5.90% to 5.45%: Why the Pound ignored the bond market’s relief rally

Keir Starmer resigned on Monday, and the Pound barely moved. That near-silence is the tell. Sterling's real driver these past four months has not been the prime minister, nor the left-leaning frontrunner lining up to replace him, but the long end of the gilt curve, which answers to a force no British politician controls. Starmer is the sixth UK prime minister to leave office in under a decade, and with a successor due by September, he will soon make way for the seventh leader since the Brexit vote ten years ago this week. The market has seen this show before. What it is actually pricing sits in the bond market, not in 10 Downing Street.

The long end is the real prime minister

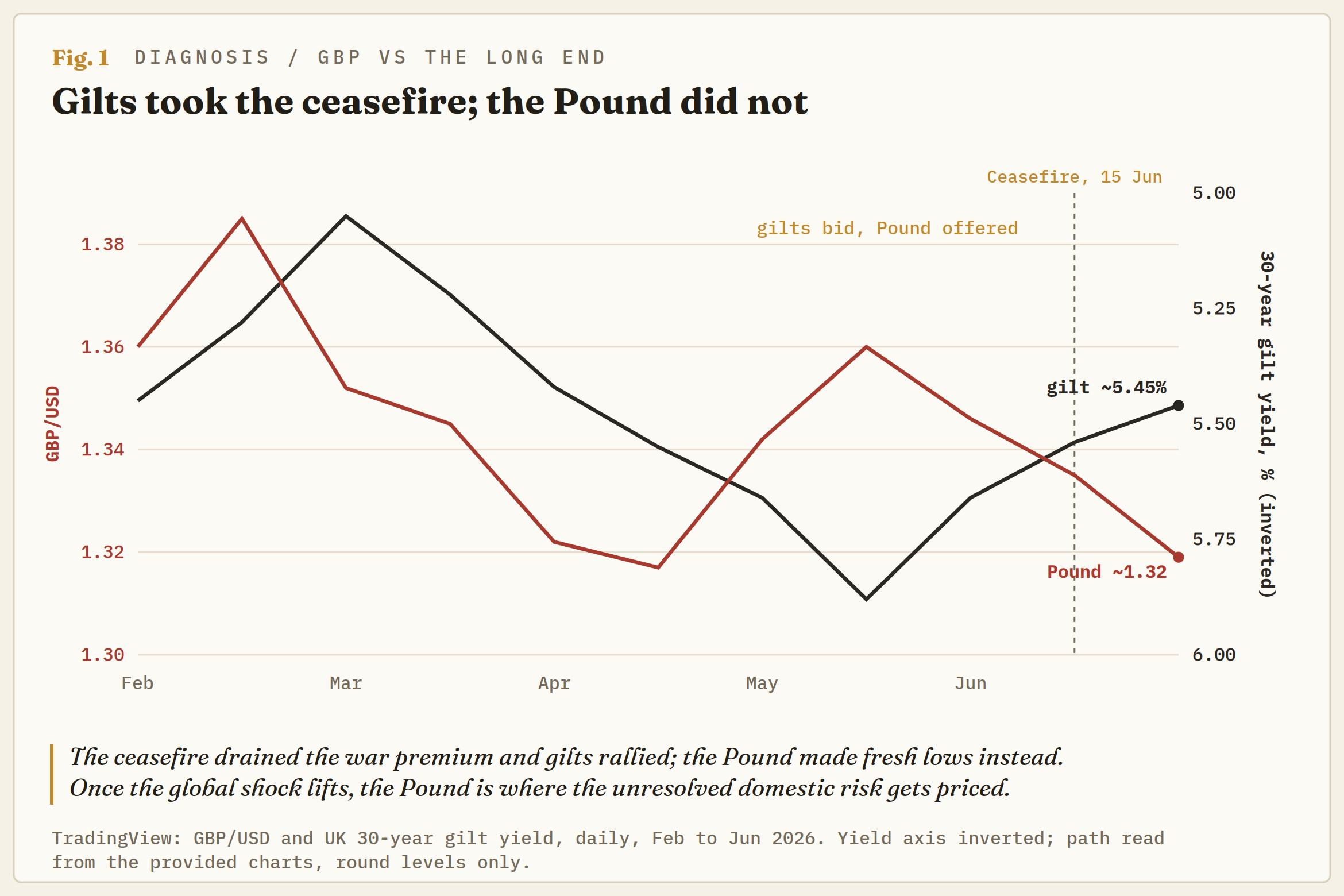

Strip the politics away, and the story of UK assets since late February is the story of one line on a chart: the 30-year gilt yield. It ran from a March trough near 5.00% to a spike close to 5.90% in May, a level Britain had not held since 1998, then unwound toward 5.45% once the US and Iran reached a ceasefire on June 15.

