US-Iran MoU agreed

US-Iran Pactum est

Pakistani authorities have announced that the US and Iran have reached a memorandum of understanding. Although the terms of the deal are still not clear, it seems that the Straits of Hormuz are to be gradually opened by Iran, while the US is to lift the blockade, the deal includes also Lebanon, while the stance of Israel is still unclear. The news have lifted the market mood supporting cryptocurrencies, equities and gold’s price, while the USD and oil prices are on the retreat.

RBA expected to remain on hold, BoJ to hike rates

In tomorrow’s Asian session, we get two interest rate decisions. In Australia, RBA is expected to remain on hold, yet given Australia’s inflationary pressures we may see RBA sounding hawkish which could provide some support for the Aussie. In Japan, BoJ is expected to hike rates and should the hike be materialised and possibly accompanied by a hawkish forward guidance by BoJ Deputy Governor Uchida (given BoJ Governor Ueda’s absence) we may see JPY getting some support.

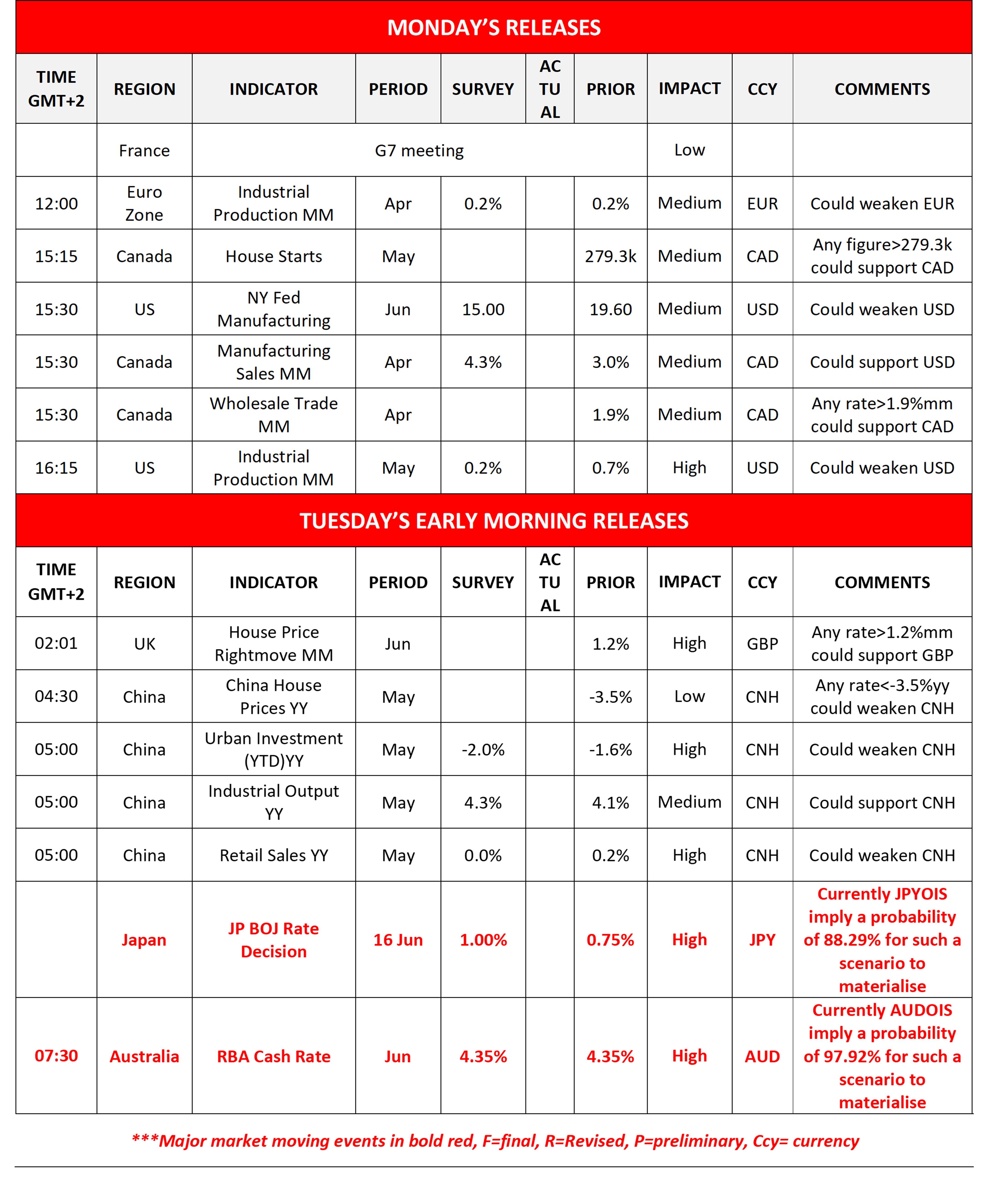

Other highlights for today

Today we get Euro Zone’s industrial output for April, Canada’s House Starts for May, Manufacturing sales for and wholesale trade for April and from the US the NY Fed manufacturing index and industrial production for May. In tomorrow’s Asian session, we get UK’s Rightmove House prices, China’s House prices, Urban investment, industrial output and retail sales, while BoJ and RBA are to release their interest rate decisions.

