US Inflation Preview: Markets set to seize on falling Core CPI to revive pivot play, three scenarios

- US core inflation is set to slow down after two strong months.

- The Fed and markets focus on CPI data more than anything else, promising high volatility.

- Investors cling to good news, raising the chances of a stronger positive reaction in stocks.

Will Christmas come early? That is what investors seem to be craving for, jumping on good news to rise and dusting off depressing developments. The reaction to the all-important Consumer Price Index (CPI) report for October is set to be no different. And probably stronger.

Here is why I expect a robust reaction, with a bias toward a rally in stocks and a weaker US Dollar.

Why inflation is a huge market mover

The Federal Reserve is focused on its price stability mandate – bringing inflation back down. That has been the #1 concern for voters heading into the midterm elections. While ballots will be closed when the CPI data is released, elevated price rises will remain left, right and center for the central bank. It is easier when the labor market is strong.

Full employment is the Fed's second mandate, and with yet another significant gain of 261,000 jobs in October, the focus is inflation. Moreover, the Nonfarm Payrolls report showed that wages are rising at a healthy clip of 0.4% MoM, adding to inflationary pressures.

The past three CPI reports triggered violent market reactions – a rally in response to July's data and crashes in the following two months. There is no reason to expect a different outcome this time, especially as liquidity has dropped. The Fed is withdrawing money from markets as part of its tightening.

In its latest decision, the bank raised rates by 75 bps to 3.75-4%. While it opened the door to slowing down the pace of hikes in its upcoming December meeting, Fed Chair Jerome Powell and his colleagues vowed to fight rising prices, reaching a higher peak interest rate. That "terminal" level heavily depends on inflation.

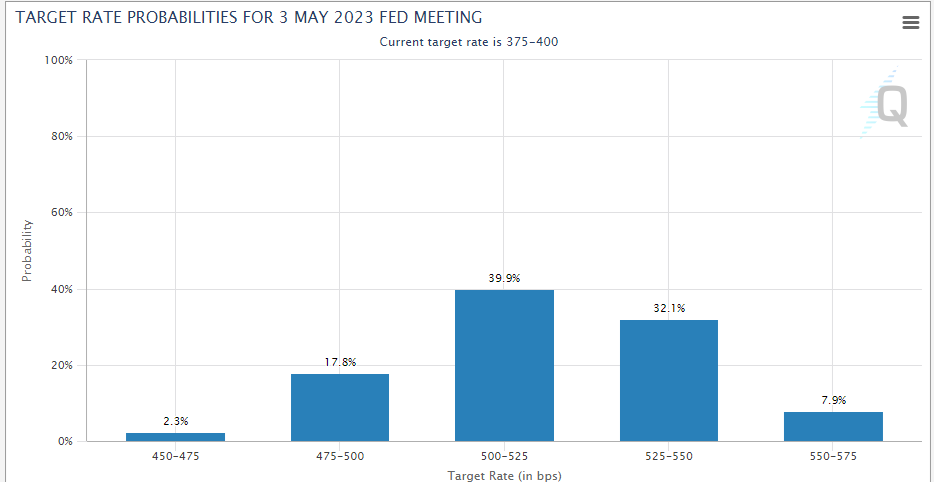

The terminal rate hovers around 5% according to bond markets:

Source: CME Group

What markets are expecting

As the central bank has limited influence on globally set and volatile energy and food items, it focuses on underlying inflation. Core CPI rose by 0.6% in the past two months, and the economic calendar indicates a modest decrease of 0.5%. While yearly core inflation climbed to 6.6% last month – the highest in 40 years – the focus is on the monthly figure, which should show the impact of the Fed's tightening.

Manheim reported a sharp, double-digit drop in prices of used vehicles. Clunkers were behind the initial rise in inflation back in 2021, and it makes sense for them to come down. On the other hand, increases in rent prices come with a lag. Housing accounts for nearly a third of core inflation, and it remains on the rise.

So far in 2022, Core CPI's have moved to the extremes:

Source: FXStreet

Three scenarios

1) Within expectations: A monthly increase of 0.5% would still represent an annualized increase of over 6%, substantially above the bank's 2% target. On the other hand, it would be lower than 0.6% recorded in the past two months. How would markets react to 0.5%?

This is where the market mood comes into play. China has been consistently denying rumors about loosening its covid zero policies, yet with every official rejection of this narrative, investors seem to believe it. "Never believe a rumor until it is officially denied" – this saying, associated with Otto von Bismarck, seems to be markets' mantra.

The same positive market reaction seems to resonate with the reaction to Friday's Nonfarm Payrolls. The robust rise in jobs and wages seemed sufficient to boost the US Dollar at first – but that didn't hold. An increase in the unemployment rate – to merely 3.7% – may have served as food for Dollar bears.

Therefore, a 0.5% Core CPI outcome, which would show underlying inflation is still hot, would be insufficient to knock stocks down or buoy the Dollar. Markets would shake and perhaps look for a surprise in the yearly figure. After a while, I expect the optimistic narrative to prevail, pushing shares up and the greenback down.

2) Below expectations: I initially thought that a monthly increase of 0.4% would also be within estimates, as it reflects an annualized level of around 5%. Nevertheless, the recent market behavior has convinced me that 0.4% would cheer markets. A 0.3% would be even more cheerful – that triggered a big upswing three months ago.

While one weak month could be dismissed, the Fed may be more open to talking about lower interest rates once the elections are over and political pressure is weaker.

To see substantially lower inflation, the shelter component would need to remain calm and items outside the automotive industry would need to suffer early Black Friday discounts.

The Dollar would extend its losses and everything would be set for a "Santa Rally"

3) Above expectations: A repeat of 0.6% as in the past two months or meeting the yearly peak of 0.7% as seen in June would deal a blow to markets. It would shatter hopes of a lower terminal rate and raise the chances of a fifth consecutive 75 bps hike in December.

In such a scenario, stocks would tumble back down and the Dollar would reclaim its throne. Shelter is the wildcard.

Final thoughts

While the scenarios seem straightforward, it would be remiss of me to end a preview of the No.1 market mover without providing an estimate. I believe Core CPI will miss estimates and hit 0.3%, a climbdown after two strong months. However, as the outcome hinges on a delicate figure, every tenth matters. Trade with care and lower your leverage around this critical release.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.