The Bank of England's (BoE) own analysis pins the bulk of last year's long-end move on higher term premium, the extra compensation investors want for holding long-dated debt, and lays most of that at the door of global forces rather than domestic ones. The proof sits across the Atlantic, where US 30-year yields hit multi-decade highs over the same stretch. The war was the trigger, an Oil and Hormuz shock that revived inflation fears worldwide; the ceasefire was the relief. None of it was minted in Westminster.

Why Britain rides the wave hardest

If the wave is global, the question is why Britain takes more water over the bow than anyone. Part of the answer is in the make-up of the debt. Around a quarter of UK government debt is index-linked, the largest share in the G7 and roughly twice the next-highest country, on some counts the highest proportion in the world. A large slice of the welfare bill, the state pension included, also rises with inflation. So a global energy shock does not merely lift gilt yields here; it feeds almost directly into the government's own bill.

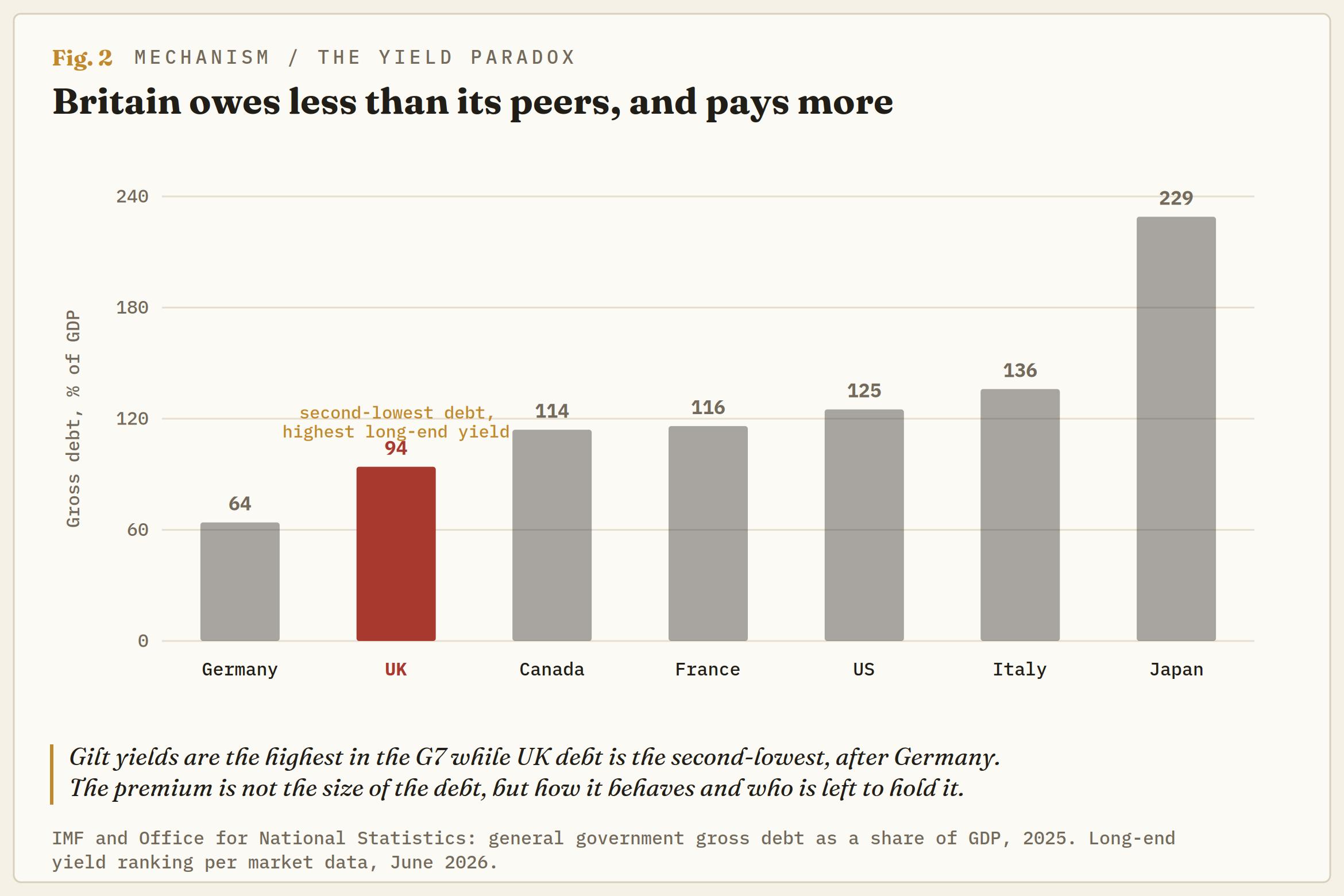

The International Monetary Fund (IMF) warned in April that the UK faces the biggest growth hit from the Iran war of any major economy, and cut its 2026 growth forecast to 0.8%. Hence, the paradox the leadership-obsessed reading misses entirely. Britain pays the highest yields in the G7 while carrying less debt than every G7 economy except Germany. This was never a story about the size of the debt. It is a story about how that debt behaves, and about who is left to hold it.