As for the rest of the week

On Tuesday we get Germany’s ZEW indicators for June. On Wednesday we get Japan’s Tankan indexes for June and May’s trade data, UK’s CPI rates for May, from Sweden Riksbank’s interest rate decision, the US retail sales for May and we highlight the Fed’s interest rate decision. On Thursday we get the interest rate decisions of Switzerland’s SNB, Norway’s Norgesbank, the Czech Republic’s CNB and the UK’s BoE, while we also note the release of New Zealand’s GDP rate for Q1, UK’s employment data for April, Canada’s Business barometer for June, and from the US the weekly initial jobless claims figure and Philly Fed Business index for June. On Friday we get Japan’s CPI rates for May, UK’s and Canada’s retail sales for May and April respectively.

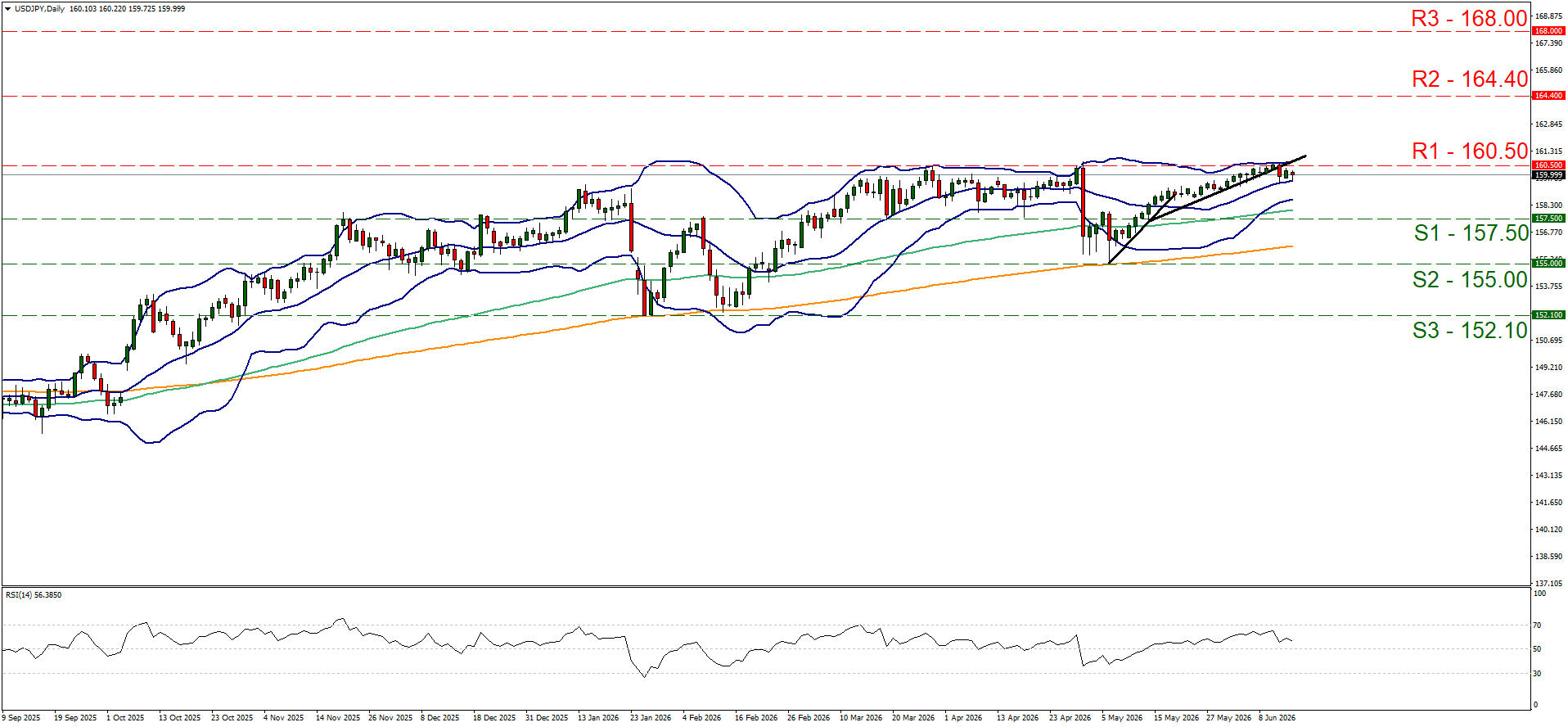

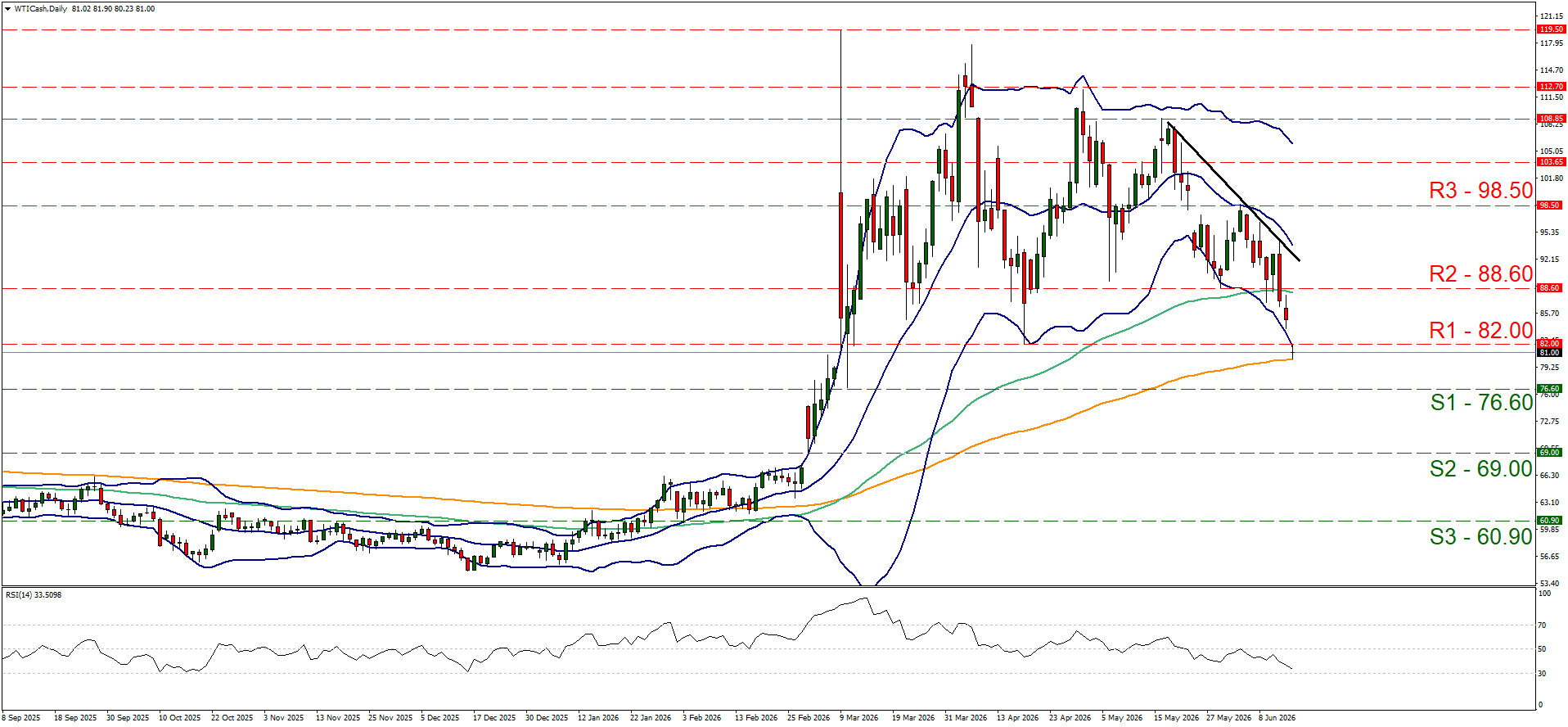

Charts to keep an eye out

USD/JPY remained in a tight rangebound motion just below the 160.50 (R1) resistance line. The bullish market sentiment seems to have eased, as the RSI indicator remains slightly above the reading of 50. The Bollinger bands are narrowing implying lower volatility for the pair, which in turn may allow the sideways motion to continue. Hence for the time being we maintain a bias for the sideways motion to continue, but at the end of the day, the pair’s direction may alter by BoJ’s interest rate decision. Should the bulls take over, USD/JPY may break the 160.50 (R1) line and start aiming for the 164.40 (R2) resistance level. Should the bears be in charge, USD/JPY’s price action may start aiming if not breaching the 157.50 (S1) support line.

