US vs Eurozone: Bank capital requirements are hardly comparable

According to an unpublished study conducted within the Single Supervisory Mechanism (SSM), if it were to perform its functions in the Eurozone, the US supervisor would be stricter, in terms of risk-weighted capital requirements, with respect to the systemically important banks (G-SIBs) established there, than the single supervisor of the Eurozone. The methodology of the exercise on which this conclusion is based has not been shared. However, it seems very complex to define.

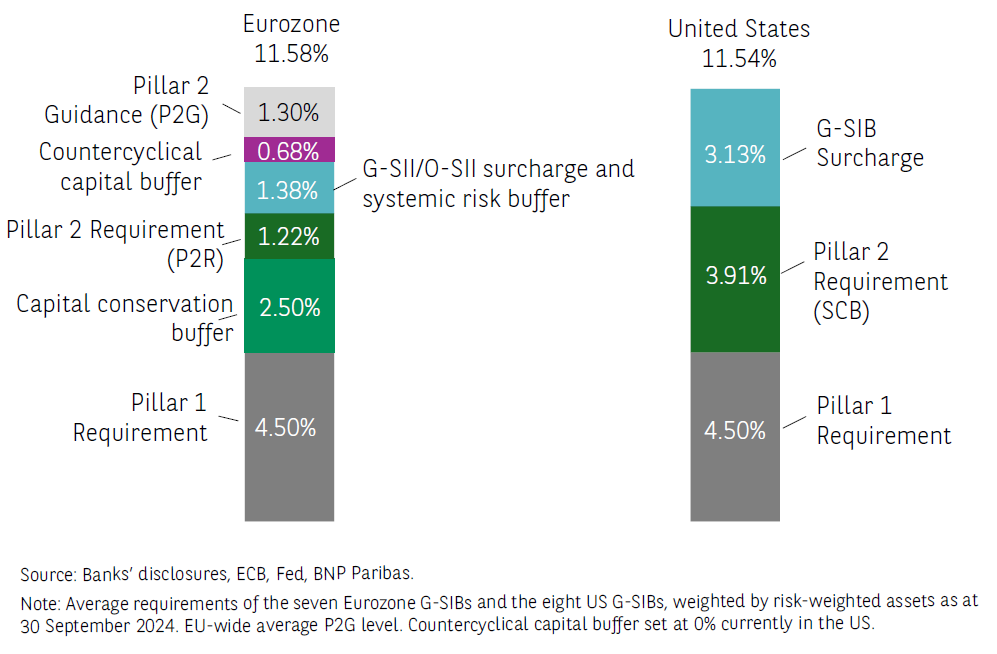

Average common equity tier 1 requirements of systemically important banks since 1st January 2025

The overall risk-weighted capital requirements and guidance of banking institutions consist of a stack of buffers: a common minimum base (Pillar 1 requirement, capital conservation buffer), institution-specific buffers according to its characteristics and exposures (countercyclical capital buffer, systemic risk buffer, buffer for global systemically important banks, buffer for other systemically important institutions), Pillar 2 requirements set by the supervisor (the P2R defined as part of the ECB's SREP (Supervisory Review and Evaluation Process), the SCB (Stress Capital Buffer) derived from Fed stress tests) and Pillar 2 guidance (the P2G based on ECB stress tests). Since 1st January 2025, the average risk-weighted capital requirement (including P2G) for the seven G-SIBs in the Eurozone has been 11.58%, which is almost the same as the level for the eight US G-SIBs (11.54%).

Of course, this mere comparison of capital requirements does not indicate the relative severity of the prudential frameworks. The business models, risk intensity and balance sheet structures of institutions differ; the expectations of supervisors, institutional frameworks, the role of banks and the process of intermediation, are specific to each of the two jurisdictions.

But assessing what the capital requirements of Eurozone G-SIBs would be if they were subject to the current US prudential framework poses further challenges. One challenge would be to estimate the Pillar 2 requirement specific to each institution, as this depends on the results of the Fed's stress tests, which are difficult to replicate for Eurozone banks. To overcome this obstacle, the SSM researchers assigned, in their simulation, a fictitious SCB to each G-SIB according to its risk profile, based on the US examples tested by the Fed[4], a relatively strong ad hoc hypothesis. Above all, the capital requirements arising from the imposed ratios are closely linked to the outstanding amount of risk-weighted assets. However, in the US, the CET1 requirements of the G-SIBs apply to a calculation basis that: 1) favours the standardised approach for measuring credit risks (while in the EU and the Eurozone, the use of internal models, encouraged by Basel II and the CRD to encourage banks to reduce their risks, will be gradually limited by the implementation of the output floor); 2) relies on advanced approaches for measuring market risks (but, unlike in the Eurozone, there is currently no plan to apply the latest Basel III recommendations); and 3) ignores (unlike in the Eurozone) operational risks. In our view, these measurement discrepancies impair the comparability of CET1 requirements and limit the scope of the exercise.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.