US First Quarter GDP Preview: Reasons to be cheerful

- US economic growth forecast to be stable in the first quarter

- Improved consumer attitudes and retail sales give reason for optimism

- Labor market key to economic growth

The Bureau of Economic Analysis a division of the Commerce Department will issue its first estimate for annualized gross domestic product for the first quarter at 8:30 am EDT, 12:30 pm GMT on Friday April 26th.

Forecast

American economic growth is predicted to be 2.1% annualized in the first quarter following the fourth quarter’s 2.2% rate. Core personal consumption expenditures are expected to be 1.6% down from the prior 1.9%.

Economic Growth and the Labor Market

In an economy that is about 70% fueled by household spending as is the US the attitudes and outlook of the consumer are paramount. Business investment is an important if secondary factor but it is one that tends to follow the prevailing consumer direction. The most salient fact for consumption is the state of the labor market.

If people are working and confident in the stability of their income and in their ability to find a new job should that need arise they will be disposed to spend a good portion of their disposable income.

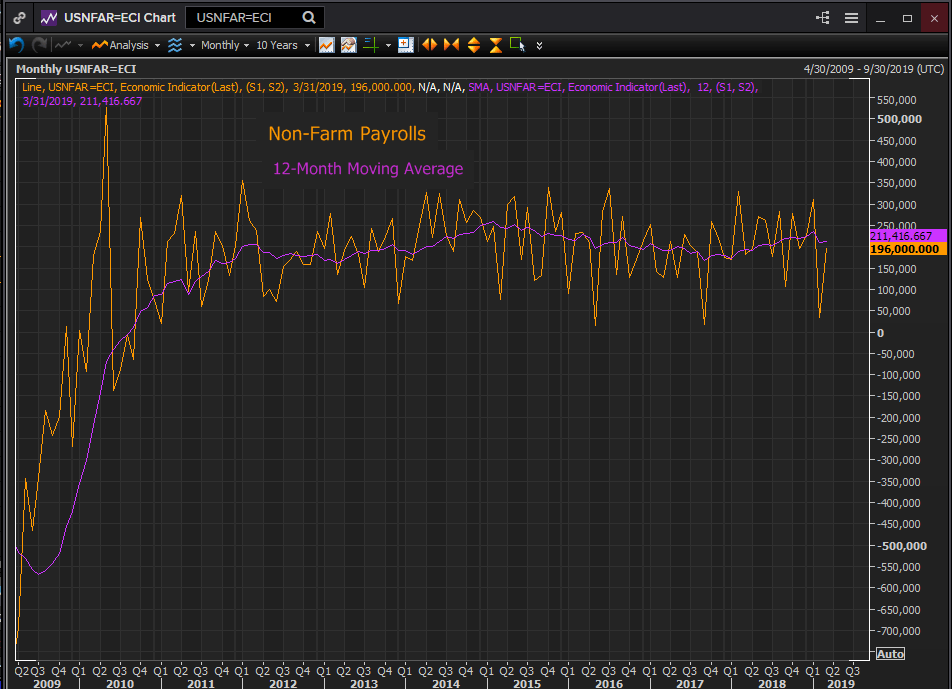

The success of the labor market in generating jobs over the past two years is a well-known story. From a low in the 12-month moving average for non-farm payrolls in September 2017 of 167,700 the average moved steadily higher reaching 235,000 in January of this year. The one month fall to 33,000 in February, bracketed by 312,000 in January and 196,000 in March was inconsequential perhaps conditioned by the government closure in January.

Reuters

Wage increases have climbed to their highest post-recession point as labor shortages have compelled employers to compete for workers. The 3.4% annual gain in February was the highest since April 2009. The drop to 3.2% in March still leaves workers better off than at any point in the ten years prior to October 2018.

Consumer Optimism

American consumer attitudes have, for the most part, regained the altitude of the past two years after a brief plunge during the partial government shutdown that ended on January 25th. The US electorate has a long standing distaste for government closures stemming from political disputes in Washington.