WTI dropped breaking the 82.00 (R1) support line, now turned to resistance. We maintain a bearish outlook for WTI’s price given that, given that the RSI indicator edged even lower, signaling an intensifying bearish market sentiment for WTIs’ price. Yet the commodity’s price action has dropped below the lower Bollinger band which may slow down the bears or even cause a correction higher. Should the bears maintain control as expected, we may see WTI’s price aiming for the 76.60 (S1) support line, while even lower we note the 69.00 (S2) support base. For a bullish outlook which we consider as a remote scenario at the current stage, we would require WTI’s price to break the 88.60 (R2) resistance level, paving the way for the 98.50 (R3) resistance hurdle.

USD/JPY daily chart

- Support: 157.50 (S1), 155.00 (S2), 152.10 (S3).

- Resistance: 160.50 (R1), 164.40 (R2), 168.00 (R3).

WTI daily chart

- Support: 76.60 (S1), 69.00 (S2), 60.90 (S3).

- Resistance: 82.00 (R1), 88.60 (R2), 98.50 (R3).

Author

Peter Iosif, ACA, MBA

IronFX

Mr. Iosif joined IronFX in 2017 as part of the sales force. His high level of competence and expertise enabled him to climb up the company ladder quickly and move to the IronFX Strategy team as a Research Analyst. Mr.