US Dollar Weekly Forecast: The Fed is not ready to blink, and the Dollar knows it

- The US Dollar traded in an inconclusive fashion this week.

- Markets kept swinging between geopolitics and Fed rate hike bets.

- The Fed Minutes suggested that extra caution may be needed.

The week that was

The US Dollar’s (USD) week was an apathetic one. There were ups and downs and plenty of uncertainty in the geopolitical field. Come Friday, and there is still no news regarding a potential US-Iran deal to end the Middle East conflict or at least bring in some clarity, particularly regarding the reopening of the Strait of Hormuz.

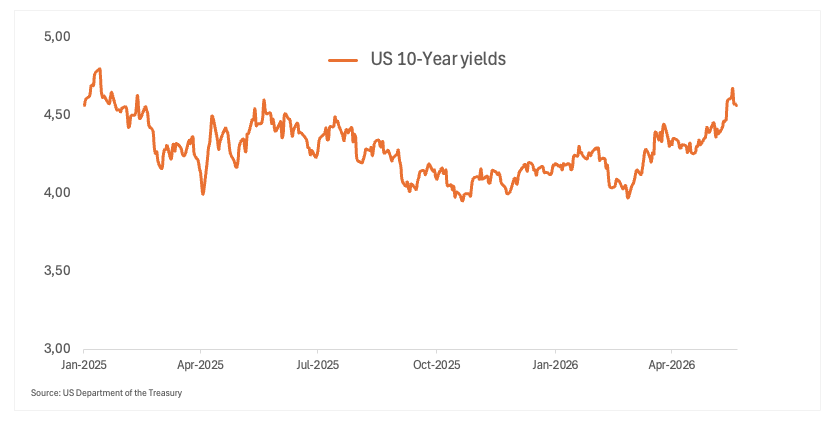

Against that backdrop, the US Dollar Index (DXY) ended the week pretty much at Monday’s levels in the low-99.00s, with US Treasury yields also navigating a mixed range: the short-end of the curve hitting fresh highs vs. corrective moves in both the belly and the long end.

On the data space, the salient event was the publication of the FOMC Minutes of the April 28-29 meeting, which delivered a hawkish-ish message after suggesting that further caution would be required.

Fed speakers keep the hawkish tone alive

Federal Reserve (Fed) officials maintained a cautious and broadly hawkish tone this week, with policymakers continuing to stress that inflation risks remain too elevated for the Federal Reserve to seriously consider rate cuts anytime soon. Comments from Goolsbee, Paulson, Barkin and Waller also highlighted growing attention on AI, bond market dynamics and geopolitical risks.

Austan Goolsbee (Chicago, 2027 voter) said inflation remains too high and warned the Fed cannot risk cutting rates prematurely, arguing that easing too aggressively could reignite price pressures. He also described the labour market as stable and said inflation should remain “front of mind” once Kevin Warsh becomes the Fed Chair.

Anna Paulson (Philadelphia, voter) said a rate hike could still be considered if growth accelerates or inflation risks intensify. She warned that risks to both inflation and the broader outlook remain “super elevated” and added that a prolonged Iran conflict could raise risks to both inflation and unemployment.

Thomas Barkin (Richmond, 2027 voter) said the Fed is balancing risks on both sides of the mandate and argued the situation is not the right environment for strong forward guidance. He added that inflation expectations remain relatively anchored and described current bond yields as still being in a “reasonable zone".

Christopher Waller (FOMC Governor, voter) warned that rising inflation expectations would become a major concern for the Fed and dismissed near-term rate cut discussions as “crazy” given recent data. He also defended the need for an ample reserves framework and stressed the importance of central bank independence.

Bottom line

The overall Fed tone remained cautious and mildly hawkish. Inflation remains the key risk in the eyes of policymakers, while geopolitical tensions and fiscal concerns are also adding to the uncertainty of the outlook. The message to markets remains the same: the Fed is in no rush to ease policy.

The Minutes reinforced the same message

The Fed minutes added to the growing sense that US rates could stay higher for longer. Policymakers still seem uneasy about inflation risks, particularly with higher energy prices and ongoing geopolitical tensions threatening to slow the disinflation process. Unless inflation starts cooling more convincingly, or tensions in the Middle East ease materially, the Fed still looks some distance away from signalling any genuine dovish shift.

Inflation is no longer moving in the right direction

As widely expected, inflation accelerated sharply in April.

Headline CPI rose 3.8% YoY, up from March’s 3.3% gain, while core inflation, which excludes food and energy, accelerated to 2.8% from 2.6%.

The return of price pressures suggests that the disinflationary trend seen earlier this year may already be fading.

