US Non-Farm Payrolls Preview: Look back, no one is gaining

- Payrolls expected at trend in July after an up and down quarter

- ADP jobs were as forecast following two weak months

- Coincident indicators remain healthy

The Bureau of Labor Statistics (BLS) a division of the US Department of Labor will issue its Employment Situation Report for July on Friday August 2nd, at 12:30 GMT, 8:30 EDT.

Forecast

Non-farm payrolls are predicted to rise 164,000 in July after the May gain of 224,000. Private payroll are expected to add 160,000 following June’s 191,000. Manufacturing payrolls will increase 5,000 in July after adding 17,000 in June.

The unemployment rate (U-3) is expected to be stable at 3.7%. Average hourly earnings will rise 0.2% in July as the month before and annual average hourly earnings will improve 3.2% up from 3.1% in June. The work week will be unchanged at 34.4 hours.

The Employment Situation Report background

Normally shortened to non-farm payrolls, payrolls or simply NFP, the Labor Department’s monthly recitation of the US labor market is the best known, most followed and actively traded American economic statistic.

The report consists of two surveys. The establishment survey tracks non-farm businesses and produces the payrolls numbers, wages, weekly hours, labor force participation rate and other measures.

The household survey samples a representative segment of the working age non-military population and classifies each person as employed, unemployed or not in the labor force and calculates the unemployment rates.

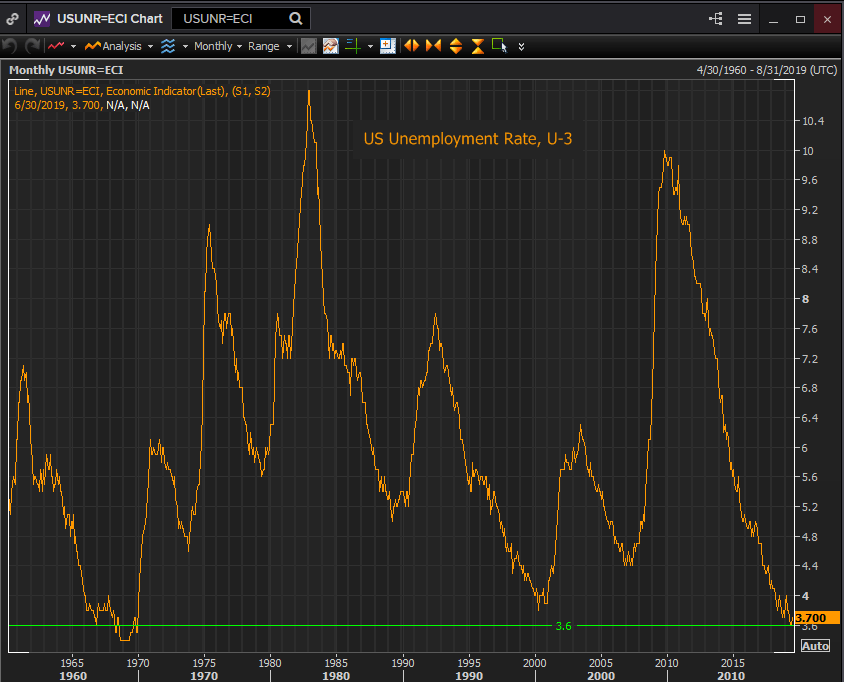

The U-3 unemployment rate is the best known gauge and the one that is commonly cited. It was 3.7% in June. Unemployment here is restricted to non-working individuals who have looked for a job in the month prior to the survey.

Reuters

The U-6 or under-employment rate includes anyone who has searched for work in the prior year. It was 7.2% in June. A person who is not employed or unemployed under the U-3 definition is not part of the official workforce.

The non-farm payroll figure includes a BLS estimate for the number of jobs created at start-up firms that have not yet been reported to the government. These conjectural jobs are revised at a later date against company and government information.

The NFP report is one of the timeliest of the government’s many analytical efforts as its data is about one month old.

