US industrial production - it will get worse

Weak industrial output is a concern. With supply chains set to face more disruption, and the energy sector hit by plunging prices, we see little prospect of near-term improvement. A rate cut before the end of 2Q20 looks ever more likely on the cards.

Industrial production fell 0.3% month on month in January versus predictions of a 0.2% decline.

The data shows the effects of the very warm January weather (it reached 69F in Manhatten the weekend of 11 January and 12th as I wore a T-shirt while watching my son play rugby down by Hudson River Park). Utility output plunged 4% in January after having declined 6.2% in December given no need for heating (and barely any need for the very expensive winter coat I was advised to buy after moving to New York).

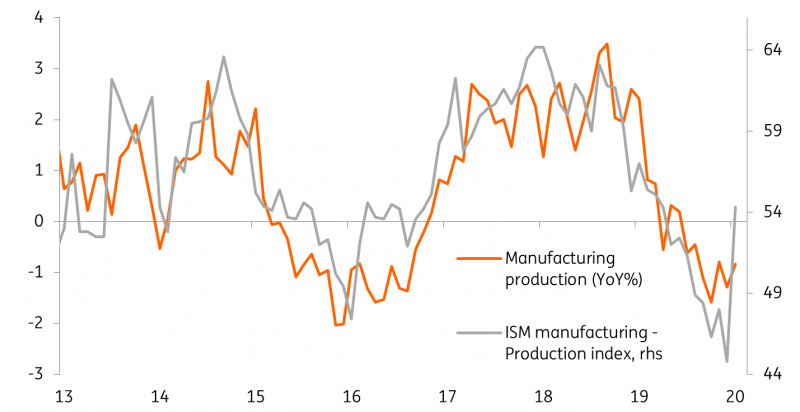

Manufacturing output was also weak (-0.1%MoM, matching expectations) despite the surge in the ISM production component (see chart). Given the ISM is a survey, it may well be that it over-represents the true situation as sentiment rebounded in the wake of the US-China phase one trade deal and participants felt a wave of relief. Further weakness is likely too in manufacturing output figures given that Boeing 737 Max production only ended in the second half of the month, so it is more of a story for February.

ISM manufacturing vs production

Source: Macrobond

The new issue is, of course, supply chain disruption resulting from lower Chinese and Asian factory output due to the impact of the coronavirus. This is already leading to a shortage of components and parts in factories around Asia and it is only a matter of time before it becomes more of an issue for Europe and the Americas - they are that bit further away so there is longer shipping time and a greater delay to the impact.

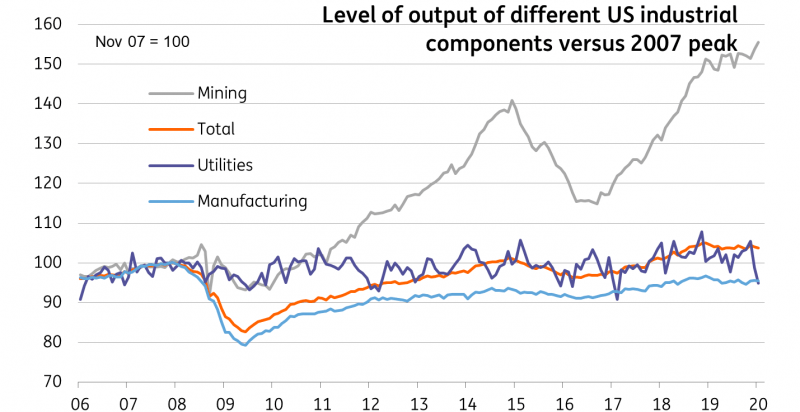

Rounding out, mining was actually pretty good, rising 1.2%MoM despite oil and gas rig counts being largely flat on the month, but with energy prices having plunged we have to be braced for declines in drilling in coming months.

Industrial production breakdown

Source: Macrobond, ING

Read the original analysis: US industrial production - it will get worse

Author

James Knightley

ING Economic and Financial Analysis

James Knightley is the Chief International Economist in London. He joined the firm in 1998 and has been covering G7 and Western European economies. He studied economics at Durham University, UK.