and industrial products in December with -0.1% and 0.2% expected, both are second level statistics with no market impact. Gross domestic product for November is expected to have expanded 0.1% following Octobers 0.1% decline. In consideration of the BOC’s concerns this may receive more attention than usual.

The US, in contrast, has a busy week. Monday brings new home sales for December with 725,000 annually forecast up from 719,000 in November. Purchases have risen from their low of 604,000 last May and reflect the strength of the housing market overall. New home construction provides most of the employment in the sector.

On Tuesday durable goods orders for December are out with a 0.4% gain expected after November’s 2.1% decrease that was largely due to a sharp drop in Defense Department procurement. A 0.5% gain is predicted in the ex-Defense category following November’s 0.7% increase.

The non-defense capital goods orders ex-aircraft group, a well know proxy for business spending, is expected to rise 0.2% in December after November’s 0.1% increase. Improvement here will likely be taken as an indication that business investment is set to return.

All three categories will be monitored for early signs that the China trade agreement has stirred the economy.

Wednesday provides wholesale inventories for December. A build here after the November drop of 0.1% would suggest businesses anticipate improving sales in the months ahead.

The Federal Reserve rate decision passes at 2:00 pm EST on Wednesday. As no change in the fed funds is anticipated market interest will focus on Chairman’s Powell’s press conference and his characterization of the US economy.

Gross domestic product will be the focus Thursday with the preliminary estimate for the fourth quarter expected to be 2.1%.

Inflation returns on Friday for the personal consumption expenditures price indexes (PCE) from the Bureau of Economic Analysis, a division of the Commerce Department. Core prices are forecast to increase 0.2% on the month in December and 1.6% on the year. As the core PCE index is the Federal Reserve’s preferred inflation measure it has a higher market impact than the older CPI. Overall price gains will be 0.1% and 1.7%.

Personal income and spending for December are also issued with 0.3% expected for each. Income is a wider gauge of household revenue than average hourly earnings as it includes a number of transfer payments.

The Michigan Consumer Sentiment final figure for January is released at 10:00 EST, a slight gain to 99.3 from 99.1 is anticipated.

Statistics conclusion

Neither the Bank of Canada nor the Federal Reserve are in an active phase. Officials from both institutions are waiting for economic developments. For the next several months direction in the USD/CAD will be determined, barring unexpected events, by the relative performance of the two economies.

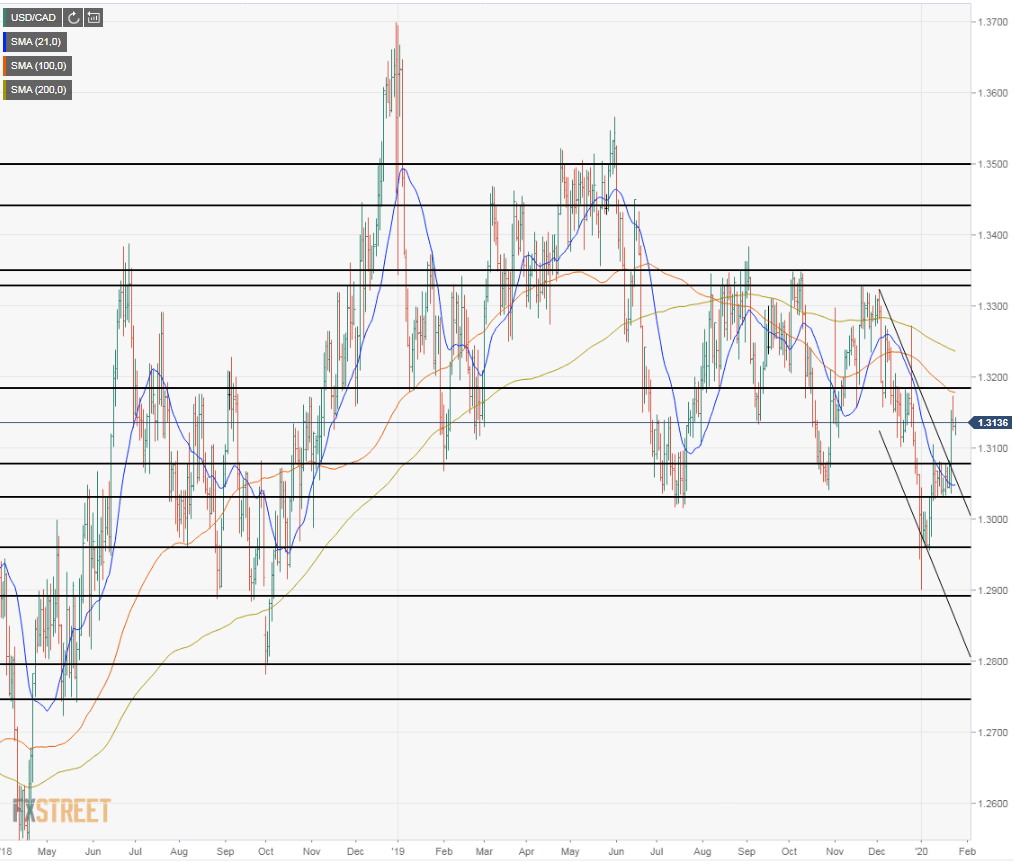

USD/CAD technical outlook

Wednesday's bold move did little to change the technical picture.

The 21, 100 and 20 day moving averages remain downcast slightly modified by the Wednesday run higher. That move conclusively broke the upper limit of the two month old down channel and will likely render it moot.

First supports are at 1.3080 and 1.3029 the upper and lower limits of price movement in the middle two weeks of January. That action having superseded the July and October trading through the same levels. Much weaker support is at 1.2960 the bottom in the first week of the year. Beneath that we return to October 2018 for the next limit at 1.2800 for a limit that is more a marker than real support as it was touched by just three days in early October. Following that is the long range line at 1.2750 from May 2018.

The first resistance above is recent and weak at 1.3185 just above the brief Thursday surge to 1.3174 and extant from a series of tops in mid-December. Beyond that the territory between 1.3200 and 1.3330, the next limit, was repeatedly traversed between July and December last year leaving no definitive boundary. The earlier highs from August and October at 1.3350 might provide resistance if a break of the 1.3330 level is without follow through. At long range we have 1.3445 and 1.3500.

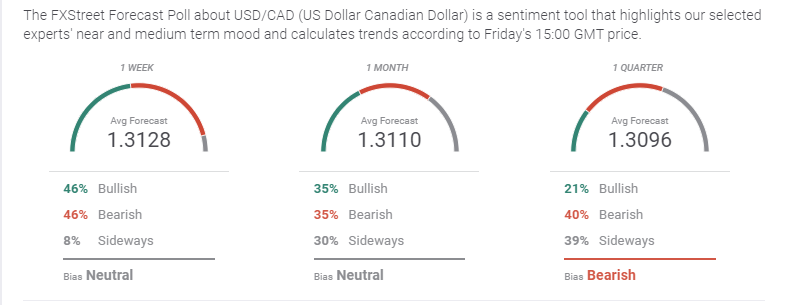

USD/CAD sentiment poll

In the one month view there is a slight rise in bullish feeling 35% from 30%, with an identical bearish sentiment at 35% and a small drop in the neutral conviction to 30% from 35%. The forecast rate is 1.3110 from 1.3066.

The one quarter forecast moves slightly higher to 1.3096 from 1.3080 with an incongruent switch to 21% bullish from 44%, an increase in both bearish sentiment to 40% from 31% and neutral to 39% from 25%. The implication here is that the one week and one month forecast will not, given current information, produce a sustained trend higher.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.