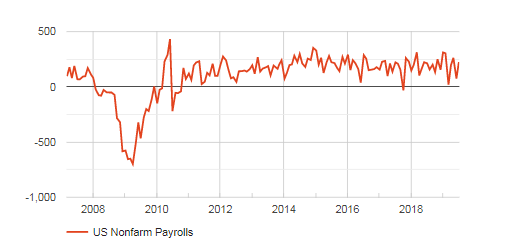

Non-Farm Payrolls

The June 224,000 payroll report mollified market concerns brought on by weak NFP numbers in February and May and below trend ADP figures in May and June that the labor economy was slipping into lower speed. While payrolls have continued the positive trends of the past several years they have declined somewhat this year.

FXStreet

The January 3-month moving average was 245,000. By April it was 141,666 and in May 147,000 both the lowest since September 2017. In June it was back to 170,666.

The volatility in NFP this year has been somewhat higher than normal. Two below trend results, February and May, in six months is unusual but not statistically meaningful. In the past four and a half years there have been seven months when payrolls fell below 100,000 without disturbing the overall trend in job creation.

Coincident labor market statistics

Many economic statistics cover a portion of the labor market. Three in particular are often used as indicators to the nationwide picture in the payrolls report: ADP payrolls, initial jobless claims and the employment purchasing managers’ indexes from the Institute for Supply Management

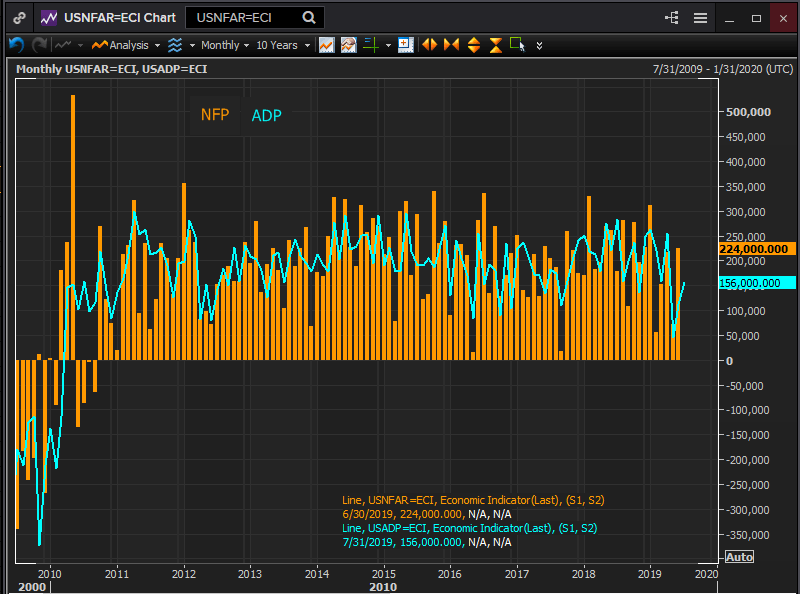

NFP and ADP

The two sets of job figures are complimentary. There are three basic differences. The ADP numbers are based on their approximately 411,000 clients. The BLS numbers cover the entire economy including all levels of government employment. The ADP numbers are actual, that is they are real paying jobs. The government payroll figures, in addition to payrolls, contain an estimate of the number of newly created but unreported jobs at start-up firms. Those jobs may or may not exist and they may or may not last as most new businesses fail. These estimated jobs are corrected against tax rolls at a later date.

The trend correlation between the two numbers is good, the individual months less so.

Reuters

The ADP payrolls continue to show good if slightly slower hiring across a wide range of businesses. The 3-month moving average has fallen from 244,333 in February to 104,666 in July. The primary culprits being May and June at 46,000 and 112,000. The 12-month average has slipped from 219,666 in February to 182,666 in July. The July result of 156,000 lies between the 3 and 12 month averages.

