US Non-Farm Payrolls Preview: Three is not the charm

- Two weak months out of four in NFP have rattled markets

- ADP’s May plunge adds to employment gloom

- Slowing economic growth and China may inhibit job creation

The Bureau of Labor Statistics (BLS) a division of the US Labor Department will issue its Employment Situation Report for June on Friday July 5th, at 8:30 am EDT, 12:30 pm GMT.

Forecast

Non-farm payrolls are expected to rise 160,000 in June following a 75,000 gain in May. Private payrolls are projected to add 153,000 workers after the prior month’s 90,000 increase. Manufacturing payrolls are predicted to be unchanged after adding 3,000 in May. Government payrolls at all levels lost 15,000 workers in May.

The U-3 unemployment rate is anticipated to be stable at 3.6%. Average hourly earnings will rise 0.3% on the month following 0.2% in May and 3.2% on the year, up from 3.1%. The work week will be unchanged at 34.4 hours.

The Employment Situation Report

The June report will have a greater impact than usual because of the volatility in the headline payroll figure over the past four months and the plunge in ADP payrolls in May to 27,000.

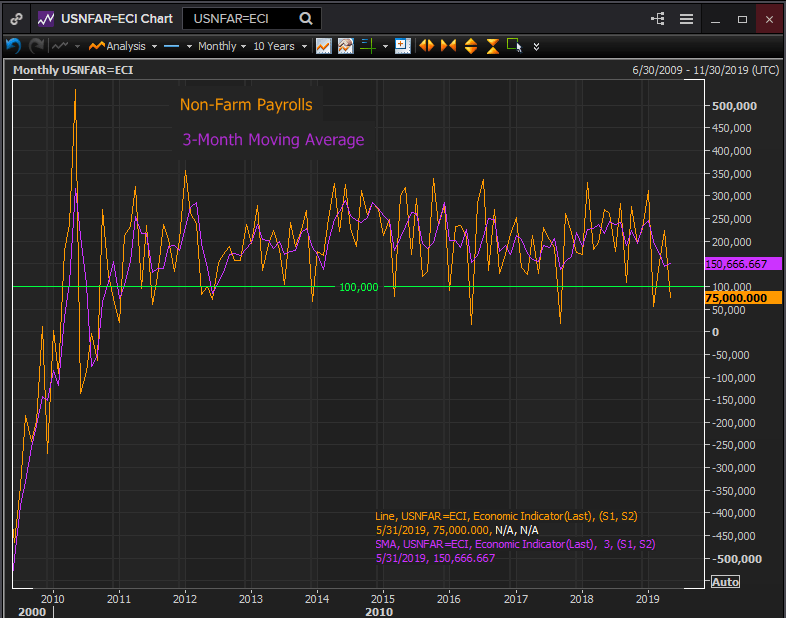

January’s 312,000 NFP brought the three month moving averge to 245,000 the best in almost three years. But February’s 56,000 and then May’s 75,000 came in far below expectations and beneath the average entering each month. May’s result dropped the average to 151,000 the lowest since September 2017 even though the interposed months of March and April at 153,000 and 224,000 respectively were much closer the prior trend.

Anomalous single months with payrolls far below adjacent months are common in the record.

In the past four and a half years there have been seven: March 2015 77,000, 3-month moving average 179,000; January 2016 90,000, 3-month moving average 202,000; May 2016 15,000, 3-month moving average 153,000; September 2017 18,000, 3-month moving average 135,000; September 2018 108,000, 3 month moving average 189,000; February 2019 56,000, 3-month moving average 198.000; May 2019 75,000 3 month moving average 150,000.

Reuters

It was not the occurrence of low payrolls in February or May this year that has excited worried speculation that the excellent job market of the past two years is beginning to crack but the proximity, two weak months out of four. Added to NFP concerns for 75,000 in May was the match with ADP that reported only 27,000 new positions, its lowest number in almost a decade. Though three month earlier in February when NFP registered just 56,000 new jobs, ADP reported a strong 220,000 jump in private payrolls.

