U.S inflation will determine whether recent price action is corrective or a reversal

A lot has been said about equity markets falling over the last few weeks, but in my view the recent equity market sell-off, spike in volatility, and rise in 10-year UST yields can be attributed to one single catalyst - the latest Employment Situation Summary.

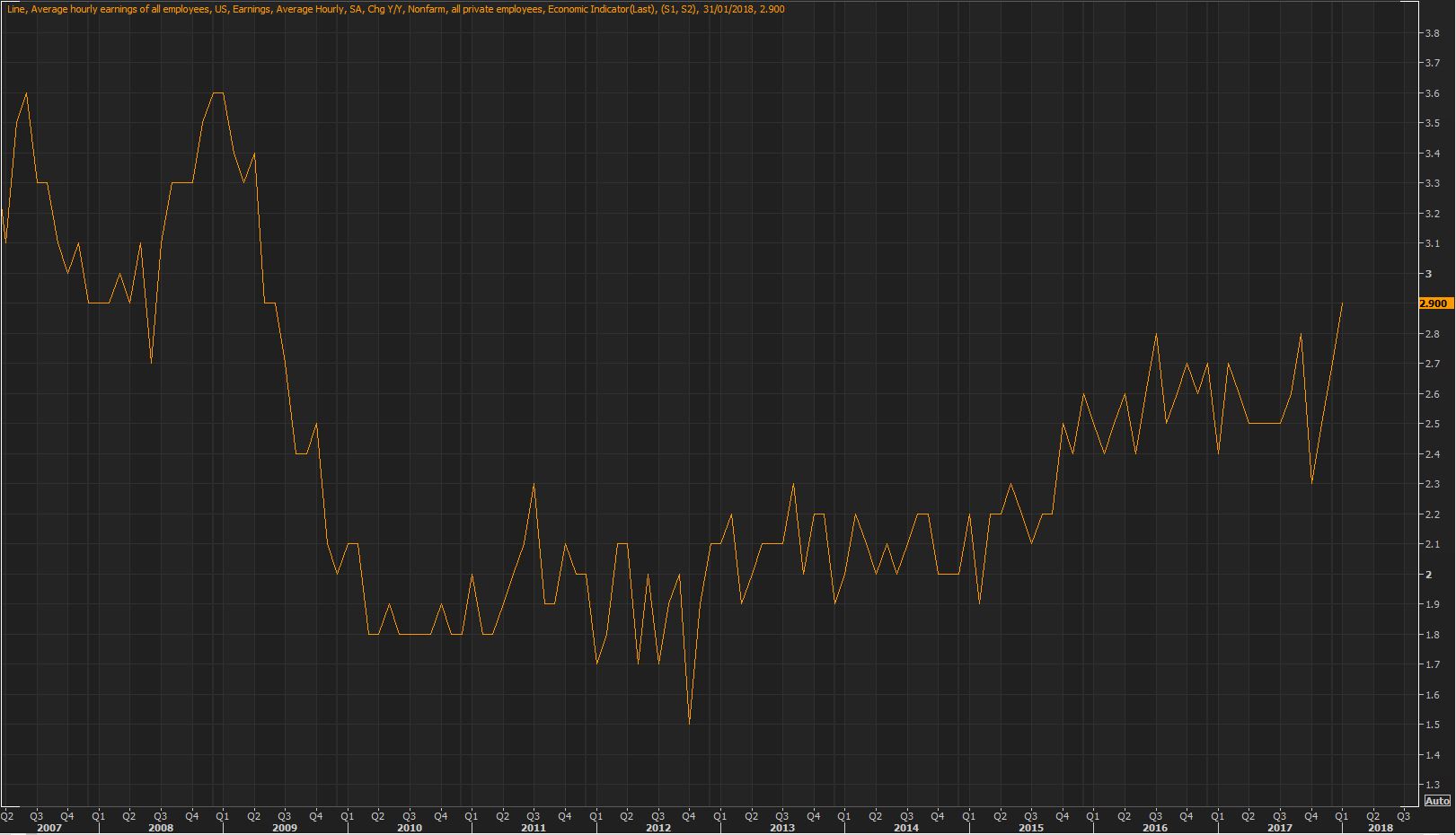

On the 2nd February the headline NFP number came in better than expected with an increase of 200k jobs in January. However, I believe the market mover was the average hourly earnings component which rose by 9 cents to $26.74 (an annual rate of 2.9%), the fastest pace in 8 years.

With the pickup in wage growth adding to an already healthy economy, traders once again began focusing on the FED rate hike narrative. Equity valuations are trading at lofty levels yet the market in a relentless uptrend. There are many sceptics out there that don’t believe in this bull market, especially at this late stage of the business cycle which made the thought of tighter monetary policy a legitimate cause for an aggressive correction.

Is this the end of the bull market, or an opportunity to buy? That’s anyone’s guess. From a technical perspective the S&P has found support on the long term trend line and 200 day moving average confluence. I prefer to structure my portfolio with long/short ratios to hedge out market risk and certainly have exposure to gold as a longer-term play.

With the FED and their policies once again on the radar, this week’s (Wednesday CPI, Thursday PPI) inflation data will add to the already volatile environment. The 12% decline in DXY and rise in wage growth is supportive of higher inflation, but, inflation has been stubbornly low for some time now so one data print isn’t all that convincing.

What does all this mean for the markets?

Well, if inflation data fails to show any upside surprises I expect the risk off sentiment that stemmed from tighter monetary policy conditions would ease, and the market to quickly get back to the dominant trends which would see equity markets rally and the USD resume its weakness against JPY and the Euro.

A rally in DXY to the 91.00 handle prior to the CPI releases would make selling a tempting proposition.

Author

Nicky Ong

Traders Corner

Nicky Ong is a Financial Trader since 2006. Having traded his own book and managed investor funds, he strongly believes in having a logical process to allow for the consistent development of well thought out trade ideas.