US Durable Goods Preview: Shutdown reporting vs the trend

- Strong rebound in durable goods orders forecast for December

- Second major delayed economic release for the holiday shopping season

- Business spending expected to be positive after 3 out of 4 negative months

The US Census Bureau will issue its delayed Durable Goods report for December on Thursday February 21st at 8:30 am EST, 13:30 GMT.

Forecast

New orders for durable goods are predicted to increase 1.7% in December following November’s 0.7% gain and the 0.8% rise in October. Orders excluding aircraft and parts, also called the ex-transport category, are expected to rise 0.3% after November's 0.4% loss and October 0.3% decline. The proxy for business investment, non-defense capital goods ex-aircraft and parts, is forecast to increase 0.2% following November’s 0.6% drop and October’s 0.5% gain.

Durable Goods: Reporting from the government shutdown

This series covers wide range of manufactured consumer and industrial products designed to last three years or more in use. Ranging from electric toothbrushes, toasters and cell phones through automobiles, construction equipment and commercial airliners, the orders give a broad picture of consumption and investment in the economy. The December number is a large part of the holiday spending picture and the year end profit of many retail firms.

The December durable goods report is about one month overdue, delayed by the 35 day government shutdown that ended on January 25th.

The forecasts are based on economic assessments, seasonal variations and overall trends in consumer spending and business investment. It will not be known until the release of the December statistics if the goods orders have some of the reporting problems that were widely suspected of skewing the retail sales numbers well below their projections.

Retail sales as reported by the Census Bureau, a division of the Commerce Department were down 1.2% overall against a forecast for a 0.2% increase. The control group category which is used by the Bureau of Economic Analysis to calculate GDP fell 1.7%, far below the prediction for a 0.4% gain.

The Commerce Department noted in reference to the sales numbers that "data collection and processing were delayed." Was the December sales information incorporated into the January numbers by reporting firms or were there other issues with assembling and collating the data?

The retail figures were in contrast to both the long term trend in employment and wages and more importantly private company and survey sales numbers for December.

Amazon the world’s largest internet retail operation reported record holiday sales. That belies the government statistic which said internet sales fell nearly 3.9% in December.

The weekly Redbook index for same store sales rose 6% weekly in December. In the last week of 2018 same store sales showed a 9.3% annual gain the largest on record. The Redbook survey tracks sales at stores representing over 80% of the Commerce Department’s retail sales report.

MasterCard said that its credit card purchases were 5.1% higher in 2018 over the previous year.

While the reporting issues were not detailed by the Commerce Department it seems unlikely that the Census report of declines in every category of sales except automobiles and building supplies is accurate.

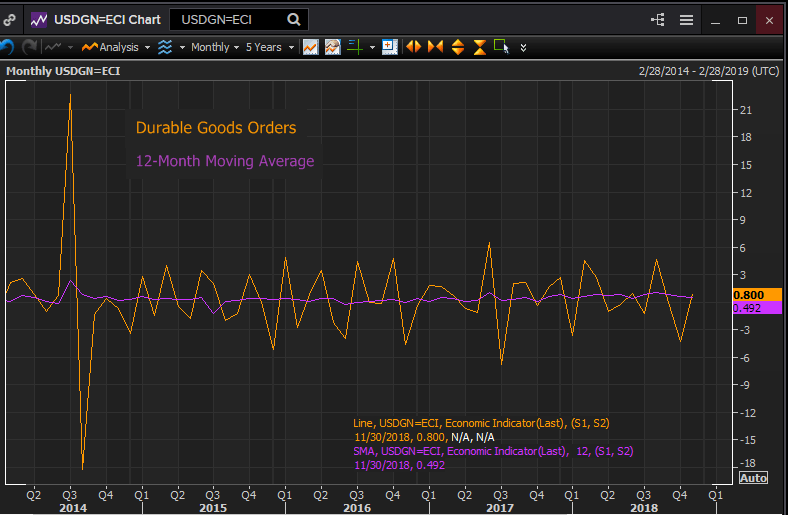

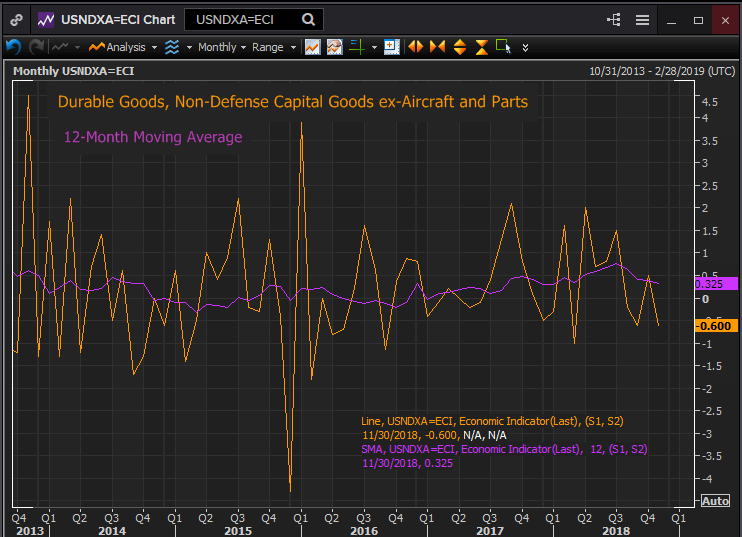

Durable goods trends

Overall goods orders were on a rising trend from mid-2016 until this past August. The 12-month moving average improved from -0.267% in June 2016 to 1.075 % last summer. The average had dropped to 0.492% by November.

Reuters

Business spending, the ungainly aforementioned non-defense capital goods ex-aircraft and parts, also exhibited a rising average from -0.207% in October 2016 to 0.758% last July, a five year high, before tailing off to 0.325% in November.

Reuters

The consumption trends in durable goods coincided, not surprisingly, with the two year improvement in consumer and business sentiment that followed the 2016 national election. The government shutdown in late December and January put a serious dent in high flying sentiment numbers and though both sides of the equation have recovered they remain below the peaks of last summer.

Durable goods as retail sales are reflective of the overall economic performance of the US economy and the optimism of the consumer. Business investment follows consumption and both are likely to return after several months of slowdown.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.