If the ADP forecast for June at 140,000 and the NFP prediction of 160,000 are accurate, they will have at least temporarily confirmed the drop in job creation in the second quarter.

The Employment Situation Report Background

Usually referred to as payrolls, non-farm payrolls, or NFP the Labor Department’s monthly catalogue of the job economy is the best known, most followed and actively traded US statistic.

The report consists of two surveys. The establishment survey polls non-farm businesses and produces the payrolls numbers, wages, weekly hours, labor force participation rate and other gauges. The household survey queries a representative sample of the working age civilian population and classifies each person as employed, unemployed or not in the labor force and calculates the unemployment rates.

The U-3 unemployment rate is the best known measure and the one that is normally meant in common parlance. It was 3.6% in April and May. To be considered unemployed under this measure a non-working individual had to have looked for work in the month prior to the survey.

The U-6 or underemployment rate counts someone unemployed if they had looked for work in the prior year. It was 7.1% in June. A person who is not employed or unemployed under the U-3 definition is not part of the official workforce.

The non-farm payroll figure includes each month a BLS estimate of the number of jobs created at new companies that have not yet been counted for tax purposes. These estimated jobs are revised at a later date against company and government information. The NFP report is one of the most up to date of the government’s many analytical efforts as its data is about one month old.

Coincident labor market statistics

Non-farm payrolls give the most encompassing image of the US job market but three other statistics are useful in judging the health and direction of job creation: ADP payrolls; initial jobless claims; and the employment purchasing managers’’ indexes from the Institute for Supply Management.

NFP and ADP

The ADP and NFP figures are complimentary. The ADP figures are based on its 411,000 corporate clients while the BLS numbers cover the entire economy and include government hiring at all levels, federal, state and local.

The correlation between the two numbers is good. One of the reasons for the extra attention on the June NFP was the coincidence of the two statistics in May.

Employment PMI

The PMI surveys are sentiment indicators. Business executives are asked to characterize their current and future hiring plans. As a gauge of attitudes they do not necessarily predict actual employment actions.

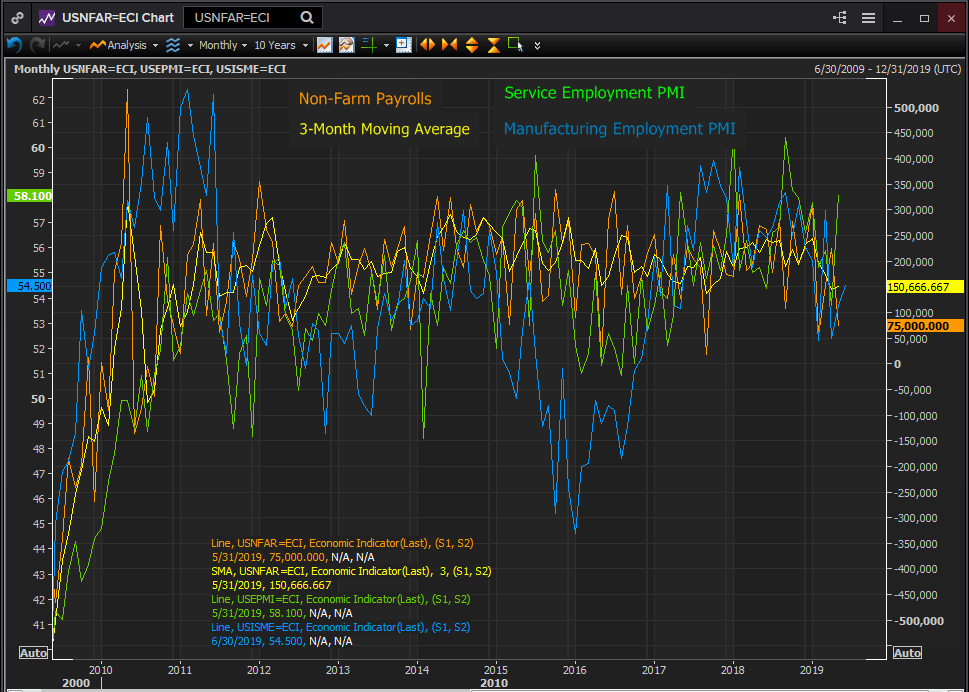

In 2015 and 2016 the manufacturing employment index dropped sharply, falling below 50 for much of the period but actual employment was healthy with NFP averaging 227,000 in 2015 and 194,000 in 2016.