The NFP averages have moved in similar fashion. The 3-month has decreased from 245,000 in January to 170,666 in June with the 12-month dropping in the same period from 235,000 to 191,750.

ADP and NFP: Consensus and Actual

Despite the large month to month volatility in the ADP and NFP figures, the consensus forecasts for both as surveyed by Reuters have been stable and remarkably accurate.

The ADP average prediction for this year has been 172,833 with a range of 140,000 to 189,000. The six month average of the actual statistic is 173,333 and the range is 41,000 to 264,000.

The average consensus prediction for the NFP has been 175,833, with a range of 160,000 to 185,000. The first half average for the actual NFP has been 172,666 with a range of 56,000 to 312,000.

Initial jobless claims

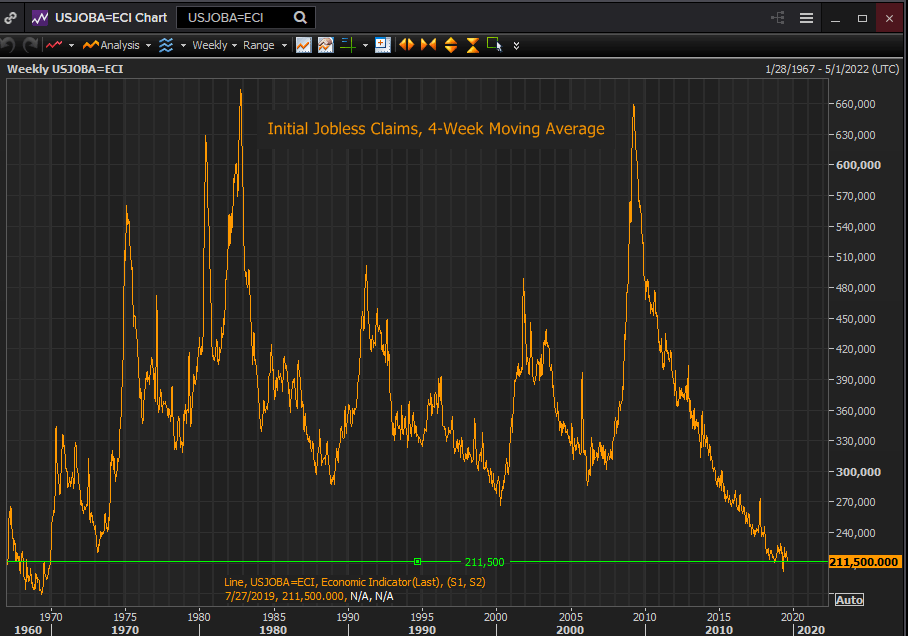

Initial claims have been setting records for more than a year. It has been nearly 50 years since so few people were filing for unemployment benefits and in those decades the US population has grown 60%.

Reuters

Claims are a good indicator of serious trouble in the labor market since filing for unemployment benefits is often the first response of most people who lose their jobs.

The 4-week moving of 211,500 in the week of July 26th is, prior to October last year, the lowest since December 1969.

