US Non-Farm Payrolls Quick Analysis: The complete labor market surprise

- Non-farm payrolls rise by 2.54 million in May, rather than losing 8 million.

- Unemployment rate fell to 13.3% from 14.7%, much better than the -19.8% prediction.

- Underemployment rate falls to 21.2% from 22.8%.

- Equity futures soar, dollar gains, Treasury yields rise.

The labor market collapse reversed in May as a totally unexpected gain in employment underlined the resilience of the American economy and the positive impact of the government’s efforts under the $2 trillion Payroll Protection Program to keep people at work.

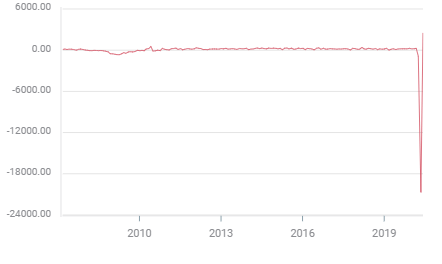

Non-farm payrolls rose by 2.54 million last month, a vast improvement from the 20.5 million who were furloughed in April and less than half the -8 million forecast.

Non-farm payrolls

Continuing unemployment claims had signaled two weeks ago that people might be returning to work when the total receiving unemployment benefits dropped 4.074 million instead of rising 838,000.

Private payrolls for May from Automatic Data Processing (ADP), the paycheck preparation giant that covers about one-sixth of the US market, suggested the same when they fell just 2.76 million rather than the 9 million consensus forecast.

Underemployment and initial claims

The unemployment rate, U-3, fell to 13.3% in May from 14.7% in April and 4.4% in March. That 8.9% jump in sixty days of reporting is still the fastest rise in joblessness in US records that go back almost a century. The highest unemployment in US history was 25.6% in May 1933.

The underemployment or U-6 rate, that includes individuals who have looked for work in the past year rather than just the prior month of the traditional U-3 list declined to 21.2% from 22.8%.

Almost 43 million people have filed initial jobless claims, an astonishing 26% of the workforce. In the week of May 22 13% of workers, 21.5 million people, were collecting unemployment benefits.

Market reaction

The economic debacle has practically vanished from the equity and currency markets. Dow futures jumped from 280 points before the release to more than 600. The Dow and S&P have largely erased their pandemic losses with the Dow down 5.92% on the year and the S&P 500 off 2.59% before the market open on Friday.

The dollar gained after the release initially rising about 30 points versus the euro and about 50 against the yen. Over the past three weeks the dollar has surrendered all of its pandemic risk-premium and is trading at pre-crisis level in all the major pairs.

Treasury yields spiked following the news with 10-year surging above 0.9% and the 2-year scaling 0.2%.

National impact

The economic collapse and the seemingly endless string of negative superlatives in economic statistics from the labor market, retails sales, durables good and soon to come second quarter GDP brought on by the imposed economic shutdowns has upended normal life in the United States.

Early concerns that the food supply chain might crack as people hoarded food and transport workers were unavailable to ship produce and goods to markets have proved to be false. Except for a few early instances of stripped supermarkets and distancing regulations food shopping has been unaffected.

Even though all states have lifted their shelter-in-place orders, many businesses remain closed and restrictions still limit social gatherings.

The states that reopened their economies first, Georgia, Texas and Florida have seen no appreciable rise in coronavirus cases or fatalities but despite those examples states on the coast, California and New York for example remain under modified closure orders with large swatch of their commercial life still closed.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.