Reuters

The manufacturing employment PMI rose to 54.5 in June from 53.7 in May though it is down from its highs of last year. Throughout the period of its fall, roughly September through April payrolls were unaffected by the worries of the executives. In April the NFP 12-month moving averge was 212,000, in September 2018 it had been 219,000.

Services employment PMI jumped to 58.1 in May from 53.7 prior. It is a relatively strong reading, commensurate with many over the past two year and not, in itself indicating a rising disinclination to hire.

The US-China trade dispute has clearly taken a toll on the optimism of business executives particularly in the manufacturing sector. Nonetheless until the last four months there had been no carryover into hiring. The volatility of the last four months in the NFP may be an early sign of an actual impact or they may be an unusual but not significant statistical event.

Initial jobless claims

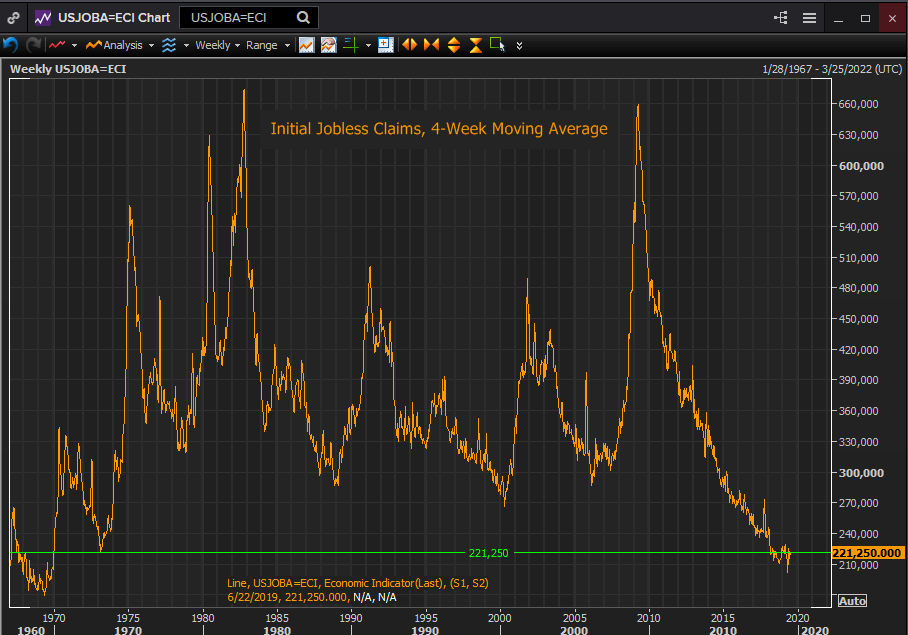

Initial claims have been at or near five decade lows for more than a year. Though claims are a good indicator of serious trouble in the labor market they are less useful as an indicator for a period when firms have curtailed or stopped hiring but not yet begun to lay off workers.

The 4-week moving of 221,250 in the third week of June is the lowest since January 1970 a period in which the US population grew 60%.

Reuters

Conclusion

Is excellent job creation, a staple of the US economy for two years and more about to shift to a lower level? Have the well documented declines in business optimism finally worked into business decisions?

The appearance of two very weak payroll reports coupled with similar poor numbers from ADP would seem to indicate that more than statistical chance is at work. Economic growth has shifted lower in the second quarter. The US/China trade dispute, the source of so much business angst does not seem to be headed for resolution anytime soon. In fact given the situation, it would be remarkable if there was no impact on the labor market.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.