The privilege that just expired

For two decades, Britain borrowed long on unusually generous terms. The country's defined-benefit pension schemes needed long-dated assets to match their liabilities, and that steady, price-insensitive demand held the 30-year term premium down, at times below the 10-year, a position few governments ever enjoyed. That world has gone. The schemes are closed to new members and de-risking, and the natural buyer of the long end has stepped back. The bank treasuries taking their place want the government's credit but not its interest-rate risk, so they buy the front end; insurers still take some long paper, but not enough to fill the hole.

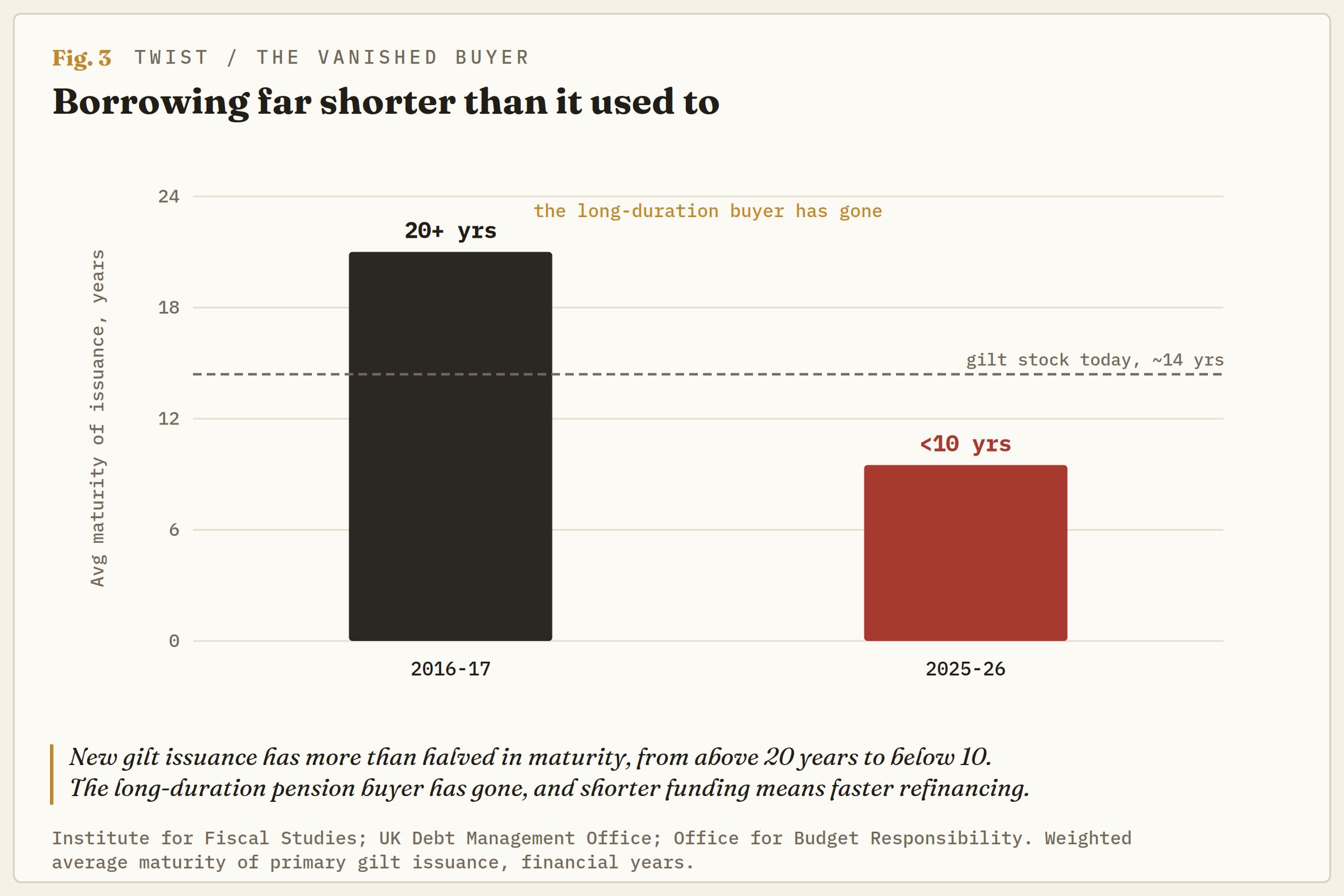

The pension and insurance funds that once held two-thirds of all gilts now hold barely a third, with overseas investors, now the largest holders, and leveraged funds that sell first and ask later filling the gap. The Debt Management Office has read the message and rotated supply to match it, from a weighted average maturity above 20 years a decade ago toward under ten years now, with short and medium gilts the bulk of this year's issuance.

That shift carries two charges the leadership story never mentions. The first is that a chunk of today's 30-year yield is simply the unwinding of that old compression, a home-grown term premium that is UK-specific, slow to move, and immune to any ceasefire; the global wave can recede and this piece stays put. The second is the trade the Treasury is making to keep the market clearing: funding shorter swaps duration risk for refinancing risk, so a rising share of the debt rolls over faster and re-prices at whatever rate prevails, just as quantitative tightening removes the one buyer, the Bank of England, that used to absorb the supply and turns it into a seller.

The same long-dated funding that once kept Britain's borrowing rate below its growth rate has flipped: that rate now sits above it, worst at the 30-year point, so the debt arithmetic the privilege used to flatter has turned against the Treasury too. None of this is in any candidate's gift. The privilege expired on its own, and no leadership contest brings it back.

The deckchair Westminster can move

That leaves the one layer a new prime minister actually controls, and it is the thinnest of the three: the premium markets attach to British political and fiscal credibility. Andy Burnham, the frontrunner, carries history here. His suggestion last September that the country should get beyond being beholden to the bond market triggered a gilt selloff at the time, and the market has not forgotten it. For now, it is taking him at his word. He has committed to the incumbent fiscal rules, has been assembling an economic team, and the early backing of a fiscally cautious rival has lifted the odds of a tidy handover over a drawn-out contest.

