US September Consumer Price Index: September inflation supports a November taper

- Consumer inflation rises 0.4% in September to 5.4% annually, highest in 13 years.

- Food and gasoline climb 1.2% on the month, 4.5% and 42.1% on the year.

- Core CPI gains 0.2%, as forecast, to 4% yearly.

- St. Louis Fed President Bullard says Fed should be more aggressive in tapering.

Food and gasoline were the driving facts in US consumer inflation last month, pushing the price index to its highest annual increase in 13 years while the core rate remained stable.

The Consumer Price Index (CPI) rose 0.4% last month after a 0.3% gain in August, reported the Labor Department Wednesday. A 0.3% increase had been predicted by analysts.

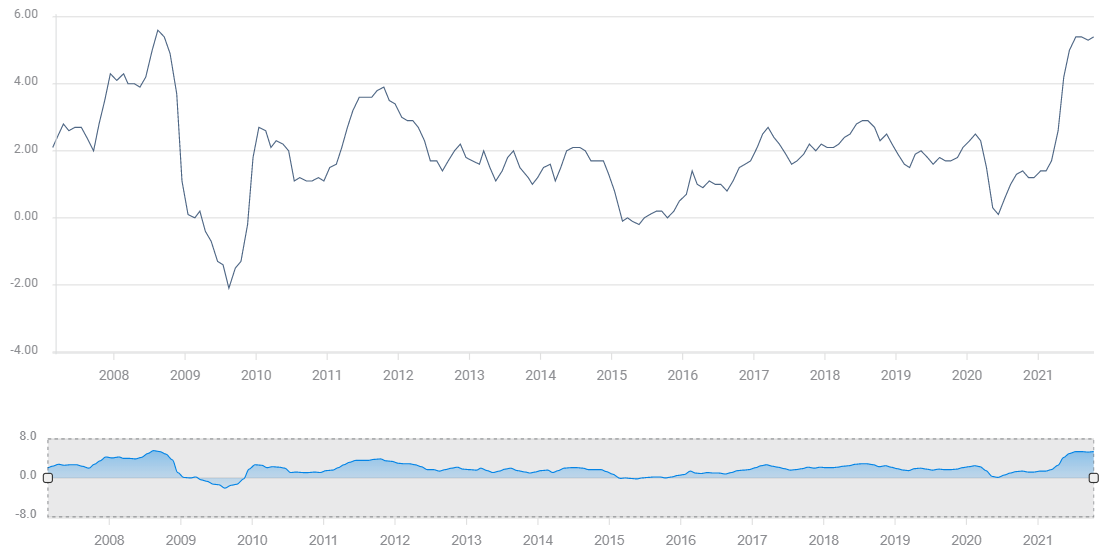

CPI

Over the last year prices climbed 5.4%, slightly ahead of the 5.3% forecast. It was the largest 12-month increase since July 2008 and the second highest in three decades

CPI

Core CPI, excluding food and energy prices, rose 0.2% in September up from 0.1% in August and was unchanged at 4% for the year.

