US Durable Goods Orders May Preview: Retail trumps the lockdown blues

- Durable goods orders expected to follow retail sales higher.

- Business spending gain forecast to be modest, PMIs remain in contraction.

- Equities and currencies have priced a strengthening economic recovery.

The American consumer proved ready to shed the lockdown blues in May returning to the stores and malls in great numbers and sending retail sales figures soaring to the largest monthly increase on record.

It would be illogical to expect that the durable goods, a component of retail spending, will perform differently.

New orders for durable goods are expected to rise 10.6% in May after collapsing 17.7% in April as most of the country entered mandatory quarantine. Orders outside of the transportation sector are predicted to climb 2.5% following the 7.7% drop in April. Non-defense capital goods ex-aircraft, the proxy for business spending, is forecast to add 1% after the April 6.1% decrease.

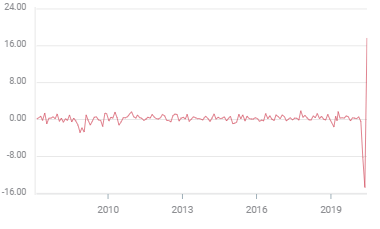

Retail sales

The retail performance in May was much better than anticipated. Overall retail sales jumped 17.7% on an 8% prediction, sales ex-autos rose 12.4% versus a 5.5% estimate and the control group, which informs the GDP calculation, climbed 11%, well beyond the 4.7% prediction. Each May increase was the largest on record as was each April decline.

Retail sales

More important for the economy retail sales reversed the 14.7% April collapse giving businesses an immediate cash infusion.

As promising as the purchasing figures were last month and as encouraging to businesses seeing customers for the first time in two months, June sales not May will be the test.

If the May spending burst was largely due to purchases deferred from March and April and June sales then tail off the single strong month will be unlikely to prompt much additional hiring. If consumption continues at normal or higher levels then the virtuous circle of spending leading to hiring and then more spending will get a kick-start.

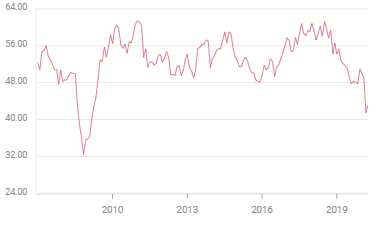

Purchasing managers’ indexes and NFP

Business sentiment has recovered from its April depths. While the Institute for Supply Management manufacturing index rose to 43.1 in May from 41.5 and the services score climbed to 45.4 from 41.8, both remain below the 50 division between expansion and contraction.

ISM manufacturing PMI

The employment gauges were the weakest of the set: for manufacturing 32.1 in May from 27.5, missing the 35 forecast; in services 31.8 from 30 in April but below the 35.8 prediction.

Even though non-farm payrolls rose an unexpected 2.5 million in May rather than dropping another 8 million as forecast managers remain pessimistic.

Conclusion and markets

Markets are waiting for proof that the recovery they have priced in is well under way. Consumers have cooperated and there is every reason to expect the large ticket items of durable goods to perform as well as overall retail sales. Equities will applaud and the dollar will have yet more preparation for its eventual rise.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.