The real tests come later: who takes the Chancellor's job if Rachel Reeves is moved, and the autumn Budget. There is a sceptical case that the premium is overstated. Some argue the much-quoted reliance on foreign buyers is inflated by domestic pension money routed through offshore vehicles, and they note it was domestic funds, not foreigners, that broke the gilt market in 2022. On that view, with the war over and the succession orderly, gilts could yet be the asset that benefits. The bond market, rallying into the resignation, half believes it.

Why the gilt rally skipped the Pound

The currency does not. Gilts have taken a double tailwind, the peace dividend and the prospect of a clean succession, and yields have fallen the length of the curve, with the 10-year back near 4.80%. The Pound has banked none of it. It caught a small relief bid when Starmer confirmed his exit, then settled into the low-1.3200s, still some 3% below where it traded in February. The split is the point. Once the global excuse is gone, the currency becomes the instrument where the unresolved domestic question gets expressed.

A bond can rally on relief that the war is over and the handover looks clean; the Pound needs an actual answer on growth and fiscal credibility, and there is not one yet. Gilts will extend the benefit of the doubt. Sterling is withholding it until it sees a Budget.

The levels that matter

On the chart, the lean is lower. The Pound sits below its 200-day moving average around 1.3400, which now caps the bounces, and the 2026 low near 1.3150 is the first trip-wire beneath. But the level the whole question turns on is the big figure at 1.3000, last year's low, and the test strategists have flagged for the summer. Above it, a soft Pound is still a Pound on the benefit of the doubt, free to grind a 1.3000-1.3400 range while the leadership process and the Budget play out. A clean break below 1.3000 is the market revoking that credit, the point the residual political premium stops trading like a deckchair and starts pricing like fiscal stress.

The topside has to earn its keep: only a clean break above 1.3400, most plausibly on a market-friendly Chancellor pick, opens 1.3500. With options desks already leaning short Sterling, the tape sits with the bears until the politics hands the bulls something to trade.

The only question left

The gilt rally has answered the question the war asked. It has not touched the one the resignation leaves behind. The iceberg that did the damage is drifting off; what remains is the smallest of the three layers, the part Westminster can actually steer, and nobody yet knows how big the new government will let it grow. Bank the peace dividend and keep the bond market onside, and the Burnham premium stays a deckchair. Reach for the spending lever, and it becomes an iceberg of its own making.

The Pound, pinned at its lows while gilts celebrate, is not waiting on the man who left. It is waiting on the one who has not yet shown his hand.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.