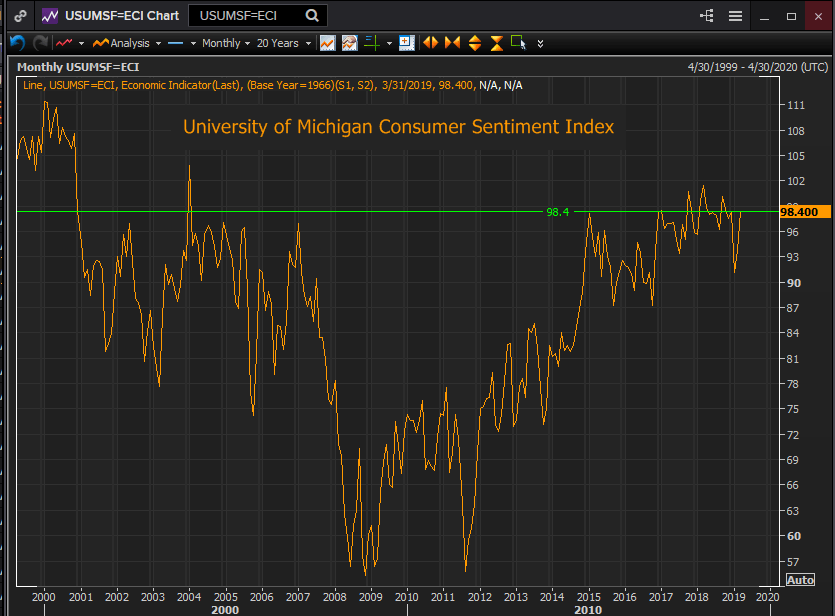

The University of Michigan Consumer Sentiment Index rebounded to 98.4 in March, on par with readings in 2017 and 2018, after the January drop to 91.2. Interestingly, it was the expectations index that was closer to its post-recession high—88.8 in March vs 91.0 in January 2015 than the current conditions index—113.3 vs 121.2 in March 2018.

Reuters

The Conference Board reading is similar if less definitive in its return. After reaching its post-recession high of 137.9 last October it had fallen to 126.6 by December, skidded to 121.7 in the month of the shutdown, recovered to 131.4 in February and then turned down to 124.1 in March. April’s reading is due on the 30th of the month, 126.0 is expected.

Retail Sales and Durable Goods

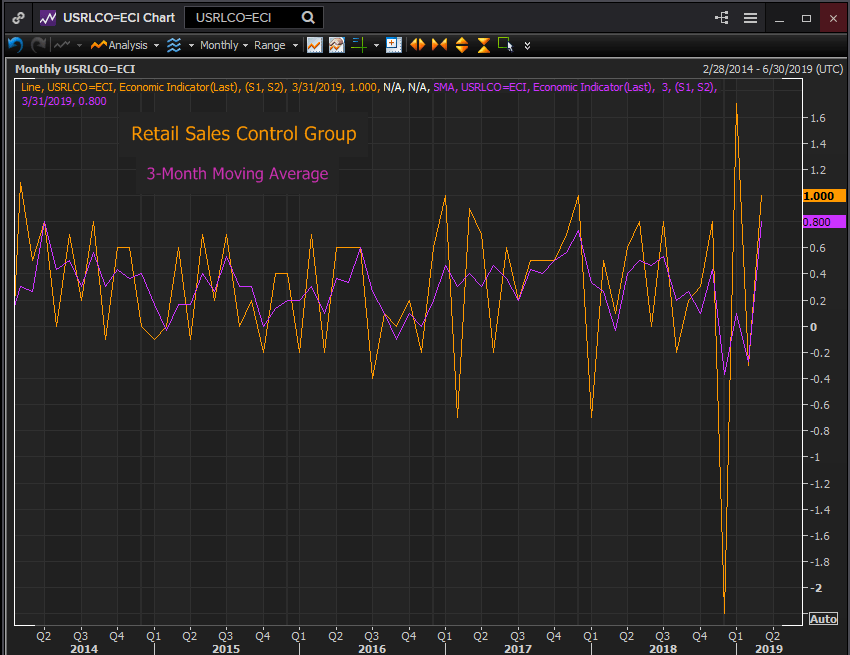

Retail sales provided a healthy surprise in March rising 1.6% on a 0.9% forecast. The GDP component control group more than doubled expectations jumping 1.0% against a 0.40% prediction. This gives the first quarter a 0.73% monthly average gain. In comparison the final quarter of last year sports a -0.20% monthly average.

The control group exhibits the same preference. The first quarter average is 0.80%. The fourth quarter equivalent is -0.37%. Even given the reporting difficulties around the government shutdown in January these are substantial differences.

