US Manufacturing PMI March Preview: Markets return first, factories second?

- Manufacturing contraction expected to continue in March.

- New orders index forecast to remain positive.

- Nascent factory revival ended in viral outbreak.

The Institute for Supply Management (ISM) will issue its purchasing managers’ indexes (PMI) for the manufacturing sector in March on Wednesday April 1 at 14:00 GMT, 10:00 EDT.

Forecast

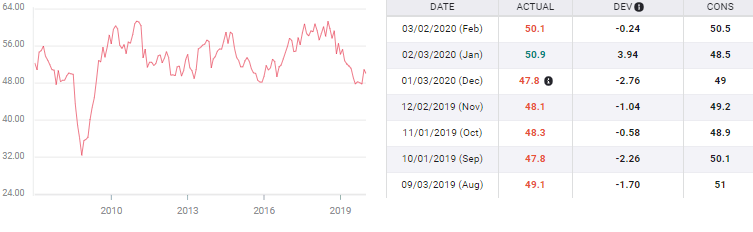

The purchasing managers’ index is projected to drop to 45 in March from 50.1 in February. The new orders index is predicted to rise to 50.2 from 49.8. Employment should fall to 45.4 from 46.9. The prices paid index is predicted to decrease to 41.3 from 45.9.

US manufacturing and the economy

The two-month recovery in manufacturing after five months of contraction will end in March as the viral outbreak in the US has shuttered plants and businesses across the country. Many factories have chosen to close for a few weeks even though it was not required by local governments. Closures will last for an indeterminate time determined by the progress of control efforts.

Manufacturing PMI

Manufacturing had slipped into gradual decline in the fall of 2018 after the best two years since the financial crisis as the US trade dispute with China escalated into a full-fledged trade war. The agreement between the world’s two largest economics announced in October halted the decline but it was the signing of the phase one deal in Washington on January 15 that prompted the surprise jump into expansion that month.

Prior to the virus the US economy was estimated to be growing at a 3.1% annualized rate in the first quarter by the Atlanta Fed. That prediction has dropped to 2.7% with the caveat that, as the model is dependent on released economic data, it does not capture or anticipate the impact of the public health efforts to deter the outbreak on the US economy.

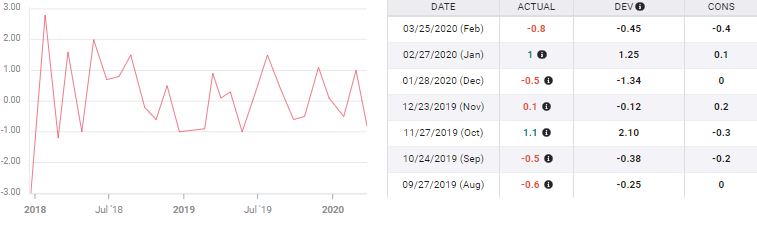

Business investment

As the US-China trade dispute intensified business spending ceased in the second half of 2019. The durable goods category non-defense capital goods, a widely followed proxy for business investment was flat for the second half, jumped 1% in January but fell 0.8% in February. Whatever the future business attitude toward China, investment will wait until the pandemic has run its course.

Non-defense capital goods ex-aircraft

Fed policy and government stimulus

Massive global liquidity provisions from the Federal Reserve and an equally huge stimulus and support program from Washington have helped to stabilize equity and credit markets.

The Dow has jumped almost 20% from its low close on March 23 at 18,951. Treasury yields have fallen over the last two weeks as central bank purchases have boosted prices and depressed returns.

Conclusion and market impact

Economic data from March and April will be historically grim. While the markets have taken a position on the eventual passing of the virus and seem increasingly convinced that the recovery will be swift and dramatic, business investment and sector recovery is likely to await more concrete information.

The US dollar retains the largest portion of the global safety trade though the panic buying phase has passed. As the global situation stabilizes and then improves risk will creep back into the markets and gradually deflate that dollar advantage but it will likely be replaced by the US economy’s faster recovery from the pandemic.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.