US ISM Manufacturing PMI February Preview: Will business catch up with consumers?

- Purchasing Managers' Index forecast for small variation to 58.9 from 58.7.

- New Orders have been strong for six months, employment lagging.

- Retail Sales soar in January, Durable Goods, business investment strong.

- Markets and the dollar waiting for confirmation of US economic resurgence.

Business executives have been cautiously optimistic for several months, investing but not hiring. While January's near record run in US Retail Sales and the looming end of the pandemic may suggest that that the recovery is at hand, employment will likely remain restrained for some time.

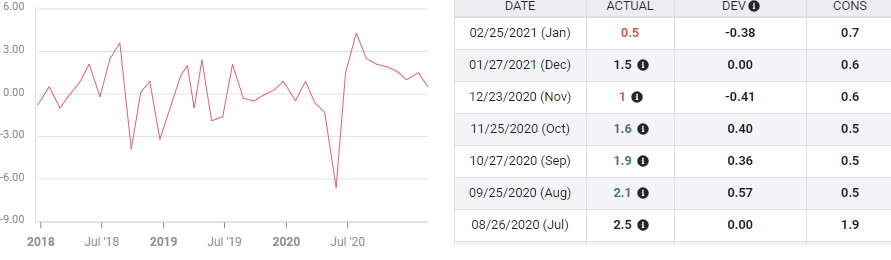

The Purchasing Managers' Index (PMI) from the Institute for Supply Management (ISM) is expected to edge to 58.9 in February from 58.7 in January. The Prices Paid Index is forecast to drop to 77 from 82.1. The New Orders Index was 61.1 in January and the Employment Index was 52.6.

Manufacturing PMI

Since rebounding from the March and April lockdown collapse manufacturing sentiment has averaged 57.8 from August to January, the best run since the second half of 2018. New orders have been particularly strong with the best six-month record at 64.6 in over two decades.

Manufacturing PMI

The laggard through that period has been the Employment Index which only reached the 50 division between expansion and contraction in October.

Problems in manufacturing employment predate the pandemic plunge in March and April. The descent from March to December 2019 was due to the trade friction between the United States and China. No sooner was the trade agreement signed in January 2020 than the economy was pushed off the economic cliff by the pandemic.

Business optimism has reflected the influx of orders in the second half of 2020 and the response has been spate of investment spending.

Nondefense Capital Goods

For the six months ending in January business investment spending as tracked by the Durable Goods category Nondefense Capital Goods ex Aircraft has averaged a 1.43%, the best run in over seven years.

Nondefense Capital Goods

Retail Sales

The Retail Sales burst of 5.3% in January has been credited to the $600 checks received by many families from the December stimulus package. With another $1400 on the way and the pandemic winding down, consumer spending will likely remain strong as the relief combines with extra cash.

Conclusion

The expectations for surge of strong economic growth portrayed in equity and commodity price levels, and US Treasury rates and powered by a liberated American consumer, was confirmed in January Retail Sales. Whether it continues through the spring is the main economic question.

Federal Reserve Chairman Jerome Powell seemed to endorse the possibility when he noted that US growth could reach 6% in 2021.

The late week rally in the US dollar, keyed on Treasury rates. If American business is more optimistic that forecast in February, especially in hiring, markets will notice.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.