Reuters

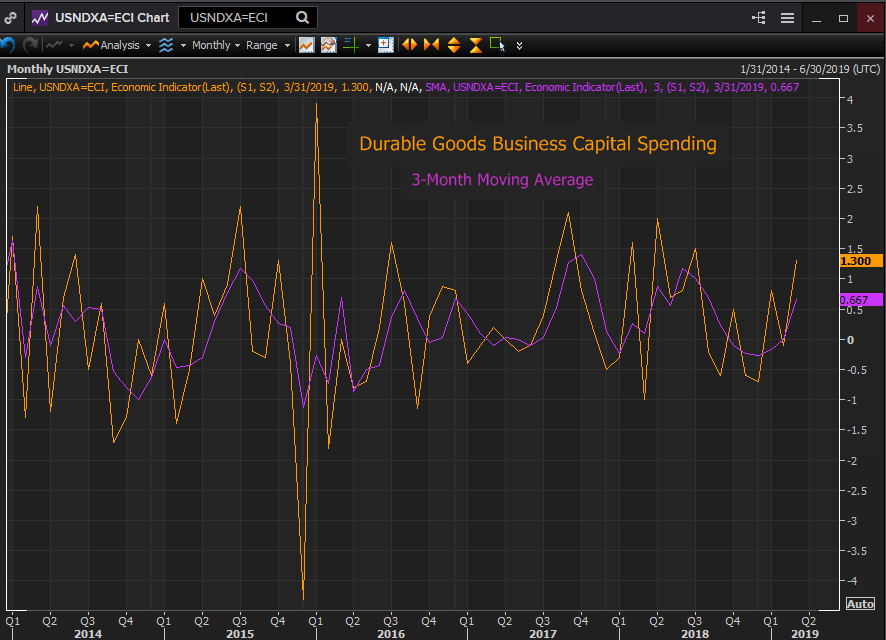

Durable goods orders are in the same situation. The first quarter average is 0.50%, that of the fourth is -0.77%. Capital goods rose on average 0.67% in quarter one, in the final three months of last year they sank 0.27% each month.

Reuters

It would be unusual if the marked improvement in consumption from the fourth quarter to the first were not reflected in the GDP figures.

Business Confidence

Optimism in the business community was lower in the first quarter than the fourth but the difference is not large and in the context of strengthening consumer spending probably retrograde.

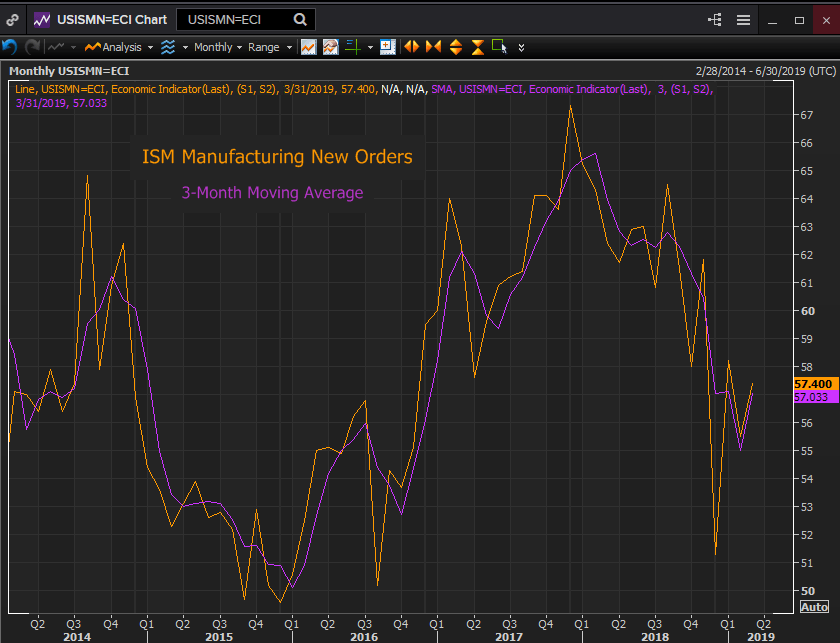

The purchasing managers’ index for manufacturing from the Institute for Supply Management averaged 56.8 in the fourth quarter, 55.3 in the first. However, the new orders index average, indicative of future business was identical in both quarters , 57.03.

Reuters

The services index was 59.47 in the fourth quarter and 57.5 in the last three months. The new order index was 62.38 in 2018’s final quarter and 60.63 in 2019’s first.

All the PMI reading from the last six months are firmly in expansion territory. There is no indication that business managers are feeling a worrisome decline in orders, general activity or the need for new hires. The declines in several of the indexes are probably as much a function of their previous elevation as any important change in business conditions.

US GDP: Conclusion

The fourth quarter's 2.2% annualized GDP pace is forecast to carry over into the first three months of this year with the 2.1% consensus estimate.

However, the late arriving retail sales figures, the much better business capital spending, the rebound in consumer optimism and the buoyant labor market background all point to an improvement in the general economy in the just completed quarter. The Atlanta Fed GDPNow model agrees positing a 2.7% pace.

Where the US consumer leads, the economy always follows.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.