Geopolitical tensions, particularly the rebound in Oil prices following the continued closure of the Strait of Hormuz, have added a fresh layer of inflation pressure.

Meanwhile, the lagged impact of US tariffs is only just starting to filter through supply chains and consumer prices, raising the risk that inflation could remain sticky for longer than anticipated.

That’s precisely the combo markets fear most: disinflation slowing but the economy still holding up.

The labour market still refuses to crack

The latest report on the US labour market showed that the economy added 115K jobs in April, comfortably beating expectations and adding to March’s upwardly revised 185K increase.

Meanwhile, the Unemployment Rate held steady at 4.3%.

Wage pressures also continued to edge higher, with Average Hourly Earnings rising 3.6% YoY from 3.4% previously, reinforcing concerns that underlying inflation pressures remain difficult to fully eliminate.

The broader takeaway is that the labour market is cooling, but not fast enough to force the Fed into a dovish pivot anytime soon.

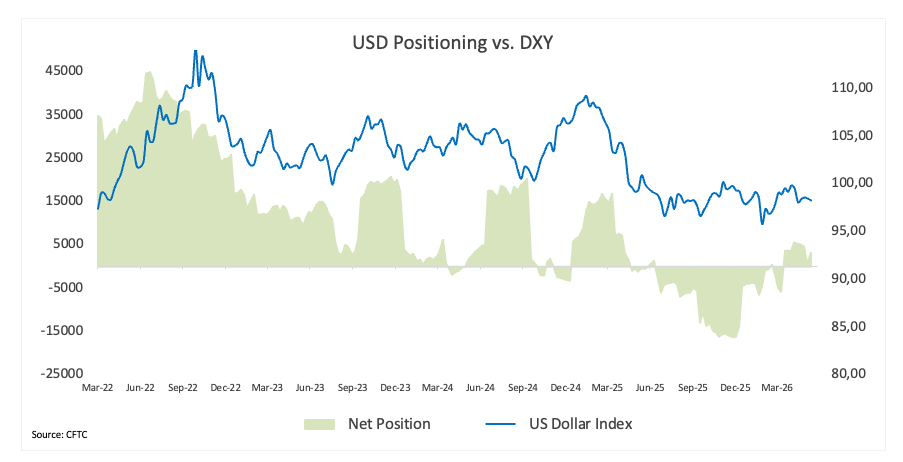

Speculative flows are turning back toward the buck

Non-commercial net longs in the US Dollar increased to two-week highs near 3.2K contracts in the week ending May 12, according to the latest Commodity Futures Trading Commission (CFTC) release.

Even so, speculative accounts maintained bullish Dollar exposure for a ninth consecutive week, while open interest eased a tad from the previous week, standing at around 32.1K contracts.

That positioning dynamic matters.

Despite months of market discussions around eventual Fed easing, speculative flows have never fully abandoned the Greenback. This week’s Fed repricing may now encourage investors to rebuild bullish exposure more aggressively in the upcoming weeks.

Technically, the DXY still appears capped by the 99.50 zone, but the latest price action increasingly resembles accumulation rather than exhaustion.

What’s next for the US Dollar

Next week, everyone will be focused on the release of inflation figures measured by the Personal Consumption Expenditure (PCE), which are expected to echo the stickier inflation trends already seen in CPI data that have kept running above the Fed’s 2.0% goal and are expected to remain at those levels for the foreseeable future.

Investors will also continue monitoring developments surrounding the Middle East conflict, Oil prices and the Strait of Hormuz, all of which are rapidly becoming central variables in the Fed outlook.

Meanwhile, Fed speakers are expected to remain highly active, especially after investors reprice rate hikes later in the year.

The market may have misread the Fed

For much of 2026, markets operated under the assumption that the next major move from the Federal Reserve would eventually be lower rates.

That assumption is now being challenged.

The combination of sticky inflation, resilient economic activity, elevated Oil prices and renewed supply-chain disruptions has materially complicated the Fed’s path back toward easing. More importantly, officials no longer sound fully confident that inflation will continue cooling on its own.

That does not necessarily mean the Fed is about to deliver another hike immediately.

But it does suggest the bar for rate cuts has moved significantly higher.

In practical terms, that environment should continue supporting US Treasury yields and, by extension, the US Dollar.

The DXY may now be entering a broader recovery phase after spending months consolidating near multi-month lows. If inflation remains elevated and the Middle East conflict continues disrupting energy markets, a move back above the 100.00 barrier could become increasingly likely in the weeks ahead.

For now, the Dollar’s biggest support may simply be this:

The market may have underestimated how difficult the final stage of the inflation fight was always going to be.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.