US: Higher inflation but not spinning out of control due to still well-behaved expectations

Key takeaways

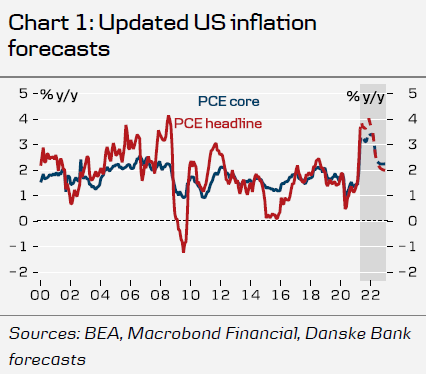

In this piece, we take a deep dive into the US inflation dynamics. We go through different drivers both from a top-down and bottom-up perspective. Based on our analysis, we project PCE inflation will be 3.3% y/y this year and 2.5% y/y next year (PCE core inflation: 2.8% y/y and 2.6% y/y).

Inflation expectations suggest that inflation will be higher on a sustained basis compared to the years before the pandemic hit. A downside risk is that inflation expectations may decline when inflation peaks (all else equal).

Higher money velocity would be inflationary but we doubt that M2 money velocity will return all the way back to its pre-pandemic level, as some of the money are spent on transactions not included in GDP (like real estate transactions and transactions in financial assets, where we have already seen large price increases).

Some of the broad price increases may take time to materialise due to sticky prices.

We expect higher wage growth, reflecting both higher inflation expectations and higher demand for labour. This should support higher inflation on a more sustained basis. The Phillips curve relationship has been weak for several years, likely because inflation expectations have become well-anchored.

Rising food and commodity prices mean higher headline inflation and inflation expectations. As we do not expect the economy to enter a commodities super cycle, we expect food and commodities price inflation to ease, which should also ease total headline inflation and all else equal pull inflation expectations lower.

PCE core goods inflation is likely to remain high for now. A stronger USD and lower goods demand should slow PCE core goods inflation in 2022.

PCE core services excluding housing and health care inflation is, in the long-run, mostly driven by inflation expectations. The current level of long-term inflation expectations suggest PCE core services excluding housing and health care inflation will run around 2.5-3.0% y/y.

Rent have started to increase sharply after the slowdown in 2020 and early 2021. We expect higher rent inflation near-term but since we expect house price increases will slow down somewhat, we expect rent inflation will settle at around 3.5% y/y.

Wage growth is important for PCE health care inflation. If wage growth increases due to higher inflation expectations we are likely to see higher PCE health care inflation also further out. We expect PCE health care inflation to run around 3% y/y.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.