US President Trump proposes new Auto Import Tariffs up to 25%

The US is considering new tariffs of up to 25% on imported vehicles and the President has instructed the Commerce Department to investigate the proposal on section 232 national security grounds. This has seen risk sentiment remain subdued with USDJPY down to fresh lows around 109.400 after falling from highs of 110.800 yesterday. This is negative for auto companies selling into the US but plans are in their early stages. US equity markets are off the lows from yesterday but Asian markets fell lower overnight with the Japanese market down to 22400.00 as a result. Reports from North Korea added to the negative sentiment after they suggested that they are reconsidering their upcoming meeting with the US after a verbal spat with the US Vice President. AUDUSD recovered earlier losses to trade around 0.78890. The US dollar selling accelerated after the FED minutes with 10 year yield falling under 3.00% after a strong hint of a rate hike at the 13TH of June meeting.

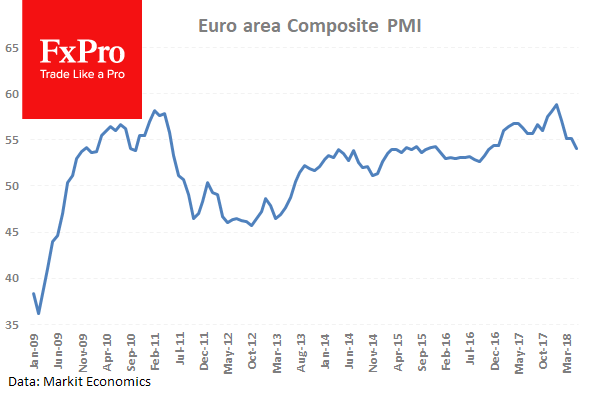

Eurozone Markit Manufacturing PMI (May) was 55.5 against an expected 56.0 from 56.2 previously. Markit Services PMI (May) was 53.9 against an expected 54.6 v 54.7 previously. Markit PMI Composite (May) was 54.1 against an expected 55.1 from 55.1 prior. This data came in softer once again after hitting highs in December and January. The continued fall in this data will be of concern for the ECB and may slow the path of monetary policy. EURUSD fell from 1.17169 to 1.16984 at which point buyers stepped in and brought price back up to 1.17474.

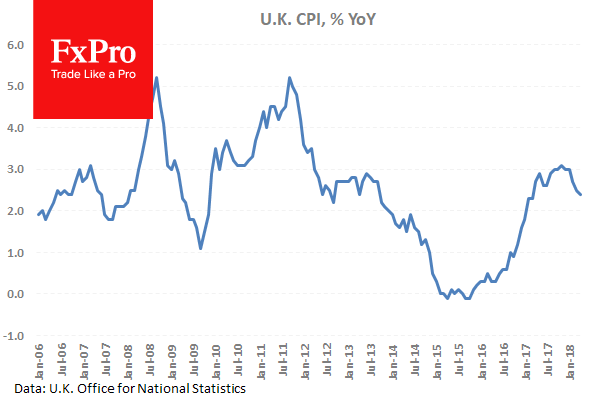

UK Consumer Price Index (YoY) (Apr) was 2.4% against an expected 2.5% from 2.5% previously. Core Consumer Price Index (YoY) (Apr) was 2.1% against an expected 2.2% from 2.3% prior. Consumer Price Index (MoM) (Apr) was 0.4% against an expected 0.5% from 0.1% prior. Retail Price Index (MoM) (Apr) was 0.5% versus an expected 0.5% against 0.1% previously. Retail Price Index (YoY) (Apr) was 3.4% against an expected 3.4% from 3.3% prior. These data points show CPI slipping slightly again. The yearly figure is still above the Bank of England’s 2% target since March of 2017 due to the change in the value of the pound after brexit. However the BOE says that inflation is likely to move back to 2% in 2018.

Producer Price Index – Input (MoM) n.s.a. (Apr) was 0.4% against an expected 1.0% from -0.1% previously which was revised up to 0.1%. Producer Price Index – Input (YoY) n.s.a. (Apr) was 5.3% against an expected 5.8% from 4.2% previously which was revised up to 4.4%. Producer Prices increased from previous readings, with higher revisions, but not by the amount expected. GBPUSD fell from 1.33832 to 1.33459 after this data release.

US Markit Services PMI (May) was 55.7 against an expected 54.9 v 54.6 previously. Markit PMI Composite (May) was 55.7 against an expected 55.0 from 54.9 prior. Manufacturing maintained its strong improvement since a low in May 2016.

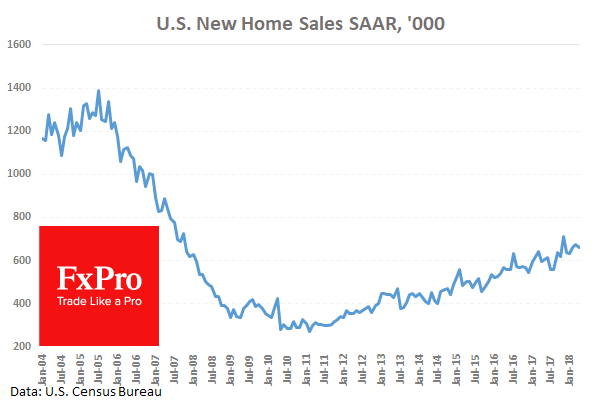

US New Home Sales (MoM) (Apr) were 0.662M against an expected reading of 0.679M from 0.694M previously which was revised down to 0.672M. The data was expected to strengthen after it beat the consensus of 0.630M last month but it missed expectations and came in lower than last month’s reading which was also revised down. This reading is still strong and shows confidence in the US housing market. USDJPY was trading at the 110.000 area when the data was released. It moved up to resistance at 110.173 before selling off to 109.885.

EURUSD is up 0.11% overnight, trading around 1.17074.

USDJPY is down -0.54% in the early session, trading at around 109.483

GBPUSD is up 0.16% this morning trading around 1.33665.

USDCAD is up 0.18% overnight, trading around 1.28528

Gold is up 0.07% in early morning trading at around $1,294.22

WTI is down -0.26% this morning, trading around $71.58

Author

Team FxPro

FxPro

FxPro is a UK headquartered online broker providing contracts for difference (CFD) on foreign exchange, shares, futures and precious metals primarily to retail clients.