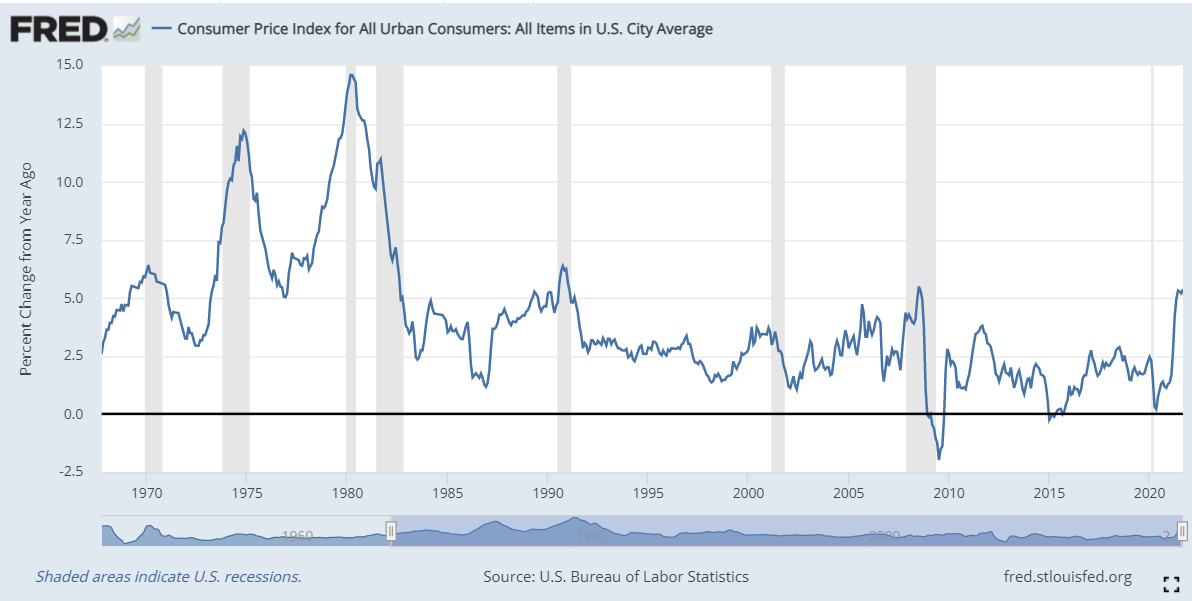

CPI details

Food prices climbed 1.2% for the month after a 0.4% increase in August and were 4.5% higher on the year. Meat expenses were up 3.3% in September and 12.6% annually.

Gasoline prices rose 1.2% last month following a 2.8% increase in August and a 2.4% gain in July, bringing the annual surge to 42.1%. Fuel oil, which heats many older homes, jumped 3.9% in September and is 42.6% more costly on the year.

Shelter expenses added 0.4% for the month and 3.2% for the year. The homeowners rental equivalent rose 0.4% in September, its biggest monthly increase since June 2006.

Several categories of consumer goods saw losses, underlining the intensity of the generalized increase in the economy, despite sector declines..

Used car prices, which had received much attention recently, dropped 0.7% for the month, lowering the 12-month gain to 24.4%. With new cars in short supply due to component and computer chip shortages, prices rose another 1.3% in September, leaving the annual increase at 8.7%.

Airline fares fell 6.4% in September.

Clothing prices slipped 1.1% in September while transport costs fell 0.5%. Nevertheless, purchase costs in both sectors were higher on the year, 3.4% and 4.4% respectively.

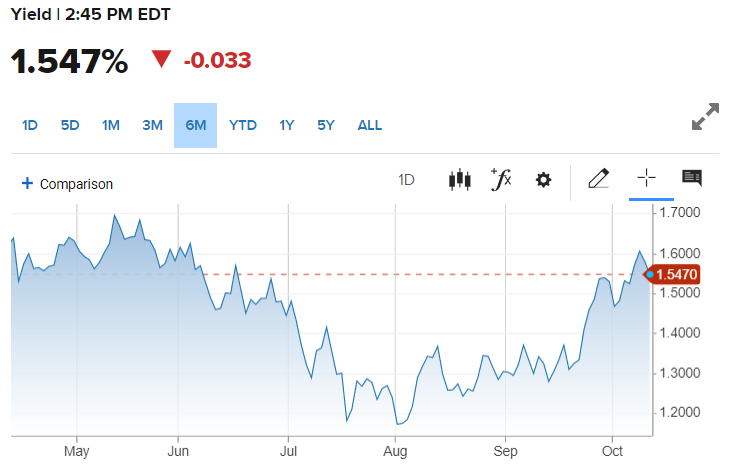

Market response

With consumer prices for September largely as anticipated, and having avoided a feared acceleration, Treasury yields retreated from their sharp increases of the past three weeks.

The 10-year yield had fallen 3 basis points to 1.547% by the early afternoon. The 30-year shed 6 points to 2.04%.

10-year Treasury yield

CNBC

Equites were flat with the Dow falling mere points and the S&P 500 rising about 0.10%.

The dollar lost ground against all the majors but retained most of its recent gains.

Federal Reserve

Markets have been anticipating that the Federal Reserve’s long-bruited taper of its $120 billion a month in bond purchases will be announced at the November 3 meeting

St. Louis Fed President James Bullard said in a Tuesday interview on CNBC that he supports starting the taper process in November and that the bank should be more aggressive in withdrawing economic support.

Also on Tuesday, Atlanta Fed President Raphael Bostic said the causes of the current inflation “will not be brief.”

These comments were backed up by the minutes of the last Federal Open Market Committee (FOMC) released at 2 pm which elaborated on the September statement, “If progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted.”

Conclusion

The September CPI numbers have not moved the discussion of the prospective Fed taper in either direction.

Consumer inflation is at its highest level in a generation and the factors driving the price gains, particularly wages and energy costs, are proving to be far more than transitory.

Labor, component and raw material shortages, shipping delays and consumer demand are all conspiring to drive prices to their highest sustained increases since the1980s.

The Fed’s anticipated November 3 taper strike remains on track.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.