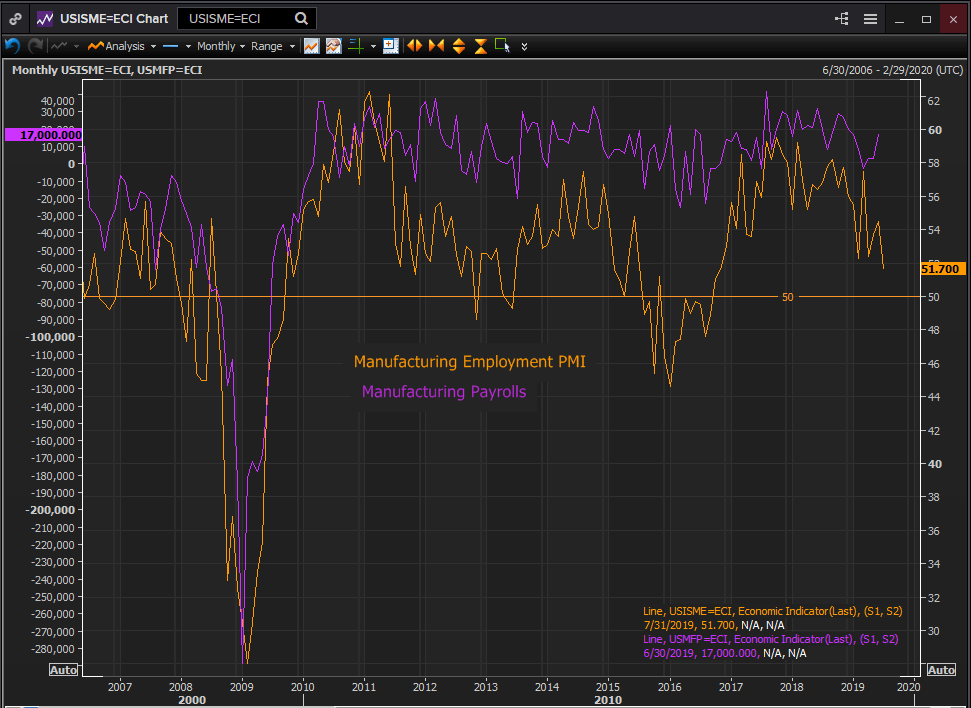

Employment PMI

The purchasing managers’ indexes from the Institute for Supply Management are sentiment indicators. The do not report sales, production or hiring results. Business executives are surveyed and asked to assess, in the case of the employment indexes, their current and future hiring plans. As a measure of attitudes they do not necessarily predict actual employment actions.

In 2015 and 2016 the manufacturing employment index dropped sharply, falling below 50 for extended periods each year but the translation to hiring was not uniform.

Employment was healthy in 2015, despite executive misgivings, with an average of 5,800 monthly jobs. However, 2016 was a different story. Hiring began the year in fine shape at 22,000 in January but with payroll losses in six of the subsequent months the year ended with a slightly negative average of 600 jobs lost per month.

Manufacturing employment PMI has been volatile this year. From 57.7 last November it crashed to 52.3 in February in the aftermath of the partial government closure in January, shot back to 57.5 in March, fell to 52.4 in April, to 54.5 in June and has now dropped to its lowest in two and a half years at 51.7 In July.

Hiring has been weaker this year than in the prior averaging 7,500 a month to June in contrast to 20,333 in the six months to December and 23,666 in the half year to June 2018. The decline in optimism in the PMI employment indexes has been reflected in the job numbers.

Reuters

Services employment PMI has also been variable but its relative levels have been stronger. From 57.8 in January it was at 53.7 in April, climber back to 58.1 in May and slipped to 55.0in June. The July survey will be released on August 5th.

Overall job creation has fallen this year. The six month average was 172,166 in June down from 233,666 in January.

Conclusion

Hiring has retreated from its very strong levels of last year but that is a relative change. With the NFP 12 month average at 191,750 in June the labor market continues to create more jobs than needed to fill work force expansion and is slowly driving up wages. That excess employment has penetrated sectors of the labor market long suffering from weak employment. Unemployment rates for Hispanics and African-Americans have fallen to record low levels.

One of the Federal Reserve’s rationales for its 0.25% rate cut was the desire to keep the expansion, now the longest post-war, running and delivering jobs in those extended sectors of the economy.

The US-China trade dispute, Brexit and the much touted slowdown in global growth have had a negative effect on the outlook and hiring plans of business executives particularly in the manufacturing sector.

The US economy grew at a 2.6% rate in the first half. Initial jobless claims are lower than most economists though possible just a few years ago and although businesses are worried about the trade war with China and have pulled back on spending and hiring, the domestic economy is in good health.

With all of the accumulating and shifting economic and political concerns the US labor market has continued to produce jobs and wage. The risk for July remains on the upside.

* Apologies to Satchel Paige for the title

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.